Online Filing of Form 10F Without PAN for Non-Residents

Page Contents

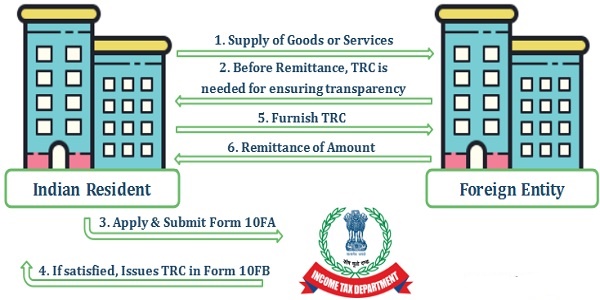

How to Obtain a Tax Residency Certificate (TRC):

A Tax Residency Certificate (TRC) is essential for determining treaty benefits under DTAA. It provides conclusive evidence of a taxpayer’s residency status and eligibility for tax relief and benefits specified in the tax treaties. By submitting a valid TRC, taxpayers can ensure they are not subjected to double taxation and can benefit from lower withholding taxes and other provisions available under the applicable DTAA. Once issued by the competent authority of a foreign country, a TRC serves as conclusive evidence of the taxpayer’s residency status and eligibility for treaty benefits. By obtaining a TRC, taxpayers can navigate international tax laws more effectively, ensuring compliance while taking advantage of treaty benefits.

Benefits of Tax Residency Certificate (TRC)

A Tax Residency Certificate (TRC) offers several advantages for taxpayers, especially in the context of international taxation and compliance.

- Helps Assessees Avoid Double Taxation It confirms an assessee’s tax residency status, ensuring their income is not taxed twice in different countries.

- Acts as a Proof of Residence for Financial Transactions. This includes international trade, investments, and opening bank accounts, thereby facilitating smoother and quicker processes. Used in financial transactions and account openings

- Facilitates Tax Treaty Benefits , its allowed Access to lower withholding taxes on specific incomes.

- Serves as a Document for Tax Compliance. They help establish the taxpayer’s residency status, which is crucial when filing tax returns or dealing with financial institutions and tax authorities. This Avoids Double Taxation: Ensures income is taxed in only one jurisdiction.

- Simplifies Administrative Tax Procedures. This ensures accurate tax treatment and reduces the likelihood of disputes with foreign tax authorities. Reduces complexities and disputes in tax procedures.

- Provides Transparency in International Transactions This facilitates smoother financial dealings across borders. Essential for meeting international tax obligations. Enhances credibility and smoothness in international transactions.

Tax Residency Certificate (TRC) for Indian Residents & Non-Residents

For Indian Residents:

- Form No. 10FA: Submit to the Assessing Officer.

- Form No. 10FB: Issued by the Assessing Officer upon approval.

Application Process:

- Indian residents must apply for a TRC using Form No. 10FA.

- Submit the application to the Assessing Officer.

- The Assessing Officer will review the application and, if satisfied with the particulars, will issue a TRC in Form No. 10FB.

Important Points while considering filling of Tax Residency Certificate:

- A TRC issued by a competent authority is the primary document used to establish the residency status of the taxpayer for DTAA purposes.

- It demonstrates that the taxpayer has complied with the residency requirements necessary to obtain the tax benefits.

- Ensure all mandatory details are included in the TRC to avoid rejection. Ensure all the necessary documents are complete and submitted on time to avail the benefits under the DTAA provisions efficiently. Taxpayers must ensure that their TRC is valid and updated to continue availing treaty benefits.

- Non-resident taxpayers must adhere to the electronic filing requirement for Form 10F.

- No other document can replace the TRC for availing the reduced TDS rate. Without a TRC, taxpayers may not be able to claim the benefits offered under the DTAA.

- Submit a fresh tax declaration (DTAA Annexure and Form 10F) and TRC to the bank upon the expiry of the previous documents.

- The reduced TDS rate will be applicable for the period mentioned on the TRC.

For Non-Resident Taxpayers:

- TRC from Country of Residence: Must contain specified information.

- Source: Non-resident taxpayers must obtain a TRC from the government of their country or specified territory of residence.

Obtaining a TRC:

- Form 10F: Filed electronically in India. Form 10F must be filed electronically with the Income Tax Department in India.

- Along with Form 10F, submit the TRC, Certificate of Incorporation (for entities), and address proof. Accompanying Documents: Include TRC, Certificate of Incorporation (if applicable), and address proof.

- Required Information on TRC:

- Taxpayer’s name

- Taxpayer’s status (individual, company, firm, etc.)

- Nationality (for individuals) or country of incorporation/registration (for entities)

- Tax identification number or unique number assigned by the country of residence

- Taxpayer’s residential status

- Validity period of the certificate

- Taxpayer’s address during the applicable period

- Additional Details Required:

- Non-resident taxpayers must provide the following information along with their TRC:

- Key person details

- Address proof

- Father’s name (for individuals)

- Tax identification number

- Email ID

- Contact number

- Non-resident taxpayers must provide the following information along with their TRC:

Online Filing of Form 10F Without PAN for Non-Residents

Non-residents who wish to claim tax treaty benefits with India must file Form 10F along with a Tax Residency Certificate (TRC). However, the requirement for electronic filing of Form 10F posed a challenge for those without a PAN. Recent updates have provided a pathway for these non-residents to comply without needing to obtain a PAN.

Registration Process for Non-Residents Without PAN

- Go to the e-filing portal: Income Tax Portal.

- Click on the ‘Register’ option. Choose the category ‘non-residents not having a PAN and not required to have a PAN’.

- Enter details like name, date of incorporation, tax identification number, status, and country of residence. Provide details of the key person (name, date of birth, designation, and Tax Identification Number).

- Enter contact details including email address and mobile number, which will be verified via OTP.

- Upload required documents such as TRC, address proof, identification proof, and any other necessary documents.

- Create a password for the e-filing account, after which a User ID will be generated.

Filing Form 10F Online

- Use the User ID and password to log into your account on the income tax portal.

- Navigate to Form 10F, Go to the ‘e-file’ tab. Select ‘Income Tax Forms’ and then ‘File Income Tax Forms’.

- Choose Form 10F from the list. Select the relevant Assessment Year (AY) and click ‘Continue’. Provide the necessary details and attach the TRC.

- Save the draft and preview the form. Verify the form using an electronic verification code (EVC) sent to the registered mobile number and email ID .Once verified, click ‘Submit’.

- Save the acknowledgment for your records.

Non-residents not required to obtain a PAN can now file Form 10F online through a streamlined process. This involves registering on the income tax portal, providing necessary details, and submitting Form 10F with the required documents, including the TRC. This development simplifies compliance and ensures that non-residents can claim tax treaty benefits without needing a PAN.

NRIs residing in countries with or without DTAA with India have access to tax relief provisions under the Income Tax Act. While those in treaty countries can benefit from specific provisions outlined in the DTAA, NRIs in non-treaty countries can still claim relief under Section 91 of the Income Tax Act. It’s essential for NRIs to understand the relevant provisions and seek professional advice to optimize their tax obligations and minimize the risk of double taxation.

PAN Transfer Consequences

Be at easy! Get a hassle-free and easy ITR filing experience by hiring a CA right away. To manage your taxes and receive assistance with tax matters, simply schedule a consultation with a Tax Advisory Service.