Optional vs Mandatory Table of GSTR 9 & GSTR 9C

Page Contents

All about Optional vs Mandatory Table of GSTR 9 & GSTR 9C

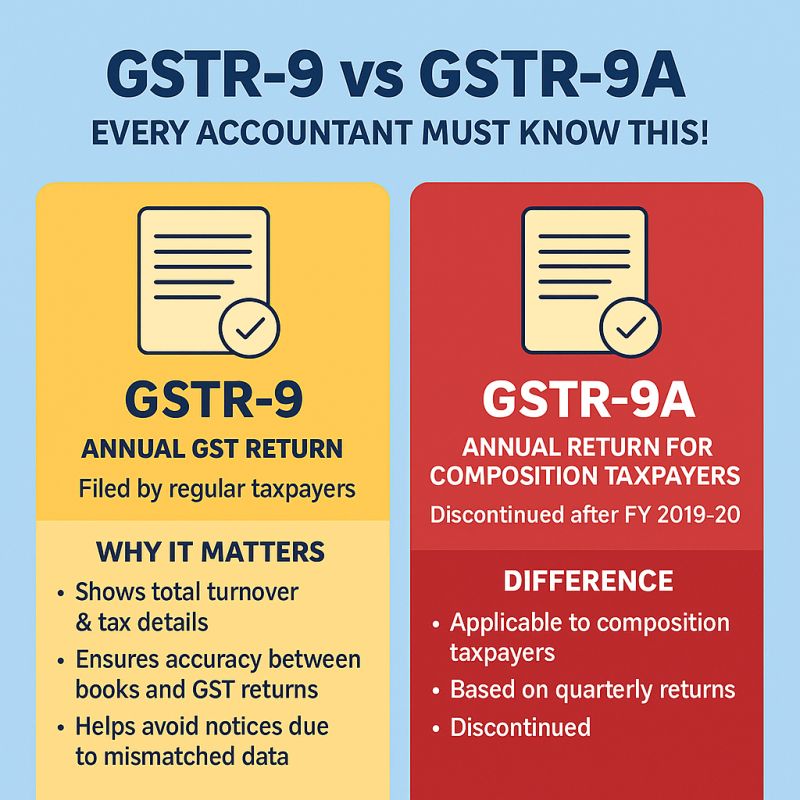

GSTR-9 & GSTR-9A — Every Accountant Must Know This!

- GSTR-9 : GSTR-9 is the Annual GST Return filed by regular GST Taxpayers. It gives a complete yearly summary of your Sales, Purchases, Input Tax Credit (ITC), Taxes paid. (Everything reported in GSTR-1 & GSTR-3B) Why it matters:

- Shows your total turnover & tax details

- Ensures accuracy between books and GST returns

- Helps avoid notices from mismatched data

- Due Date: 31st December of the next financial year

- Late Fees: INR 200 per day (INR 100 CGST + INR 100 SGST)

- GSTR-9A: GSTR-9A was the Annual Return for Composition Taxpayers (under the Composition Scheme). Discontinued after FY 2019–20, now replaced by GSTR-4 (Annual Return).

- The GSTR 9 and GSTR 9C forms for the FY 2023-24 are now available for filing, with several important updates. These changes streamline the process of filing GSTR 9 and GSTR 9C, particularly with the introduction of new rows for reporting e-commerce supplies under Section 9(5) and the removal of certain validation checks. The auto-population of data in Table 8A from GSTR-2B simplifies the reconciliation process, reducing the manual effort involved in filing.

- For detailed guidance, the summary of mandatory and optional tables for GSTR 9 & GSTR 9C should be referred to during filing. Below are the key points regarding mandatory filing requirements and important changes introduced in the forms:

- Under this blog you may find reconciliations and adopting best practices, businesses can minimize the risk of errors, improve their compliance process, and effectively address any departmental queries regarding mismatches in their GSTR filings.

