Taxation of Share Transaction & Disclosing F&O Income

Page Contents

Important Points for Taxation of Share Transaction & Disclosing F&O Income

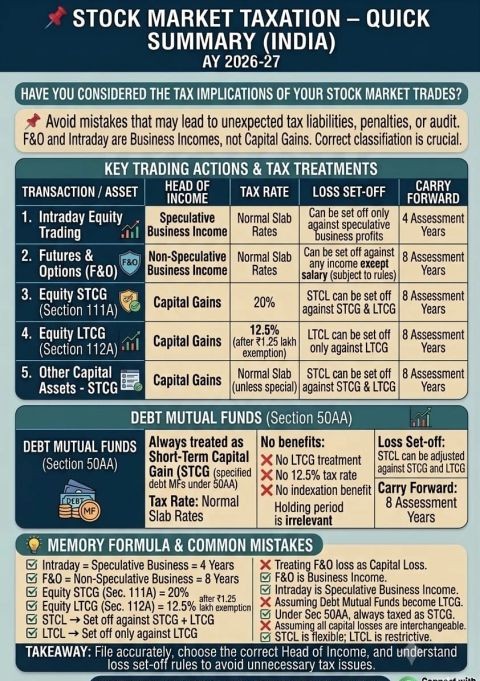

- The income from these transactions should be reported under the head “Income from Business or Profession” in the Income Tax Return. Taxpayers engaged in these activities may be liable to pay advance tax if their tax liability exceeds ₹10,000 in a financial year

- Income from Futures and Options (F&O) transactions must be reported in ITR-3, whether the taxpayer is an individual, Hindu Undivided Family (HUF), or a company. ITR-3 is designed for individuals and HUFs having income from profits and gains of business or profession, which includes income from F&O trading.

- F&O income is considered business income and must be reported under the head “Profits and Gains from Business or Profession”. ITR-3 also allows you to report other incomes such as Salary income, Income from house property, Income from other sources (like interest income, dividends, etc.)

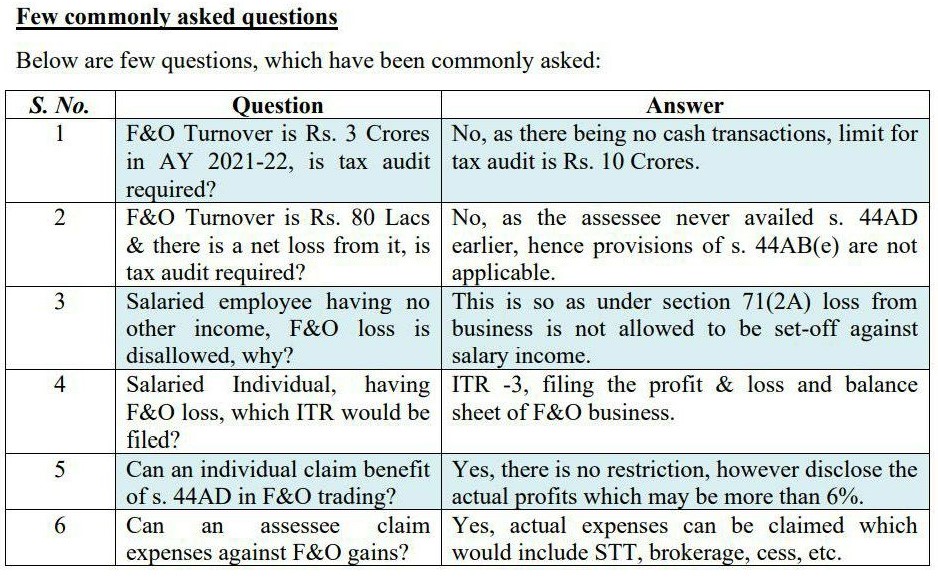

- If your total income exceeds a certain threshold, you may be required to maintain books of accounts and have them audited by a Chartered Accountant. You can deduct expenses directly related to your F&O trading, such as brokerage fees, internet charges, and other related expenses. If your turnover from F&O trading exceeds ₹10 crore (from AY 2021-22) or you opt for the presumptive taxation scheme under section 44AD and your total income exceeds the basic exemption limit, you

