Presumptive Taxation Scheme for Business Section 44AD

Page Contents

Presumptive Taxation Scheme for Business Section 44AD of Income Tax Act

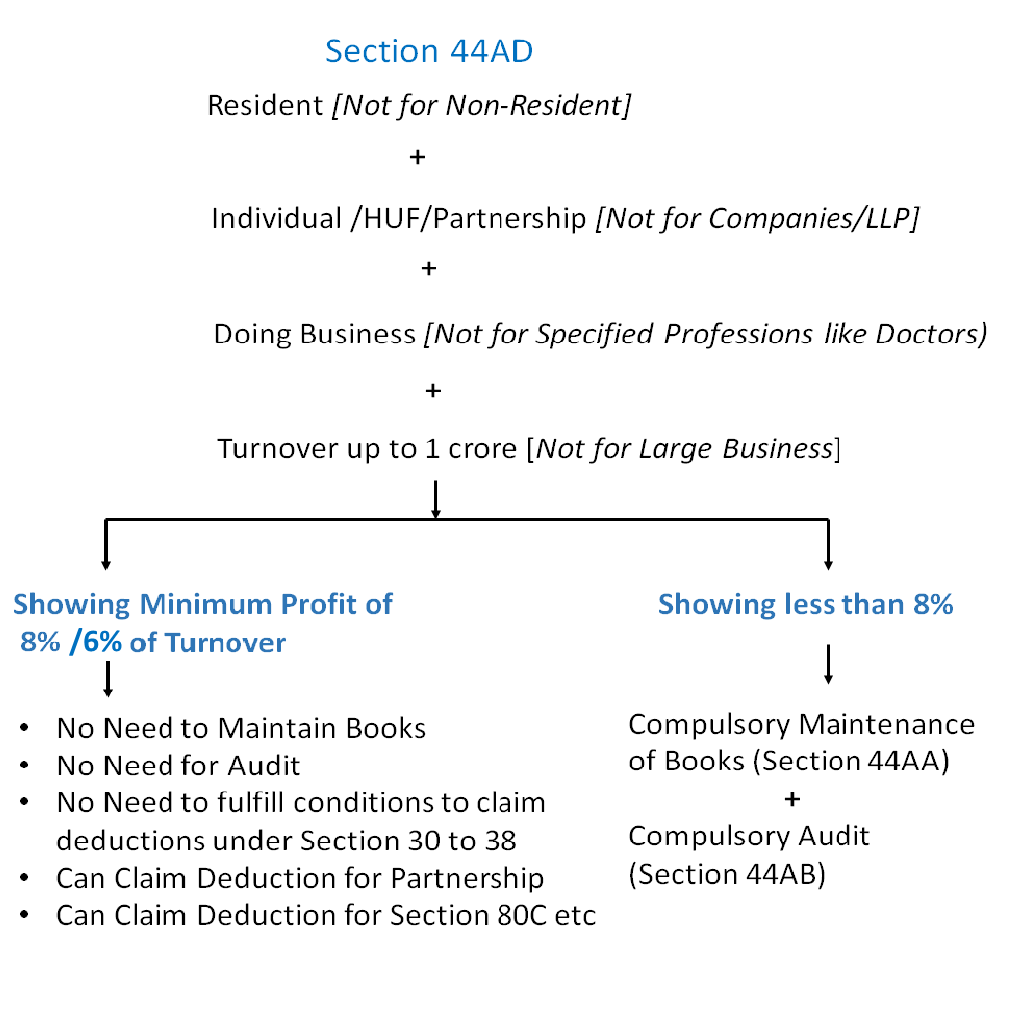

Section 44AD of the Income Tax Act provides for a presumptive taxation scheme for businesses. This scheme offers a simpler method for calculating taxable income by allowing taxpayers to declare their income at a prescribed rate based on turnover or gross receipts. By opting for presumptive taxation, eligible taxpayers can reduce their tax liability and simplify their tax compliance process, ultimately encouraging more individuals and businesses to come under the tax net. Here are the key points regarding the Presumptive Taxation Scheme for Business under Section 44AD:

- Eligibility: The scheme is available to resident individuals, Hindu Undivided Families (HUFs), and partnership firms (except Limited Liability Partnership firms) who are engaged in any business except the business of plying, hiring, or leasing of goods carriages referred to in Section 44AE. Income Tax Section 44AD of the Income Tax Act. Below are the types of tax assesses who can adopt the provisions of presumptive taxation scheme Under Section 44AD :

– Resident Individual tax payers

– Hindu Undivided Families

– Partnership Firm (except LLP or Limited Liability Partnership Firm)

Basic Condition for Presumptive Taxation Scheme Section 44AD :

- Turnover Limit: Businesses with a turnover of up to Rs. 2 crore in the financial year are eligible to opt for this scheme.

- Presumptive Income Rate: Under this scheme, the eligible taxpayer can declare income at a presumptive rate, which is 8% of the total turnover or gross receipts of the eligible business for the financial year.

- Maintenance of Books of Accounts: Taxpayers opting for this scheme are relieved from the requirement of maintaining regular books of accounts under Section 44AA. They are also exempt from getting their accounts audited under Section 44AB if the income is declared under this scheme.

- Disallowance of Deductions: Taxpayers availing the benefits of Section 44AD are not allowed to claim deductions under Sections 30 to 38 of the Income Tax Act, which includes deductions for expenses such as depreciation, rent, repairs, etc.

- Tax Audit Requirement: If the taxpayer opts for the presumptive taxation scheme under Section 44AD, they are not required to get their accounts audited under Section 44AB, irrespective of the turnover.

- Optional Scheme: It’s important to note that opting for the presumptive taxation scheme under Section 44AD is optional. Taxpayers can choose to avail of the benefits of this scheme if it is beneficial to them or opt for regular taxation as per the provisions of the Income Tax Act.

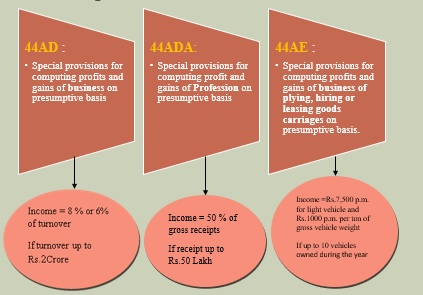

- The presumptive taxation scheme, available under Section 44AD for businesses and Section 44ADA for professionals, aims to streamline tax compliance for eligible taxpayers, particularly those with limited turnover or challenges in maintaining detailed books of accounts.

Overall, the Presumptive Taxation Scheme u/s 44AD aims to simplify the tax compliance process for small businesses by providing them with an easier method of computing their taxable income and reducing the burden of maintaining detailed books of accounts.

Income Tax Return filing u/s 44AD (Presumptive Income Scheme)

Under the Income Tax Act’s Presumptive Income Scheme, specifically Section 44AD, certain rules apply to the treatment of assets and deductions for taxpayers opting for this scheme:

Treatment of Fixed Assets: Construction equipment used for rental services can indeed be considered as fixed assets under Section 44AD. These assets contribute to the business’s operations and are essential for generating income.

Restrictions on Deductions: Taxpayers who choose to file returns u/s 44AD are not allowed to claim deductions provided under Section 30 to Section 38 of the Income Tax Act. This includes deductions for expenses such as depreciation, repairs and maintenance, rent, insurance, etc.

Presumptive Income Calculation: Instead of claiming actual expenses and deductions, the income for taxpayers under Section 44AD is calculated presumptively based on a fixed rate of 8% of the turnover or gross receipts of the eligible business for the year. This fixed percentage is deemed to cover all expenses, including depreciation.

Treatment of Depreciation: While no deduction is permitted for depreciation u/s 44AD, the Written Down Value (W.D.V) of any asset used in the business will be calculated as if depreciation has been allowed. This ensures that the asset’s value is accounted for in the business’s financial statements, even though no deduction is claimed for tax purposes.