Mandatory Filing Requirements of GSTR 9 & GSTR 9C forms

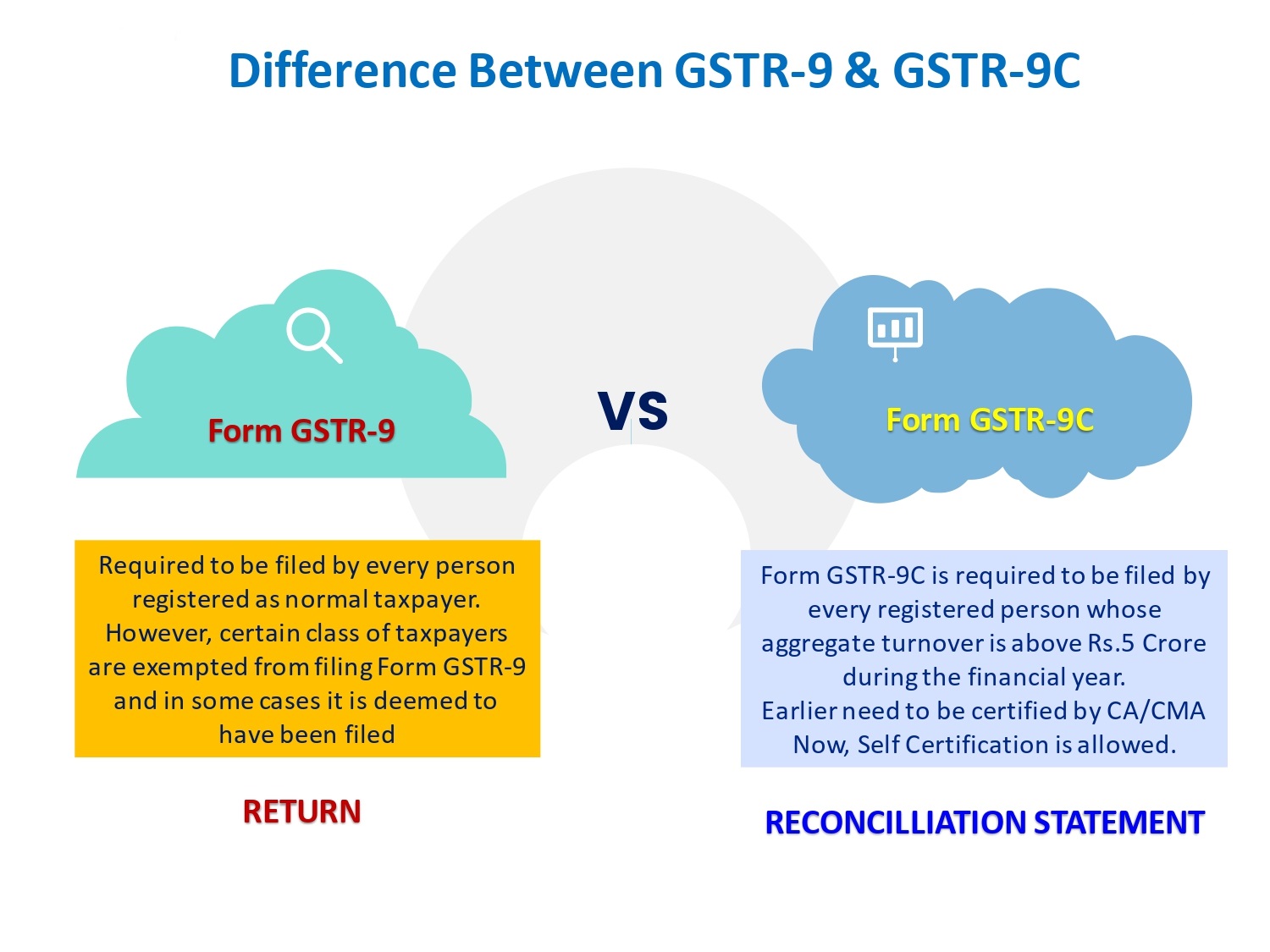

- GSTR 9: Mandatory if turnover exceeds ₹2 crore.

