Overview TCS on Liberalized Remittance scheme

Page Contents

Key Takeaways About the TCS On Liberalized Remittance scheme (LSR) Applicability

Concept of Liberalized Remittance scheme as per Reserve Bank of India Regulation :

- AD’s Liberalized Remittance/ Transfer Scheme may openly allow Remittance/ Transfer s of up to USD 2,50,000 (April-March) per Financial Year to resident individuals for any approved current or capital account transaction or a combination of both.

- The Liberalized Remittance/ Transfer Scheme is not applicable to corporations, partnership businesses, HUFs, trusts, etc.

- Remittance/ Transfer s under the Scheme may be accumulated in respect of members of the family required to comply with its terms and conditions by individual members of the family.

- Fortunately, for capital account activities such as opening a bank account/investment/purchase of property, clubbing is not allowed by other family members if They are not the co-owners / co-partners in foreign bank accounts/investment/property.

Benefits of Liberalized Remittance scheme

The Liberalized Remittance scheme framework gives Indian residents the freedom to

- Pay for international education, medical care, and other personal expenses.

- Make global investments for diversification.

- Transfer funds abroad for family maintenance.

- Repay foreign loans or meet other financial obligations overseas.

Liberalized Remittance Scheme Eligibility Requirements

Liberalized Remittance scheme is available to Resident individuals, including minors and students. A valid PAN, Indian bank account, and passport are mandatory. Transactions can be for Education, Travel, Maintenance of relatives, Investments (shares, mutual funds, property abroad), Medical treatment and Business or personal purposes.

Liberalized Remittance scheme Annual Remittance Limit

Under Liberalized Remittance scheme, a resident individual may remit up to USD 250,000 per financial year. This covers Education, Medical treatment, Travel, Gifts, Employment/emigration, Overseas investments (equity, debt, real estate) and Maintenance of relatives

Prohibited Transactions under Liberalized Remittance scheme

Remittances cannot be used for Margin trading, Lottery winnings, Banned/illegal activities, Purchase of real estate abroad on behalf of someone else and Trading in foreign exchange abroad

Activities that are prohibited in compliance with rule 3 of the foreign exchange management act, 1999:

- In case of Remittance/ Transfer from winnings of lotteries.

- If Remittance/ Transfer of revenue or some other pleasure from racing/riding etc.

- Transfer / Remittance for lottery ticket purchases prohibited/proscribed magazines, football games, sweepstakes, etc.

- Payment of the export commission for equity investment in joint ventures / wholly owned subsidiaries of Indian companies abroad.

- Remittance/ Transfer of dividends from any company to whom a dividend balancing provision applies.

- In case Payment of commissions for exports under the Rupee State Credit Route, with the exception of commissions of up to 10% of the invoice value of tea and tobacco exports.

- In case Payment for telephones connected to ‘Call Back Systems.’

- Remittance/ Transfer of interest income on funds deposited in the Non-Resident Special Rupee (Account) Scheme.

Activities that require prior approval by the central government (see Schedule II Rule 4)

- Cultural trips

- Advertisement in global print media by the State Government and its Public Sector Undertakings for objectives other than development of tourism, foreign investment, and international bidding (exceeding USD 10,000)

- Transfer / Remittance of freight chartered by a PSU vessel

- Import payment by Govt. Department or PSU on the basis of c.i.f. (i.e. not based on f.o.b. and f.a.s.)

- Multi-modal transport operators that transfer Remittance/ Transfer s to their agents In abroad

- Remittance/ Transfer of transponder hiring charges by (a) TV networks (b) Internet Service Providers

- In case Remittance/ Transfer of charges for the detention of containers in excess of the rate stated by the Director-General of Shipping

- Technical partnership deal Remittance/ Transfer s where royalty payments exceed 5% on local revenues and 8% on exports and lumpsum payments exceed USD 2 million

- If Remittance/ Transfer for P & I Club membership

- Once Remittance/ Transfer by a person of prize money/sponsorship for sports activities in abroad other than International / National / State Level sports bodies of prize money/sponsorship of sports operation overseas, if the sum concerned reaches USD 100,000.