F&O Taxation

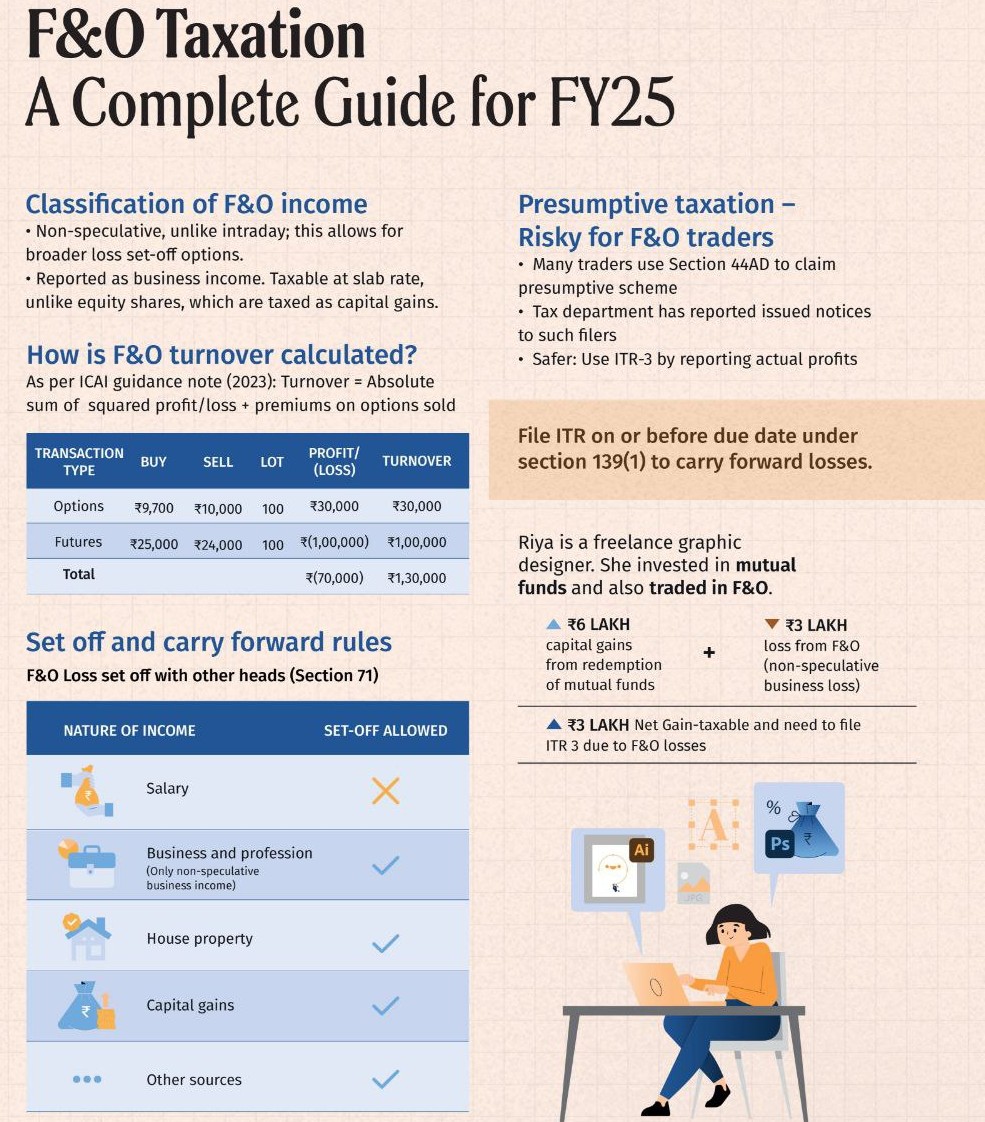

Classification of F&O income

-

Treated as non-speculative business income (unlike intraday trading).

