Why was Rule 86B introduced under GST regime?

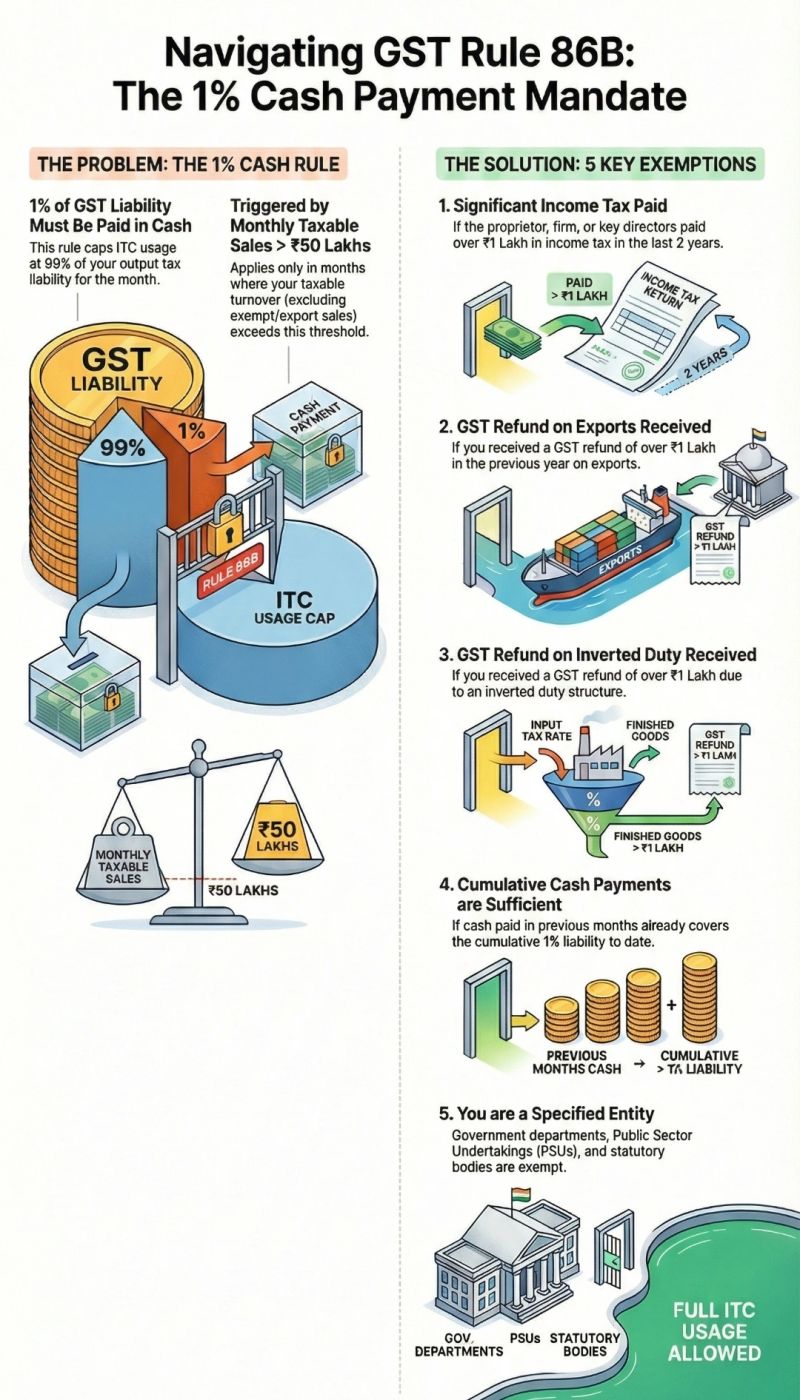

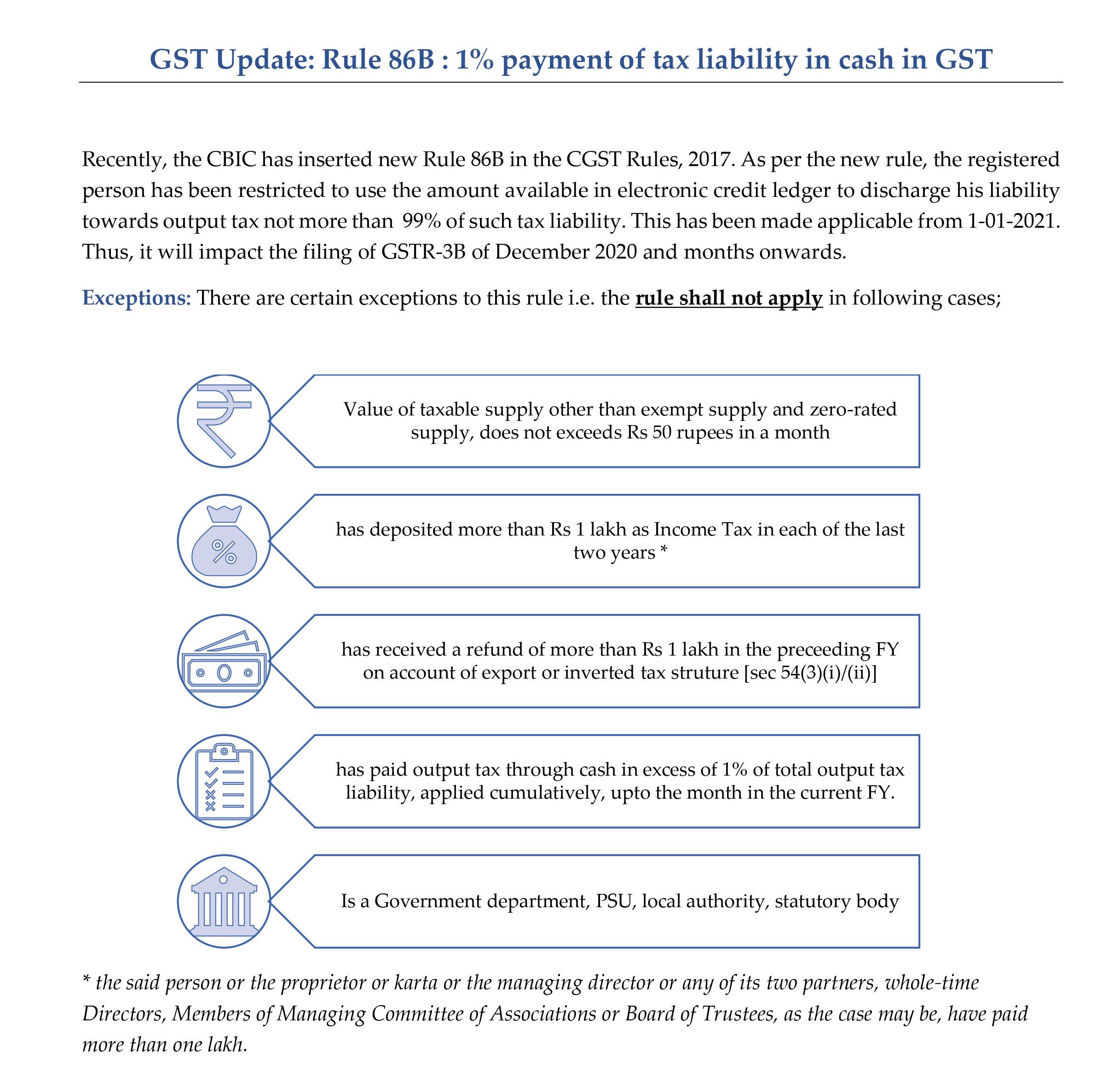

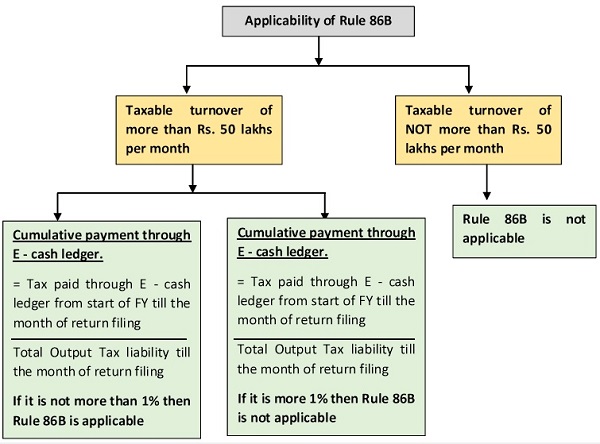

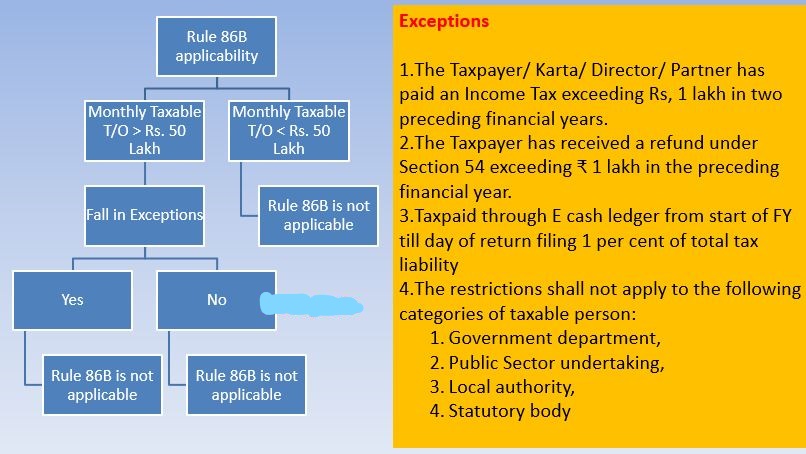

Rule 86B under the GST Regime Rule 86B is a provision introduced under the Goods and Services Tax (GST) regime to restrict the use of Input Tax Credit (ITC) for paying output tax liability. Applicability: This rule applies to registered persons whose taxable value of supply (excluding exempt supply and zero-rated supply) in a month exceeds Rs. 50 lakh.

Key Provisions on Rule 86B under the GST Regime :

- Purpose: The primary aim of Rule 86B is to prevent tax evasion and fraud. It targets taxpayers who claim fake ITC and do not pay any tax in cash.

- Compliance with Rule 86B is determined based on the GST returns filed by the firm, rather than the Income Tax Returns (ITR) of the firm or its directors.

