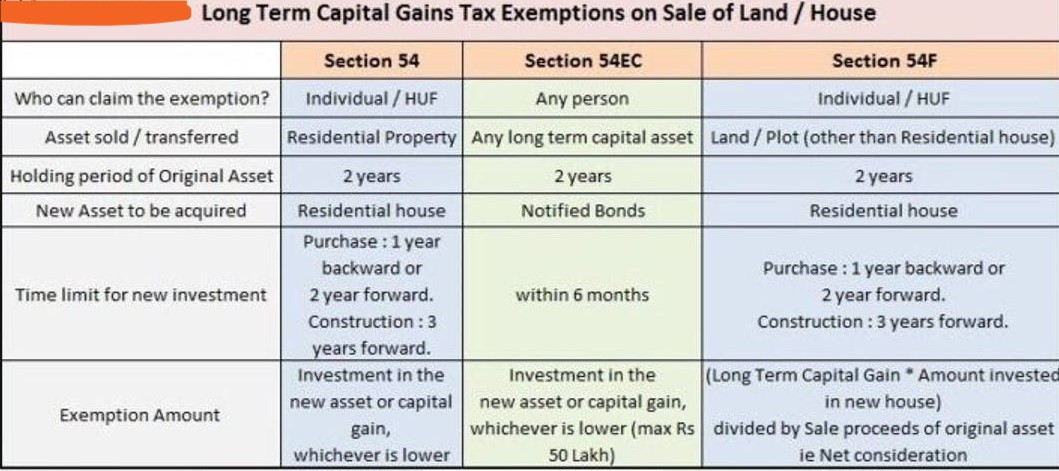

Is Deduction u/s 54 & 54F can be claimed simultaneously

Page Contents

Is deduction u/s 54 & 54F of the Income Tax Act be claimed simultaneously?

- Under Section 54 & Section 54F investment in residential house has to be made within a period of 2 years from the date of sale of respective capital assets. A longer period of 3 years is available if you go for self-construction or booking an under-construction residential house.

- In the matter of Venkata Ramana Umareddy Vs Dy. CIT (ITAT Hyderabad) decision made by the Income Tax Appellate Tribunal : There is no specific bar in simultaneously claiming the exemption under both sections.

- We can conclude that a Taxpayer can claim income tax deduction u/s 54 & Section 54F simultaneously subject to that above has been acquired in conditions fulfilment of stipulated under the said respective sections.

What will be nature of Capital Gain where Depreciable Asset is sold after a period of 36 months ?

- Unser Section 50 of Income Tax Act being a Deeming provision, its Operation is restricted, not to allow indexation advantage When taxpayer sold the depreciable Assets, Even if Holding period is more than thirty Six months.

- Once Depreciable Asset was hold for more than thirty Six months, Nature of Capital Gain is Long Term ( No Indexation benefit), and Tax to be deposited under section 112 @ 20%.

- Taxpayer can entitled to claim advantage of Section 54EC, Section 54 & Section 54F , from that LTCG.

Section 54F exemption not allowed if assessee purchased two non-adjacent flats in same residential society: HC

The High Court’s ruling reaffirms that Section 54F of the Income Tax Act applies to the purchase or construction of “a residential house”, and this phrase should be interpreted strictly as a single residential unit. The court emphasized that if the assessee purchases two separate flats — even within the same residential society — which are not adjacent or combined into one unit, the benefit of Section 54F will not apply. The High Court held that the phrase ‘a residential house’ in Section 54F of the Income Tax Act should be interpreted strictly to mean a single residential unit

Key Highlights of the Ruling: Section 54F One Flat One Exemption

- Strict Interpretation of “a Residential House”: The phrase “a residential house” under Section 54F has been interpreted to mean a single residential unit. If multiple independent residential units are purchased, the exemption cannot be claimed for both.

- Non-Adjacent Flats: The exemption will not apply to two flats unless they are combined into a single functional unit. Non-adjacent flats are treated as distinct residential properties, disqualifying the assessee from availing the exemption for both.

- Implication for Taxpayers: Assessees claiming Section 54F benefits must ensure that the property purchased constitutes one single residential house. The intent and functionality of the property as a single unit will be crucial in determining eligibility for the exemption.

This judgment highlights the need for taxpayers to carefully evaluate the nature and structure of the residential property purchased when seeking benefits under Section 54F.

Capital Gain Exemptions comparison summary

| Section | Sale Asset | Purchase Requirement | Time Period | CGAS Required |

|---|---|---|---|---|

| 54 | Residential house (Individual or HUF only) | Residential house | Within 1 year before or 2 years after sale | ✅ Yes |

| 54B | Agricultural land | Agricultural land (rural) | Entire sale consideration to be reinvested | ✅ Yes |

| (2nd 54B) | Any urban land | Purchase within 3 years | Land/building held for 2 years prior to sale | ✅ Yes |

| 54D | Industrial undertaking | Purchase within 3 years | Used for re-establishing industrial undertaking | ✅ Yes |

| 54EC | Any Long-Term Capital Asset (LTCA) | Invest in specified infrastructure bonds (e.g. NHAI/REC) | Within 6 months; bonds must be held for minimum 5 years | ✅ Yes |

Notes:

-

CGAS = Capital Gains Account Scheme: Required if the capital gain is not fully utilized before the due date of ITR filing.

-

Section 54 is for individuals/HUFs only, on sale of residential property and reinvestment into another residential property.

-

Section 54B applies only to sale of agricultural land and reinvestment into agricultural land.

-

Section 54D pertains to compulsory acquisition of industrial undertakings.

-

Section 54EC allows exemption by investing in notified bonds (up to ₹50 lakhs per financial year).

Popular blog:

- All about the Income taxation on capital gain

- Provision-of-capital-gains-charts

- Govt needed to introduce changes in NSP Budget 2021

- All about the Income taxation on capital gain

- Deduction u/s 80CCD of Income Tax Act, 1961

- All about the Income taxation on capital gain

- Delay in the deposit of Employer provident fund during the lockdown

- Aware of the penalty of Section-234f for late filing of ITR

For query or help, contact: singh@carajput.com or call at 9555555480