-

Allows broader loss set-off options.

-

Taxable at slab rate — not under capital gains.

How is F&O turnover calculated?

As per ICAI : Turnover = Absolute sum of profit/loss + Premiums on options sold

Example:

| Transaction Type | Profit/(Loss) | Turnover |

|---|---|---|

| Options | INR 30,000 | INR 30,000 |

| Futures | (INR 1,00,000) | INR 1,00,000 |

| Total | (INR 70,000) | INR 1,30,000 |

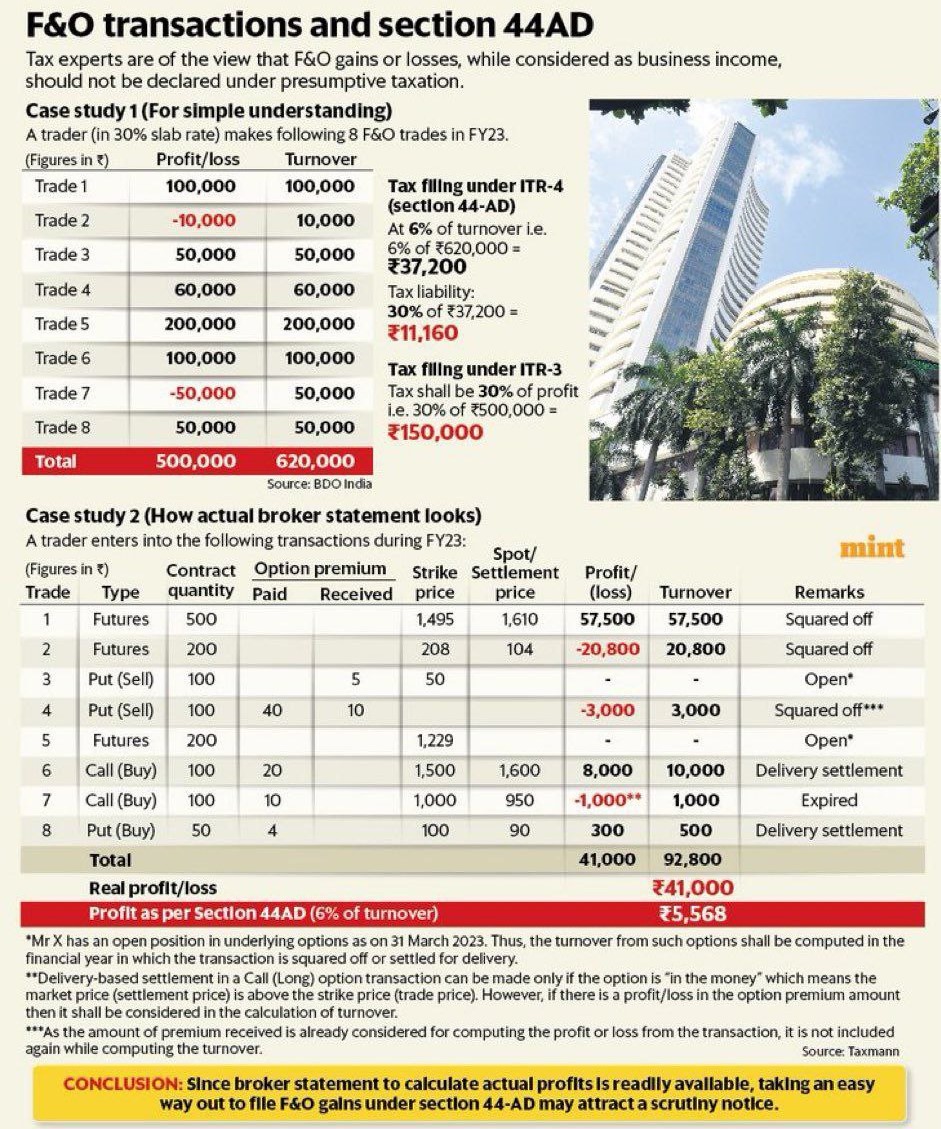

Presumptive taxation (Section 44AD) – Risky for F&O traders

-

Some traders claim 44AD presumptive scheme — but tax department has issued notices. Safer to report actual profits and file ITR-3.

