Overview on Goods subject to reverse charge mechanism

Page Contents

Goods subject to reverse charge mechanism under GST:

The supply of goods subject to reverse charge mechanism (RCM) where the recipient is needed to pay GST, have been notified vide Central Board of Indirect Taxes & Customs Notification No. 4/2017 dated 28 June 2017 U/s 9(3) of the Central Goods and Services Tax Act, 2017.

List of Goods subject to reverse charge mechanism (RCM) under GST law:

The list of notified goods on which GST is needed to be paid under reverse charge is given below along with date from which reverse charge provisions are applicable on such goods. These goods are also notified for reverse charge under other Goods and services Tax Acts(s).

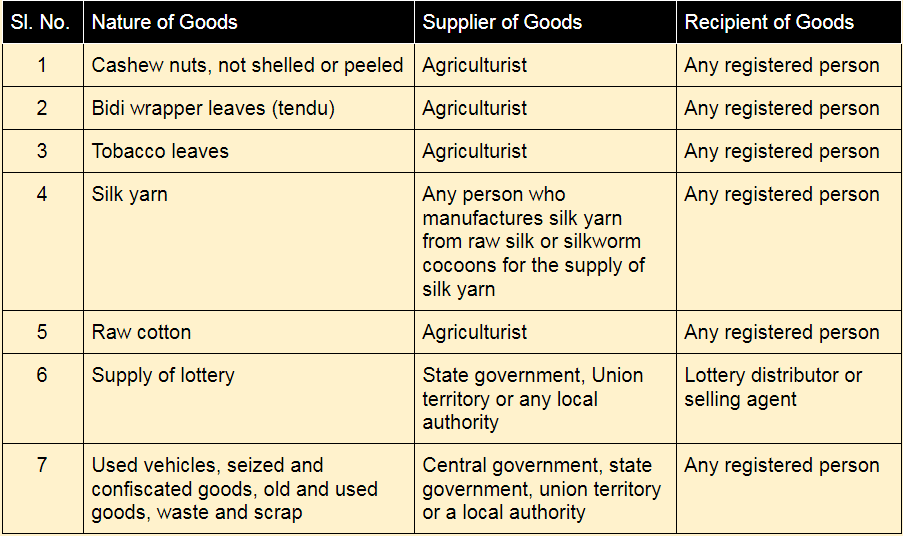

| Sr No. | Goods Description | Goods Supplier | Recipient of Goods |

| 1 | Cashew nuts, not shelled or peeled (RCM applicable from 01.07.2017). |

Agriculturist | Any registered person |

| 2 | Bidi wrapper leaves (tendu) (RCM applicable from 01.07.2017). |

Agriculturist | Any registered person |

| 3 | Tobacco Leaves (RCM applicable from 01.07.2017). |

Agriculturist | Any registered person |

| 4 | Raw cotton (RCM applicable from 15.11.2017 vide Central Board of Indirect Taxes & Customs N.N. 43/2017-CT(R) dated 14.11.2017) |

Agriculturist | Any registered person |

| 5 | Silk yarn (RCM applicable from 01.07.2017). |

Agriculturist | Any person who manufactures silk yarn from raw silk / silk worm cocoons for supply of silk yarn |

| 6 | Supply of lottery (RCM applicable from 01.07.2017). |

State Government, Union Territory or any local authority |

Lottery distributor or selling agent |

| 7 | Used vehicles , seized and confiscated goods, old and used goods , waste and scrap. (RCM applicable from 13.10.2017 vide Central Board of Indirect Taxes & Customs N.N. 36/2017-CT(R) dated 13.10.2017) |

Central / State Government, Union Territory or a local authority |

Any registered person |

| 8 | Priority Sector Lending Certificate (RCM applicable from 28.05.2018 vide Central Board of Indirect Taxes & Customs N.N. 11/2018-CT(R) dated 28.05.2018) |

Any registered person | Any registered person |

| 9 | Following essential oils other than those of citrus fruit namely: a) of peppermint (menthapiperita) b) Of other mints: Spearmint oil, watermint oil, Horsemint oil, Bergament oil. (RCM applicable w.e.f 01.10.2021 vide Central Board of Indirect Taxes & Customs N.N 10/2021-CT(R) dated 30.09.2021. |

Any unregistered person | Any registered person |

Brief discussion on some of the goods subject to RCM:

RCM on Purchase of goods from Agriculturist:

Out of eight goods wherein RCM is applicable on five goods , if purchased by GST Registered person from an agriculturist. So it is essential to understand the meaning of ‘Agriculturist’.

