How can I file ITR, claim TDS refund for a deceased parent?

Page Contents

Filing ITR & Claiming TDS Refund for a Deceased Parent

Obtain Proof That You Are the Legal Heir

Apply through the local tehsildar/municipal corporation office for a legal heir certificate. Submit an application form, death certificate, PAN of the deceased, your PAN, address proof, bank account details, and documents proving your relationship. Once verified, the tehsildar issues a legal heir certificate.

Register as Legal Heir on the Income Tax Portal

-

Log in to your own account on the Income Tax e-filing portal.

-

Request registration as a representative assessee.

-

Select “Deceased (legal heir)” and upload required documents:

-

Death certificate

-

PAN of deceased

-

Legal heir proof

-

Your PAN, ID & address proof

-

Bank account details for refund

-

-

Once the income tax department approves, you can file ITR on behalf of your parent.

File the ITR & Claim Refund

-

File the ITR as usual (for the income earned till the date of death).

-

Refund (if any) will be credited to the legal heir’s validated bank account.

-

If the original bank account of the deceased is closed, file a “Refund Re-issue Request” with your bank account details.

Income Received After Death

Any income after the date of death (e.g., interest credited later) is taxable in the hands of the legal heir. If TDS is deducted post-death, you can claim it in your own ITR.

Multiple Heirs?

-

Registration of one legal heir is sufficient for filing. If there are multiple heirs, consensus is needed to avoid disputes. Keep legal documents ready for verification. No separate prior intimation to the Income Tax Department is needed apart from registering as a legal heir on the portal.

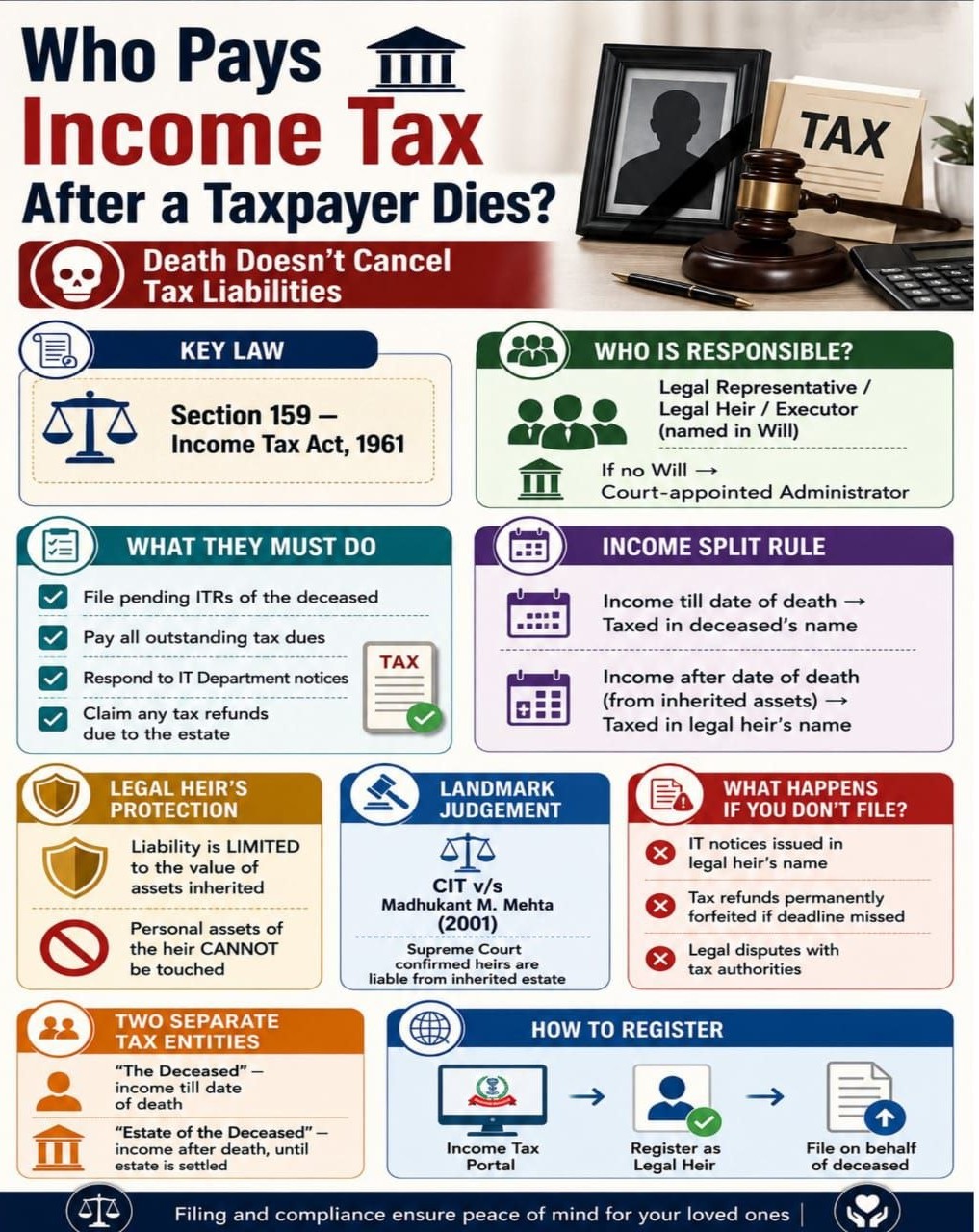

Who Pays Income Tax After a Taxpayer Dies?

Who Pays the Tax?

Legal Representative / Legal Heir: As per Section 159 of the Income Tax Act, 1961, the legal heir (executor, administrator, or family member who inherits the estate) is responsible. This could be a spouse, children, or Any person managing the estate.

What Taxes Are Payable?

The legal heir must handle:

- Tax on Income Earned Before Death: Income from April 1 to the date of death. A return must be filed in the name of the deceased (e.g., “Late Mr. X, through legal heir Mrs. Y”)

- Tax on Income Earned After Death: Income generated from the inherited assets (rent, interest, etc.) This is taxed either in the hands of the legal heir OR in the estate (if the the estate is under administration).

Extent of Liability:

The legal heir is liable only to the extent of the estate inherited. They are not required to pay from their personal funds. The legal heir must register as a legal heir on the income tax portal, file an ITR on behalf of the deceased, pay any outstanding taxes, and claim refunds (if any).

Special Case:

Will / Executor: If a will exists, the executor handles tax matters. During administration, income may be taxed as “Estate of the deceased.” Filing ensures closure of PAN records; the taxpayer must avoidance of notices/penalties. Taxpayers always segregate the following:

- Pre-death income → deceased ITR

- Post-death income → heir/estate ITR

The legal heir pays the deceased person’s income tax, but only from the assets inherited, not from personal funds.