More read for related blogs are: New revised TDS/TCS due date for filing Return and Payment for the year 2020

- Moreover, a resident cannot give a foreign currency as a gift to another resident for the credit of a foreign currency account kept abroad by the latter under the Liberalized Remittance Scheme.

- The scheme should not be used to make remittances/transfers for any prohibited or immoral activities such as margin lending, lotteries, etc.

Prohibition on the drawing of foreign exchange :

Prohibition on the drawing of foreign exchange by any person for the following purposes:

- The transaction specified in Schedule I;

- Travel to Bhutan and/or Nepal;

- The transaction with a person who is resident in Nepal or Bhutan.

Such that the prohibition referred to in clause (c) may be excluded by the Reserve Bank of India , pursuant to such terms and conditions as may be considered appropriate by special or general order.

- All such transactions not otherwise permitted under The Foreign Exchange Management Act and those of a margin or margin call Remittance/ Transfer form to overseas exchanges / overseas counterparties are not permitted under the Liberalized Remittance/ Transfer scheme.

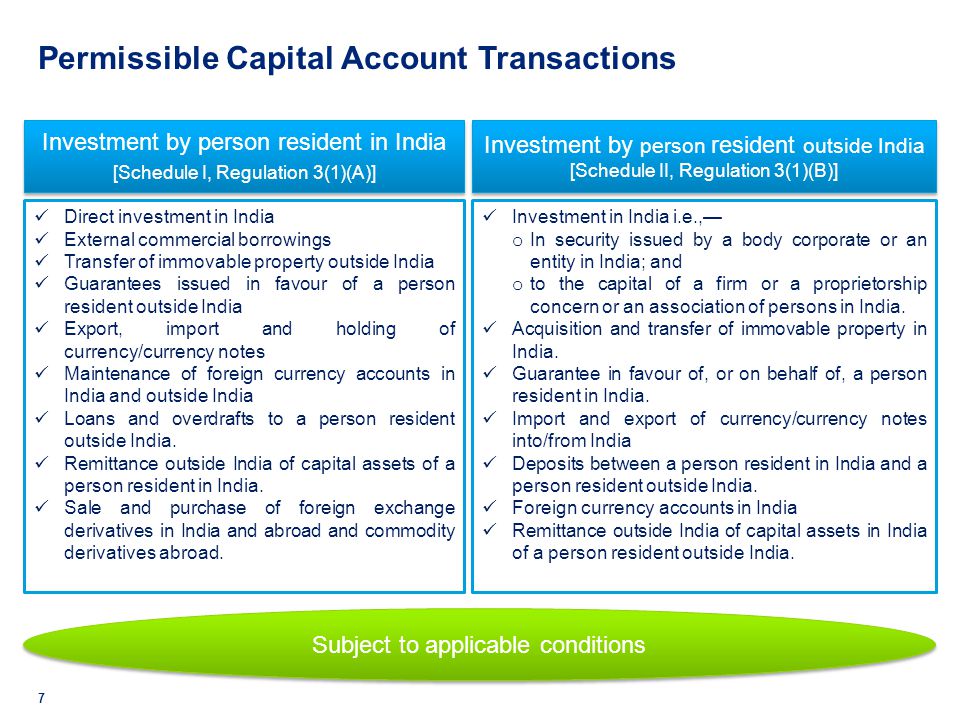

- Allowable Current account transactions: The cap of USD 2.50,000 per Financial Year (FY) under the Scheme also contains/subsumes Remittance/ Transfer s for current account transactions (i.e. private visits; gifts/donations; work from abroad; emigration; preservation of close relatives abroad; business trips; medical care in abroad; studies abroad) available to the resident individual in India foreign exchange not more than USD 250,000 by getting prior approval from RBI.