It should be noted that the term “agricultural” does not have a meaning under the GST law, but the term “agriculturist” does. Generally, the term “agricultural” is understood very broadly in commercial jargon to also cover post-harvesting activities. Horticulture, sericulture, and floriculture should all be included in further agriculture. It does not, But cover animal rearing.

RCM on Supply of lottery tickets

According to the as per Schedule III of the Central Goods and Services Tax Act, 2017. The ‘Lottery tickets’ is an actionable claim & is classified as ‘Goods’, under Goods and Services tax. But an actionable claim other than betting, lottery & gambling has been kept outside scope of supply.

So lottery tickets Sale would be considered to be the supply of taxable goods and will attract Goods and Services Tax.

Payment of GST under reverse charge:

- When a state govt is running a lottery, the state govt sells the tickets to a lottery distributor or selling agent. Reverse charge compels the selling agent to pay tax.

- Consequently, no tax is due when selling agent delivers such tickets to sub-agent/customer. Local sub-agents are likewise exempt from paying taxes. As a result, in the case of a state govt -run lottery, a tax is imposed at a single location under the reverse charge system.

- Nevertheless, in the case of lottery authorised by State Govt, the tax is to be paid by the lottery selling agent under the upfront charge. At each and every stage of supply, a tax is also paid.

- On all lotteries, there is an uniform GST rate of 28%.

RCM on Priority Sector Lending Certificate (PSLC)

What is the PSLC?

Priority Sector lending certificate are tradable instruments issued as certificates against priority sector lending by Nationalized or Private sector banks. The certificates help banks to meet their lending goals specified for the priority sector. Buyers of Priority Sector Lending Certificate are generally those Nationalized or Private sector banks who are not able to meet there needed target of lending priority sector. So, Nationalized or Private sector banks moving ahead of their targets issues Priority Sector Lending Certificate to non-achievers to balance the flow of lending and credit.

PSLC (Priority Sector Lending Certificate) are issued only between Nationalized or Private sector banks and the risk on account of credit made by over-performing Nationalized or Private sector banks, does not transfer with the issue of certificates to other Nationalized or Private sector banks.

Four specified types of PSLC include:

- Priority Sector Lending Certificate Agriculture: Priority Sector Lending Certificate issued for agriculture sub lending target.

- The Priority Sector Lending Certificate Micro Enterprises: Priority Sector Lending Certificate issued for Micro-enterprises sub lending target

- Priority Sector Lending Certificate Small and Marginal farmers: Priority Sector Lending Certificate issued for Small and Marginal farmers sub lending target

- The Priority Sector Lending Certificate General: Priority Sector Lending Certificate issued for correspondingly balancing the overall lending target.

Priority Sector Lending Certificate issued by Nationalized or Private sector banks does not transfer any risk, loan assets, interest or any right, hence, Priority Sector Lending Certificate does not fall under the definition of securities. They have an intrinsic value of their own and are to be taxed at general rates like other taxable goods under Goods and services Tax.

Levy of Goods and services Tax on Priority Sector Lending Certificate

- As per Central Board of Indirect Taxes & Customs Circular No.62/36/2018-GST dated 12.09.2018 clarified that Goods and services Tax on Priority Sector Lending Certificate starting from period 1 July 2017 to 27 May 2018 will be paid by the seller bank on a forward charge basis at the rate of 12 percentage. Whereas from 28 May 2018 onwards, the charge would be paid by the buyer bank on RCM

- The trade of Priority Sector Lending Certificate among Nationalized or Private sector banks will be considered as an Inter-state supply, so Integrated Goods and Services Tax is payable on such transactions.

New GST Update: on utilize amount in cash ledger in GST law

The option to utilize amount in cash ledger of one Goods & Services Tax Identification No by another Goods & Services Tax Identification No (entities having same Permanent Account No) by way of transfer through form PMT-09 has been made effective in Goods and Services Tax portal.