Set-off and carry-forward rules (Section 71) – F&O loss can be set off against:

| Nature of Income | Set-off Allowed? |

|---|---|

| Salary | Not allowed |

| Business & Profession (non-speculative) | Allowed |

| House Property | Allowed |

| Capital Gains | Allowed |

| Other Sources | Allowed |

File ITR on or before due date (u/s 139(1)) to carry forward losses.

CBDT Clarification on treatment of Share Sale as Business Income or Capital Gains Income

- CBDT Clarification: Income Taxpayers can choose to treat income from listed shares as either business income or capital gains. Once chosen, the treatment must be consistent in subsequent years unless circumstances change significantly. The chosen method will be accepted by the Assessing Officer (AO), reducing disputes.

- the CBDT Circular No. 6/2016 (Dated 29 February 2016) : Business Income: If the taxpayer treats listed shares as stock-in-trade, income will be treated as business income, irrespective of holding period. & Capital Gains: If treated as capital gains, the AO will not dispute the classification for shares held over 12 months.

- Non-Speculative Nature of F&O Transactions: According to Section 43(5)(d) of the Income Tax Act: Transactions in trading of derivatives (as per clause (ac) of Section 2(20) of the Securities Contracts (Regulation) Act, 1956) carried out on a recognized stock exchange are not deemed speculative. This means F&O transactions are classified as non-speculative business income, not speculative.

- Treatment of Unlisted Shares: Income from the transfer of unlisted shares is taxed under ‘Capital Gains’ regardless of the holding period, as per CBDT circular dated 2 May 2016, to avoid disputes.

- Potential Reclassification: There is market speculation that the government may consider reclassifying F&O turnover from non-speculative business income to speculative income. This would have significant implications for how these transactions are taxed and reported.

Calculation of Turnover from F&O Trades

- Previous Method: Earlier, the turnover was computed as the sum of the absolute profit and the premiums earned from options writing.

- New Method (from AY23) Absolute Profit method : The total of all profits and losses from F&O trades, where losses are also added to the profits to calculate the total turnover.

Deductible Expenses:

Taxpayers can claim deductions for expenses related to F&O business, such as: Brokerage fees, Interest on loans availed for trading, Electricity costs, Internet charges.

Other Consideration

- Typically, you will need to use ITR-3 for reporting income from F&O trading as business income. Keep detailed records of all transactions, including profits, losses, and all related expenses. If the total turnover exceeds the specified limit, an audit may be required under Section 44AB of the Income Tax Act.

- Ensure accurate calculation of total turnover, deductible expenses, and net income from F&O trading for correct tax liability assessment. Follow the prescribed method for calculating turnover and ensure consistent reporting across assessment years.

- If the F&O transactions are considered as a business, the taxpayer is required to maintain proper books of accounts as per the provisions of the Income Tax Act. If the turnover exceeds the prescribed limit under Section 44AB, the accounts must be audited by a Chartered Accountant. Under Section 44AD, taxpayers with a turnover of up to INR 2 Cr can opt for presumptive taxation and declare 6% or 8% of the turnover as income, provided they are eligible and not engaged in speculative transactions.