- Private visits

- Gift / donation

- Moving abroad for jobs/employment

- Emigration

- Maintenance of close relatives in Abroad

- Business trip

- Medical care in abroad

- Resources for students to complete their studies abroad.

Also Read key features of TCS on goods sale section-206c

Permitted transactions of the capital account:

The permitted transactions of the capital account by an individual under the Liberalized Remittance Scheme are

- New Opening a bank account for foreign currency account abroad.

- Investment in abroad: purchase and retention of stock in both listed and unlisted foreign companies or debt instruments; purchase in qualified stock of a foreign company for hold the position of director; purchase of stocks of a foreign company for professional services rendered or in exchange of remuneration of the Director; investment in Mutual Funds units; Venture Capital Funds; promissory note, unrated debt securities;

- Setting up of Wholly Owned Subsidiaries and Joint Ventures (w.e.f. 5th Aug 2013) for the bonafide industry outside India, according to the Reserve Bank of India terms and conditions.

- Extending loans to non-resident Indians (NRIs) who are relatives, including loans in Indian Rupees as specified in the Companies Act, 2013

- To encourage capital account Remittance/ Transfer s under the Liberalized Remittance Scheme, banks do not provide any kind of credit facilities to resident individuals.

TCS on an Amount for remittances transactions under LRS Scheme.

TCS on a sum for remittance transactions under Liberalized Remittance Scheme.:

According to the amendment pursuant to section 206C of the Finance Act 2020, an approved dealer who collects a sum for remittances under the Liberalized Remittance Scheme shall be liable for TCS transactions under the Liberalized Remittance Scheme.

- tax collection at source will be effective 1 October 2020 for all Liberalized Remittance Scheme transactions, including international debit card transactions.

- Underpayments are within the limits of the tax collection at source applicability-

- Liberalized Remittance Scheme forwarding transactions via the Bank branch or bank Online.

- Foreign Currency Demand Draft or cash issuance from a domestic resident account for the purpose of the Liberalized Remittance Scheme.

- International transactions on Debit Card Transactions (including transactions on international traders or platforms providing Dynamic Currency Conversion-DCC Transactions)

- Transfers from domestic resident customers to Liberalized Remittance Scheme NGO account (Loan to NRI or Gift to NRI)