- In case of GSTR 9C: Mandatory if turnover exceeds ₹5 crore.

Important Changes in GSTR 9 and GSTR 9C for FY 2023-24:

Table 4:

- New Row G1: Added for reporting Section 9(5) supplies by the E-Commerce Operator (ECO).

- Subtotal in Row H: Updated to include values from Rows A to G1, covering all relevant details, including those from the new row.

In the Table 5:

- New Row C1: Inserted to report Section 9(5) supplies by the supplier.

- Total Turnover (Row N): Now excludes the impact of ECO supplies as reported in Table 4, Row G1, ensuring clarity in turnover calculations.

Table 6:

- Validation Check Removed: The requirement for CGST and SGST amounts to be equal in Rows 6K and 6L has been eliminated, offering greater flexibility in reporting.

In the Table 7:

- Validation Check Removed: Similar to Table 6, the validation requiring CGST and SGST to match has also been removed in Table 7.

Table 8:

- Table 8A Auto-Populated: From FY 2023-24 onwards, Table 8A will be auto-populated with data from GSTR-2B. The heading for Table 8A has been updated accordingly.

- In the Table 8B Heading Updated: The heading for Table 8B has been revised to reflect the changes in how data is presented and calculated.

Best Practices & Tips on minimizing the risk of errors, improve their compliance process,

- Turnover Reconciliation: Audited Financial Statements of GSTR 9 : Ensure reconciliation for all GSTINs of the business to align reported turnover across entities.

- Outward Taxes – Liability Reconciliation: Liability as per Books vs GSTR 3B + DRC-03 (if any). Ensure reverse charge mechanism (RCM) liabilities are included in the total.

- Rate-Wise Liability Reconciliation: Rate-wise liability as per workings should match rate-wise liability in the books. Any differences should be addressed before finalizing GSTR 9.

- GSTR 1 vs GSTR 3B: Perform reconciliation between GSTR 1 (outward supplies) and GSTR 3B to help populate GSTR 9 with accurate data.

- Inward Taxes – ITC Reconciliation: Reconcile credit as per books with credit as per GSTR 3B to identify any excess ITC claims or missed credits. Missed ITC can be claimed in October 3B returns before 30th November 2023.

- Closing Balance Reconciliation: Reconcile the cash and credit balances as per books with the balances on the GST portal for all GSTINs.

- Rectifications Beyond the Deadline: Identify and note any rectifications or modifications made after the 30th November timeline.

- Invoice-Level Reconciliation: Perform invoice-level reconciliations, comparing data from GSTR 2A/2B with the books. This is essential to correct errors and provide accurate information to the department.

- Maintain Linked Workings: Ensure that GSTR 9 & 9C workings are linked to relevant data sources (avoid manual keyed-in workings). Maintain a detailed record of ITC claimed, reversed, and re-claimed as per the conditions of Section 16.

- Amendment Register: Keep an outward supply register with original and amended values to help in filling Table 4 & Table 5 of GSTR 9.

- Invoice-Level ITC Reconciliation: Compare GSTR 2B with ITC as per books for Table 8 disclosure in GSTR 9 to ensure accurate reporting of credits.

- Treatment of Unclaimed Credits: For credits not claimed due to non-matching with GSTR 2A/2B, consider passing them as an expense in the books of FY 2022-23. Verify options for recovery from vendors.

Annual GST Management Report:

- Prepare an “Annual GST – Management Report” which includes: A folder containing final workings and filed GSTR 1, 3B, GSTR 9 & 9C. Reconciliations for outward, inward supplies, and RCM, with a high-level overview.

- Reasons for variances and actions taken. Summary details of additional liabilities detected and payment documentation. Suggestions for improving internal accounting, processes, and reporting going forward.