Summary Share trading or F&O transactions Treatment

| Criteria | Business Income | Capital Gains | |

| Volume/Frequency | High (e.g., day trading, F&O trading) | Low to moderate | |

| Intent | Short-term profit | Long-term investment | |

| Expenses Deduction | All business-related expenses | Transfer-related expenses only | |

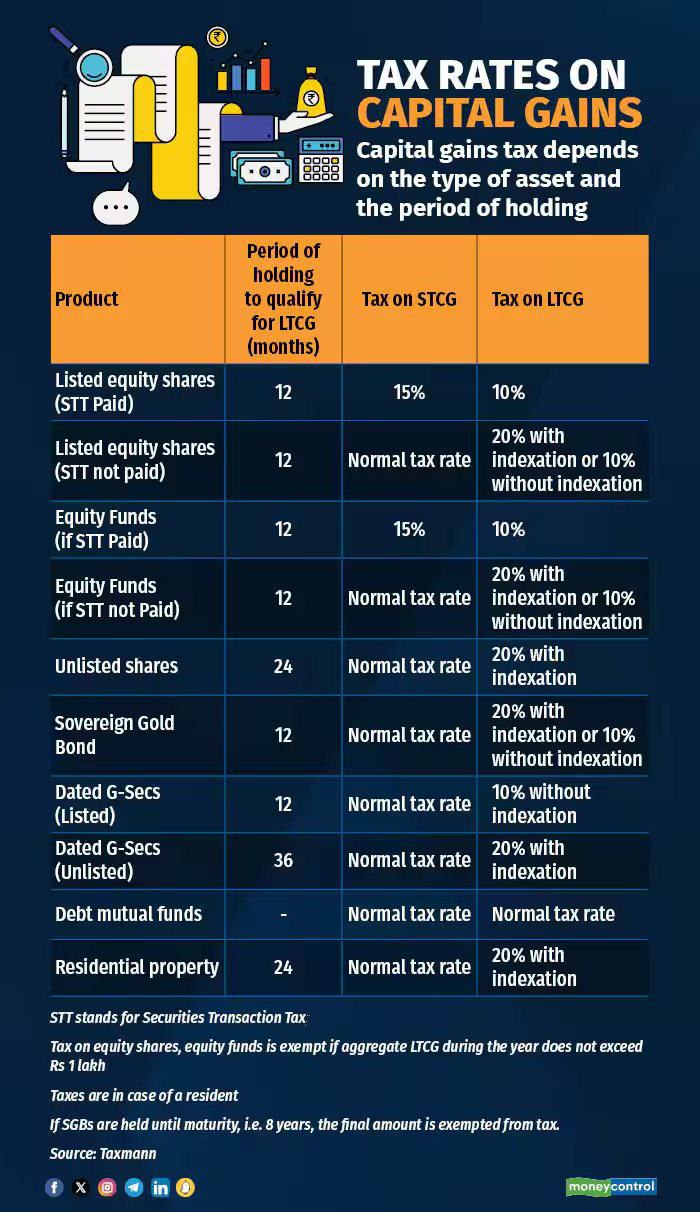

| Tax Rate | Normal slab rates | 15% (STCG), 10% on gains > ₹1 lakh (LTCG) | |

| ITR Form | ITR-3 | Typically ITR-2 | |

| CBDT Circular (Listed Shares) | Option to choose, consistent in subsequent years | Option to choose, consistent in subsequent years | |

