Income Tax Savings through House Property

Page Contents

INCOME TAX SAVINGS THROUGH HOUSE PROPERTY

Does your home, saving your income tax? Buying a house for self occupation can be biggest tax saving instrument. It saves your income tax in two ways. You can save maximum Rs 75750 per year on your home.

Introduction:

There are two main benefits which are available under Income Tax Act, 1961 in relation to Purchase or Construction of House Property which are described as under:

- Deduction of Interest on Capital borrowed for purchase or construction of House Property under Section 24 (b) of the Income Tax Act, 1961. (Interest paid by house owner on housing loan)

- Principle amount paid towards Housing loan for purchase or construction of House Property under Section 80 C of the Income Tax Act, 1961.

- The amount stamp duty/ Registration charges paid while acquiring a property will be allowed deduction U/s 80C.

Interest Paid towards housing loan:-

The house property has been acquired, constructed, repaired, renewed or reconstructed with borrowed capital, the amount payable towards interest on borrowed capital is allowed as deduction under u/s 24(b) of the Income-tax act.

- We have to note here Interest payable on borrowed capital is allowed (Interest paid is irreverent here).

- In case of under-construction property, Interest will aggregate from the date of borrowing till the end of the previous year prior to the previous year in which the house is completed and allowed in five successive financial years starting from the year in which the acquisition or construction was completed.

- In case Assesses is the owner of more than one residential property, he may exercise an option to treat any one of the houses to be self-occupied and the other houses will be deemed to be let out and the annual value of such house will be determined as per Section 23(1)(a) of the Income Tax Act, 1961.

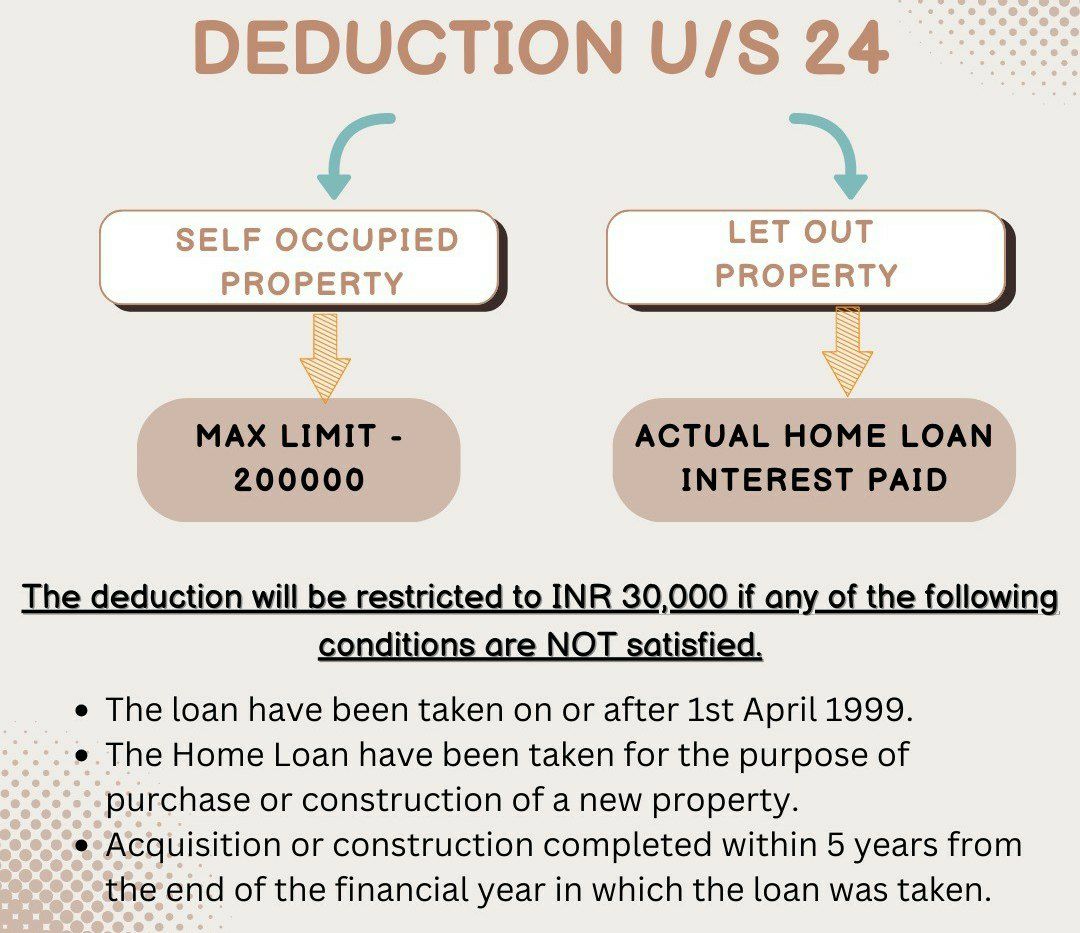

How much Interest Deduction allowed U/s 24(b) :-

In case of self occupied house:-

(a) In case property is acquired or constructed with capital borrowed on or after 01-04-1999 and such acquisition or construction is completed within 3 years of the end of the financial year in which the capital was borrowed:

Minimum of Actual Interest payable or Rs 1, 50,000/- .

(b) In case property is acquired or constructed with capital borrowed

Minimum of Actual Interest payable or Rs 30,000/- .

In case of Rental / Deemed to be let out House Property.

Interest payable on barrowed capital for the previous year is allowed as deduction under U/s 24(b).

Principle Amount paid towards Housing Loan:-

Any payment made for purchase or construction of a residential house property which is chargeable to tax under the head “Income from House Property” towards any installment or part payment due to any Bank, Financial Institution, Company or Co-Operative Society towards the cost of the house property allotted to him is allowed as deduction U/s 80 C of the Income Tax Act, 1961 to the extent of Rs. 1,00,000 along with other Specified Investments mentioned under Section 80 C of the Income Tax Act, 1961.

Stamp Duty and Registration Charges for a home:-

The amount you pay as stamp duty or registration fee when you buy a house can be claimed as deduction under section 80C in the year of purchase of the house.