- This rule ensures that there is a minimum cash payment of 1% of the output tax liability, enhancing the authenticity and accountability of the ITC claimed by businesses.

- Restriction on ITC Usage: Such registered persons cannot use more than 99% of their ITC balance to discharge their output tax liability. They must pay at least 1% of their output tax liability in cash.

- Exceptions of Rule 86B under the GST Regime

-

- Taxpayers who have paid more than Rs. 1 lakh in income tax in the preceding two financial years.

- GST Taxpayers who have received refunds of unutilized ITC on account of zero-rated supplies or inverted duty structure of more than Rs. 1 lakh in the preceding financial year.

- Taxpayers who have made cash payments exceeding 1% of their total tax liability for the current financial year up to the said month.

Conclusion

GST Rule 86B is a measure to ensure that registered persons with significant taxable supplies make a minimum cash payment of their output tax liability, reducing the scope for fraudulent ITC claims and increasing tax compliance.

Rule 86B is a new rule introduced under the GST regime that restricts the use of input tax credit (ITC) available in the electronic credit ledger for paying the output tax liability. This rule is applicable to registered persons who have a taxable value of supply (other than exempt supply and zero-rated supply) in a month exceeding Rs. 50 lakh. According to this rule, such persons cannot use more than 99% of their ITC balance to discharge their output tax liability, and they have to pay at least 1% of their output tax liability in cash. This rule is aimed at preventing tax evasion and fraud by unscrupulous taxpayers who claim fake ITC and do not pay any tax in cash.

The rule 86B is to be checked on the basis of the GST returns of the firm, not the ITR of the firm or the directors