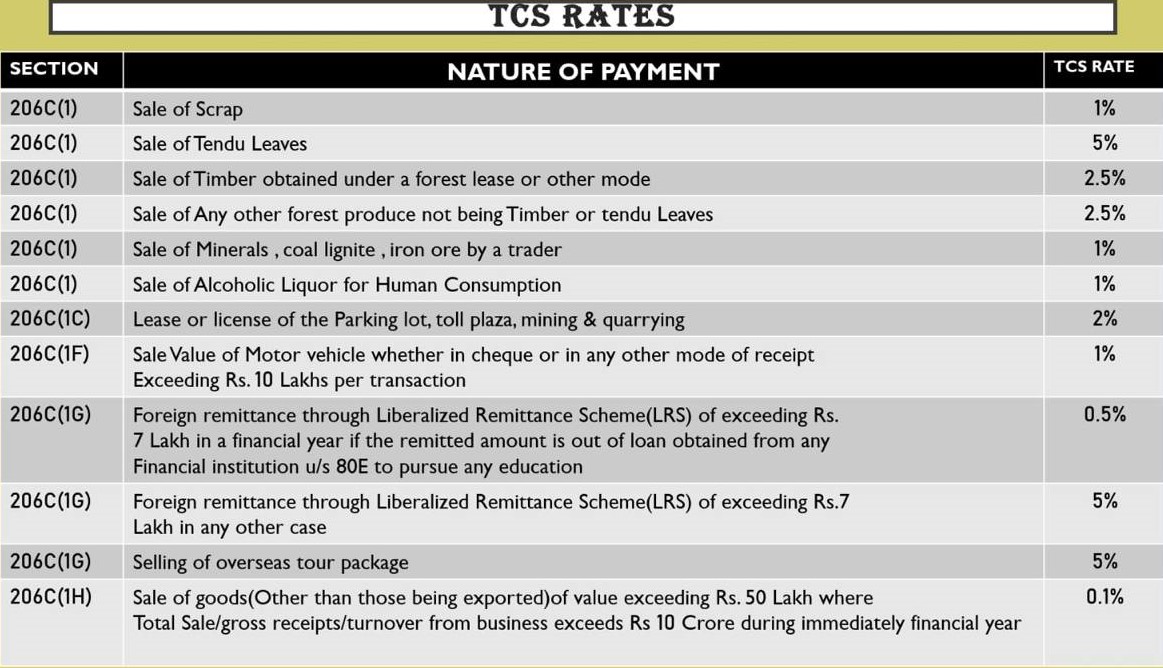

Tax collection at source charging grid for Liberalized Remittance Scheme remittances and transactions

| Liberalized Remittance Scheme Purpose/Type of transaction | Applicable of Tax collected at source |

| 1. Remittances under Liberalized Remittance Scheme Purpose S0306 – 2. International transactions on Debit Cards (including Dynamic Currency Conversion – DCC transactions) and 3. Other travel including holiday trips and payments for settling international credit card transactions. |

5% of the transaction/remittance amount |

| Liberalized Remittance Scheme Purpose S1107 Studies abroad and S0305 Travel for education, where the source of funds is Education loan | 0.5% of the remittance amount above INR 7 lacs during the financial year. |

| Any Other Liberalized Remittance Scheme purposes | 5% of the remittance amount, above INR 7 lacs during the financial year. |

Note:- It is to ensure that the account is properly financed to cover the cost of the remittance, the Tax collected at source cost, the remittance charges, the related bank fees as well as other taxes/charges as applicable. In the case of insufficient balances, payments will not be processed.

Changes have been made to the Source Tax Collection (TCS) provision for international remittances made during the Union Budget 2020-21. Please find below the list of the amended provision;

- The TCS clause will now be effective from 1 October 2020 instead of 1 April 2020.

- On the basis of the recent clarification, TCS shall refer to sums greater than INR 7 lakh in the financial year and not to the total sum.

- In situations where the sum is charged for continuing education through a loan from any financial institution, the rate of TCS shall be 0.5 percent above the sum of INR 7 lakh.

In summary

- Residents can easily enter into a transaction of up to USD 2,50,000 under the Reserve Bank of India’s Liberalized Remittance Scheme for a financial year from April 1 to March 31.

- According to the Foreign Exchange Management Act, a resident individual can engage in current and capital account transactions, or a combination of both, as prescribed by the Reserve Bank of India.

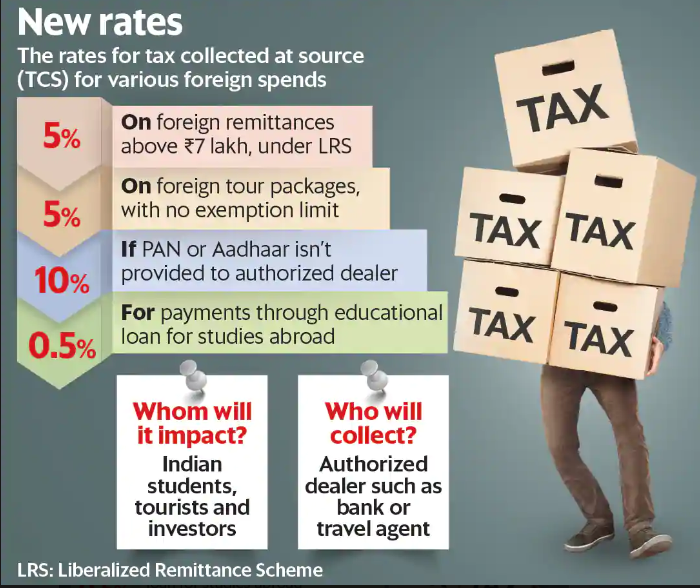

- Foreign exchange transactions of up to Rs. 7,00,000 in a financial year will be tax-free as of October 1, 2020. In the hands of a person, any amount above Rs. 7,00,000 is subject to TCS at a rate of 5% and 0.5 percent in the case of an education loan transaction.