GSTR 9 Vs. GSTR 9C

Optional vs Mandatory Table of GSTR 9 & GSTR 9C

GST Advisory – File Pending GST Returns Before Expiry of 3 Years

- As per the Finance Act, 2023 (8 of 2023) dated 31st March 2023, & implemented with effect from 1st October 2023 vide Notification No. 28/2023 – Central Tax dated 31st July 2023, GST taxpayers shall not be allowed to file GST returns after the expiry of three years from the due date of furnishing such GST Return.

- This restriction applies to returns under Section 37 – Outward Supply (GSTR-1, GSTR-1A), Section 39 – Payment of liability (GSTR-3B, GSTR-4, GSTR-5, GSTR-5A, GSTR-6), Section 44 – Annual Return (GSTR-9, GSTR-9C), Section 52 – Tax Collected at Source (GSTR-7, GSTR-8)

- GST Taxpayers will be barred from filing the above returns after three years from their respective due dates. This restriction will be implemented on the GST portal starting October 2025 tax period. Meaning, any GST Return whose due date was three years back or earlier, and is still pending as of October 2025, cannot be filed thereafter.

- GSTN had already issued an advisory in this regard on 29th October 2024. All taxpayers having pending GST returns older than 3 years must file them before October 2025 to avoid permanent closure of the GST Return filing facility.

Changes to GSTR-9 & GSTR-9C now enabled on the GST Portal in FY 2024-25

GSTR-9: Key Enhancements & Clarifications

Exemption Taxpayers with turnover up to INR 2 crore are exempt from filing GSTR-9.

New Tables Introduced

- 4G1 & 5C1: Section 9(5) e-commerce transactions.

- 6A1 & 6A2: ITC bifurcation between previous and current FY.

- 6M: Transitional ITC via ITC-01, ITC-02, ITC-02A.

- 7A1 & 7A2: Rule-wise ITC reversals (Rules 37A, 38).

- 8H & 8H1: IGST credit split across FYs.

- Table 9: Tax payable vs paid.

- Tables 12 & 13: Mandatory for deferred ITC and reversals.

Auto-Population Logic

- Based on GSTR-1/1A/IFF, GSTR-2B, and GSTR-3B.

- Amendments in supplier returns affect Table 8A (Excel vs Online view may differ).

- Reclaimed ITC due to Rule 37/37A is excluded from Table 6A1 and reported in Table 6H.

ITC Reporting Scenarios

- Same FY Claim-Reverse-Reclaim: Use Tables 6B, 7A–7H, and 6H.

- Previous FY ITC reclaimed in current FY:

- Rule 37/37A: Report in Table 6H.

- Other reasons: Report in Table 6A1.

- Current FY ITC reclaimed in next FY:

- Rule 37/37A: Report in next FY’s Table 6H.

- Other reasons: Report in Table 13 of current FY and Table 6A1 of next FY.

Table 8 Specifics

- 8A: Auto-populated from GSTR-2B.

- 8C: Only for missed ITC claimed in next FY (not for reclaimed ITC).

- 8D: Delinked from Table 6H to avoid mismatches.

- 8H1: New row for IGST credit claimed in next FY.

GSTR-9C: Key Enhancements

- Marketplace Supplies: Section 9(5) disclosures by supplier and ECO.

- New Tax Rate Rows: Includes 6% and “Others”.

- Table 16 & 17: Tax on erroneous refunds, demands, and late fee.

- Payment Flexibility: Additional liability can be paid via cash or ITC.

Late Fee Clarification

- GSTR-9: Late fee under Section 47(2) if filed after 31st Dec 2025.

- GSTR-9C: Late fee calculated from date of GSTR-9 filing or due date, whichever is later.

- Auto-calculated and split between GSTR-9 and GSTR-9C.

Details of key enhancements & clarifications under GST 9 and 9C are mentioned in the attached presentation : https://carajput.com/archives/changes-to-gstr-9-and-gstr-9c-now-enabled-on-the-gst-portal.pdf