Disallowance under Section 40(a)(ia): Taxpayers opting for the presumptive tax scheme u/s 44AD are not subject to disallowance u/s 40(a)(ia). This provision typically pertains to the disallowance of certain expenses or payments if they are not deducted or paid within the stipulated time frame.

These provisions aim to simplify the tax compliance process for small businesses and professionals while ensuring that their income is appropriately assessed and taxed under the presumptive income scheme.

Who is Exempt from advance tax payment?

– Resident senior citizens without business income.

– Those under presumptive taxation scheme (section 44AD or section 44ADA).

Question : We have been filing u/s 44AD for the past two years. Suppose a person didn’t file their return because their income was below the basic exemption limit in third year. However, the rule states that if someone opts for Section 44AD, they must file returns for five consecutive years. Will this trigger an audit when the person tries to file their income tax return next year?

Ans : We have been filing u/s 44AD for the past two years. Suppose a person didn’t file their return because their income was below the basic exemption limit in third year. However, the rule states that if someone opts for Section 44AD, they must file returns for five consecutive years. Will this trigger an audit when the person tries to file their income tax return next year?

Club Membership Fee – which ITR form applicable ITR-3 or ITR- 4?

Question: What about membership club that provides hotel to stay in every city like mahindra holidays saffire holidays For this we need ITR-3 or ITR- 4?

Responses:

For a membership club providing hotel services like Mahindra Holidays or Saffire Holidays, the choice between ITR-3 and ITR-4 depends on the nature of income and the club’s structure:

- ITR-3: This form is suitable if the club earns income from proprietary business or professional practices. ITR-3 is typically filed by individuals engaged in a broader range of business or professional activities.

- ITR-4: Designed for individuals and Hindu Undivided Families (HUFs) opting for the presumptive taxation scheme u/s 44AD or 44ADA. If the club chooses presumptive taxation and declares a minimum income of 8% of turnover, ITR-4 may be suitable.

If the club’s turnover is less than Rs. 2 crore and it opts for the presumptive taxation scheme u/s 44AD, it can declare a minimum net income of 8% of the turnover. In such cases, ITR-4 is typically used for filing returns. This simplifies the tax calculation process for the club, making it more convenient and reducing the compliance burden.

Query : Can we claim remuneration deduction if we are filing return u/s 44ad partnership firm after declaring income @ 8%.

Ans: Yes, Partnership firm can claim remuneration paid to partners as a deduction u/s 40(b) , even if it is filing its return under the presumptive taxation scheme u/s 44AD, subject to certain conditions. Key Points to Consider:

- Declaration of Income @ 8% or More: The partnership firm must declare income at 8% or more (or 6% in case of digital transactions) of the total turnover or gross receipts.

- Remuneration in Accordance with the Partnership Deed: The remuneration to partners must be authorized and specified in the partnership deed. If not specified in the deed, the remuneration cannot be claimed as a deduction. Partnership Firm must Ensure that Proper documentation of the partnership deed., Remuneration payment is within limits. And Other filing requirements u/s 44AD are met. In case the above conditions are satisfied, the remuneration deduction can be claimed without any issues.

- Limits as per Section 40(b): The remuneration paid to working partners should not exceed the following limits as prescribed under Section 40(b):

- On the first INR 3,00,000 of book profits: Maximum of INR 1,50,000 or 90% of the book profits, whichever is higher.

- On the balance of book profits: Maximum of 60% of the book profits.

- Book Profits Definition:

- Book profits mean Income computed under the head “Profits and Gains of Business or Profession” before deducting remuneration paid to partners.

- Presumptive Income u/s 44AD:When filing u/s 44AD, the declared presumptive income (8% or 6% of turnover) is considered as the book profit. The remuneration can then be calculated and deducted as per the limits u/s 40(b).