- Individuals can file an Income Tax return to receive a tax refund or to reduce the amount of tax collected against their overall tax due. There is no minimum threshold for collecting Taxes on tour packages.

Liberalised Remittance Scheme – Updated Overview (Budget 2025 & 2026)

The Liberalised Remittance Scheme is an RBI initiative that allows resident Indian individuals to remit up to USD 250,000 per financial year for various permitted current and capital account transactions. These include education, travel, medical treatment, gifts, maintenance of relatives, and overseas investments. Key Updates: Budget 2025 & Budget 2026

Budget 2025 Update – Higher TCS-Free Threshold

- The TCS exemption limit on foreign remittances under Liberalized Remittance Scheme has been raised from ₹7 lakh to ₹10 lakh per financial year.

- No TCS will be levied on Liberalized Remittance Scheme transactions up to ₹10 lakh.

- Education remittances from educational loans (from recognised financial institutions):

0% TCS, irrespective of amount. - For remittances exceeding ₹10 lakh (except education loan remittances):

5% TCS applies. - The TCS paid can be claimed as refund/adjustment in ITR, visible in Form 26AS.

Budget 2026 Update – Major TCS Reductions

- Liberalized Remittance Scheme for Health & Education – TCS reduced from 5% → 2%.

- Overseas Tour Packages – TCS reduced from 5% & 20% → flat 2%, with no minimum threshold.

Liberalized Remittance Scheme Applicability for NRIs

The Liberalized Remittance Scheme scheme is only for resident Indians. NRIs cannot remit under Liberalized Remittance Scheme because they cannot hold resident savings accounts. However, they can remit funds abroad outside Liberalized Remittance Scheme, through the following accounts:

NRI Remittance Rules

| NRI Account | Remittance Limit | Notes |

|---|---|---|

| NRO | Up to USD 10,000 per year | For taxable Indian income; repatriation requires documentation (Form 15CA/CB). |

| NRE | No limit | Fully repatriable funds. |

| FCNR | No limit |

Latest Overview on RBI Guidelines for Outward Remittance

Outward remittance refers to the transfer of funds from an Indian bank account to a foreign bank account. The Reserve Bank of India regulates all outward remittances under the Foreign Exchange Management Act and the Liberalised Remittance Scheme for resident individuals. Under these guidelines, outward remittances may be made through A bank-issued demand draft in the sender’s or beneficiary’s name, or Transfer through authorised dealer (AD) banks and Maintaining a foreign bank account abroad (permitted under The Foreign Exchange Management Act for specific purposes). As per Reserve Bank of India norms following Steps for Making an Outward Remittance.

1. Select an Authorised Dealer (AD) Bank

Choose a bank branch that is an authorised dealer in foreign exchange. Only authorised dealer Category-I banks are permitted to process Liberalized Remittance Scheme related outward remittances.

2. Carry Your PAN Card

A valid PAN is mandatory to initiate any remittance under Liberalized Remittance Scheme.

3. Complete KYC & AML Compliance

Banks must follow KYC (Know Your Customer) norms, AML (Anti-Money Laundering) guidelines and CFT (Combating the Financing of Terrorism) checks. These verifications are compulsory before processing any foreign exchange transaction.

5. Fill and Submit Form A2

Form A2 is required for purchasing foreign exchange or remitting funds abroad.

It includes Purpose of remittance (as per The Foreign Exchange Management Act purpose codes), Amount of foreign exchange required and Declaration of Liberalized Remittance Scheme compliance. Banks cannot process the remittance without this form.