| Unlisted Shares | Not applicable | Always treated as capital gains |

Equity / Capital Gains Tax in India & Across the world

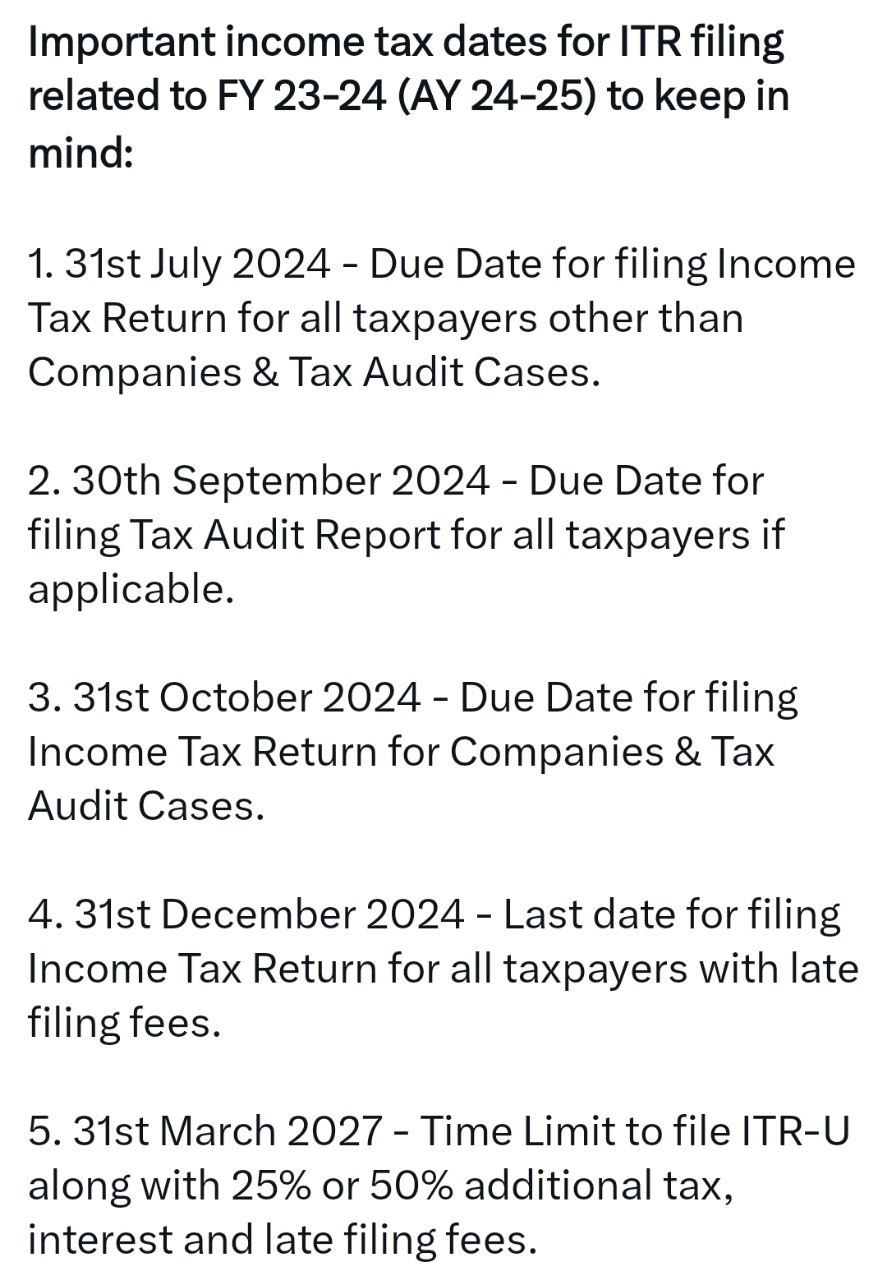

Important due dates for income tax for FY 2023-24

Popular blog:

Income tax rate in case of capital Gain regulation in India

Ready Recknor for calculating capital gains tax for all class of Assets.

- All about the Income taxation on capital gain

- Provision-of-capital-gains-charts

- All about the Income taxation on capital gain

- Provision-of-capital-gains-charts

- All about the Income taxation on capital gain

- All about the Income taxation on capital gain

- Delay in the deposit of Employer provident fund during the lockdown

- Aware of the penalty of Section-234f for late filing of ITR

Help Need? – Contract us

Rajput Jain and associates Professional are available to help you file your ITR return without any kind of hassle. We ensuring your foreign assets are accurately reported & you comply with Indian tax regulations. For query or help, contact: singh@carajput.com or call at 9555555480