- Applicability of Section 44AD: The partnership firm can opt for presumptive taxation u/s 44AD, provided its turnover is less than ₹2 crore. Filing u/s 44AD simplifies tax compliance but does not restrict claiming eligible deductions such as partner remuneration

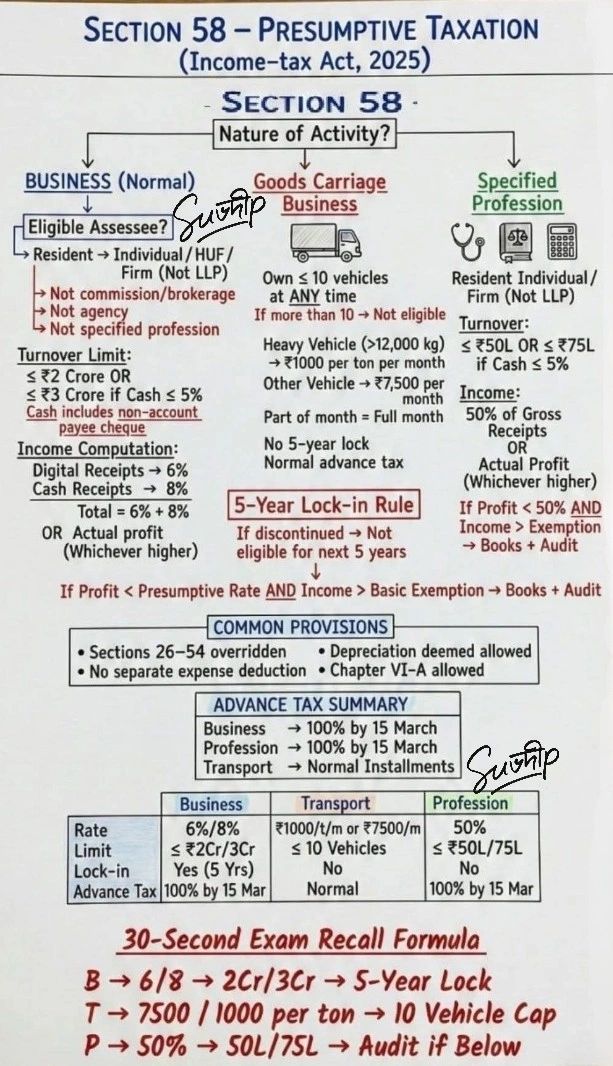

Presumptive Taxation – Section 58 (Proposed Income‑tax Act, 2025)

The Presumptive Taxation Scheme under Section 58 of the proposed Income Tax Act, 2025, aims to simplify tax compliance for small businesses and professionals. Under the presumptive taxation scheme, eligible taxpayers are not required to maintain detailed books of accounts. Instead, their taxable income is computed on a presumptive basis, i.e., as a fixed percentage of turnover or gross receipts.

The objective of the presumptive taxation scheme under Section 58 of the proposed Income Tax Act, 2025, is to reduce the compliance burden, simplify tax calculations, encourage voluntary tax compliance, and provide certainty and ease of filing for small taxpayers. The provisions under Section 58 of the proposed Income Tax Act, 2025, are aligned with the current presumptive taxation framework and are subject to enactment and final notification.

Section 44AD of Income-tax Act, 1961 Vs Section 58 of Income Tax Act, 2025

The Income Tax Act, 2025, effective from 1 April 2026, has substantially reorganized the presumptive taxation framework. One of the notable changes is the replacement of the standalone provisions of Sections 44AD, 44ADA, and 44AE under the Income-tax Act, 1961 with a consolidated Section 58. However, for small businesses, the fundamental tax benefits largely remain unchanged

Section 44AD:

Section 44AD of the Income-tax Act, 1961 provided a simplified taxation scheme for eligible small businesses by allowing them to declare income on a presumptive basis instead of maintaining detailed books of account. Key Features of Section 44AD

- Applicable to resident Individuals, HUFs, and Partnership Firms (excluding LLPs).

- Turnover limit:

- INR 2 Crore generally.

- INR 3 Crore where cash receipts do not exceed 5% of total turnover.