6. No Credit Facility Allowed for Liberalized Remittance Scheme Transfers

As per Reserve Bank of India regulations Banks are prohibited from extending any credit facilities to residents for making remittances under Liberalized Remittance Scheme. This means You cannot remit money abroad using overdrafts, loans, or credit lines offered by banks. Only freely available funds in your bank account can be used for outward remittances.

Frequently Asked on TCS on Liberalized Remittance Scheme.

Questions: 1. what is the effective date of introduction of the tax implications?

The effectiveness of the Tax collected at the source clause on international remittances is updated from 1 April 2020 to 1 October 2020.

Question:2. What all transactions will be affected by this Tax collected at source requirement?

- All remittances in excess of INR 7 lakh in the financial year under the Liberalized Remittance Scheme will be liable for 5 percent of TCS, except where the remittance is for education paid out through a loan from any financial institution.

- The rate would then be decreased from 5% to 0.5%.

- The exclusion from TCS for remittances abroad under Liberalized Remittance Scheme for sums just under INR 7 lakh in the financial year would not apply if the sum is charged for the purchase of the overseas tour program kit.

Questions: 3. Can GST be applied to the 5% TCS collected?

No GST would refer to the tax collected by the TCS. However, GST will refer to the conversion & remittance service fee of the currency.

Questions: 4. what are the various reasons for which the tax collection applies?

Tax would apply to all remittances from India that come under the Liberalized Remittance Scheme of Reserve Bank of India.

Questions: 5. what are the various Purpose permitted under Liberalized Remittance Scheme?

Following are the purposes permitted under Liberalized Remittance Scheme.

- Private visits to any country (excluding Nepal and Bhutan)

- Donation or charity;

- Study abroad

- Moving overseas to work

- Emigration:

- Maintenance of loyal family members abroad

- Travel for business, or attending a conference or advanced training, or meeting expenses for meeting medical expenses, or checking abroad, or accompanying a patient going abroad for medical treatment/check-up;

- Expenditures for medical care overseas

- Any other current account transaction not protected in The Foreign Exchange Management Act, 1999.

Questions: 6. what are the various permissible capital account transactions by an individual for purposes permitted under Liberalized Remittance Scheme?

Permissible capital account transactions by an individual under Liberalized Remittance Scheme are:

- Investments abroad – acquisition and holding of shares in both listed and unlisted foreign companies or debt instruments; 5 acquisition in qualified shares of a foreign company for the role of the director; acquisition of shares of a foreign company for professional services rendered or in lieu of remuneration of the director; investment in units of mutual funds, venture capital funds;

- Establishment of wholly-owned subsidiaries and joint ventures (with effect from 05 August 2013) outside India for a bonafide company subject to the terms and conditions set out in Notification No FEMA.263 / RB-2013 of 5 March 2013;

- to extend loans, namely loans in Indian Rupees, to non-resident Indians (NRIs) who are relatives.

- the opening of foreign currency accounts with a bank abroad;

- purchase of foreign property;

Questions: 7. What’s Dynamic Currency Conversion (DCC)?

- Many international traders offer the ‘Dynamic Currency Conversion’ facility – which enables customers to make purchase payments directly in their home currency (i.e. Indian Rupees for cards issued in India).

- This service is provided by selected international merchants or websites. The final transaction amount (as determined by the merchant / Dynamic Currency Conversion service provider) must be checked by you before the payment is made. Depending on the sum given by the merchant, Citi will charge you the final amount (Indian Rupees).

- The conversion procedure, the exchange rate, and any markup applied in such cases shall be decided, as the case may be, by the applicable merchant or Dynamic Currency Conversion service provider.

- If we do not opt for Dynamic Currency Conversion, you will be billed in local currency by the merchant. If the local currency is not USD, then the transaction is translated first from the local currency to $ then from $ to INR.

Popular blog:-