- Presumptive income:

- 8% of turnover received in cash.

- 6% of turnover received through banking or digital modes.

- Reduced compliance burden by exempting taxpayers from maintaining detailed books and audit requirements in certain cases.

What is Section 58 of the Income Tax Act, 2025?

The new Act consolidates the presumptive taxation provisions for:

- Small businesses (earlier Section 44AD)

- Goods carriage operators (earlier Section 44AE)

- Specified professionals (earlier Section 44ADA)

into a single provision Section 58. The objective is to create a structured, table-based framework that is easier to understand and administer.

Section 58 of the Income Tax Act 2025 is primarily a structural and compliance reform rather than a substantive tax reform. For taxpayers previously covered U/s 44AD, the turnover thresholds, presumptive rates of 6% and 8%, and eligibility conditions remain largely unchanged. The key change is that the presumptive taxation regime has been consolidated into a single, table-based provision, making the law simpler, more organized, and easier to administer. While the “math” largely remains the same, the “map” has changed significantly under the new legislation

Comparative Analysis: Section 58 vs 44AD

The govt. has intentionally preserved most substantive benefits available to small taxpayers. There is no change in presumptive rates. Business income continues to be computed at 6% of turnover received digitally. And 8% of turnover was received via other modes. Also, there is no change in turnover thresholds. The eligibility threshold remains INR 2 crore generally. And INR 3 crore where cash receipts do not exceed 5% of total receipts.

The scheme continues to Reduce compliance burden, encourage voluntary compliance and Minimize bookkeeping requirements, Promote digital transactions. Following are the Comparative Analysis Section 58 vs 44AD

| Particulars | Section 44AD (1961 Act) | Section 58 (2025 Act) |

| Provision | Separate section for small businesses | Consolidated presumptive taxation framework |

| Applicable from | Income-tax Act, 1961 | Income Tax Act, 2025 |

| Turnover Limit | INR 2 crore / INR 3 crore (digital receipts condition) | Same limit retained |

| Presumptive Rate | 6% digital receipts, 8% cash receipts | Same rates continue |

| Eligible Assessee | Resident Individual, HUF, Firm (non-LLP) | Same broad eligibility |

| Professionals | Covered separately under 44ADA | Merged into Section 58 |

| Transport Business | Covered separately under 44AE | Merged into Section 58 |

| Structure | Multiple sections | Single unified table-based provision |

| Terminology | Previous Year / Assessment Year | Tax Year |

| Compliance Framework | Spread across several provisions | Consolidated and simplified |

Major Changes Introduced U/s 58

Unified Presumptive Taxation Framework: Instead of referring to Sections 44AD, 44ADA, and 44AE separately, taxpayers now need to consult only Section 58 The provision classifies taxpayers through a table-based structure:

- Sl. No. 1 – Business taxpayers.

- Sl. No. 2 – Goods carriage operators.

- Sl. No. 3 – Specified professionals.

The Income Tax Act 2025 focuses on reducing cross-references and making provisions easier to read.

Many explanations and conditions that were previously scattered across the Act have now been integrated into the main provision.

Introduction of “Whichever is Higher” Language

- A noteworthy drafting change in Section 58 is the explicit inclusion of “profit claimed to have been actually earned, whichever is higher.” This clarifies that if actual profits are higher than presumptive profits, higher profits cannot be ignored merely by relying on presumptive rates.

- New Terminology: The new Act replaces Previous Year, Assessment Year with a single concept: Tax Year This change is intended to make the law easier for taxpayers to understand.

- Requirements relating to the maintenance of books and audits have been reorganized under the Income Tax Act 2025 and are linked with Section 62, reducing the need for extensive cross-referencing.

- For most small businesses using presumptive taxation: Same digital transaction incentive Easier navigation of law, Same tax relief benefits, , Same presumptive rates, Same turnover limits, Reduced complexity due to a single consolidated provision, No significant tax concession , enhancement, No major reduction in tax liability merely because of renumbering, No increase in presumptive thresholds,