File Fresh declaration required for GTA Services

Page Contents

File Fresh declaration required for Goods Transport Agency Services

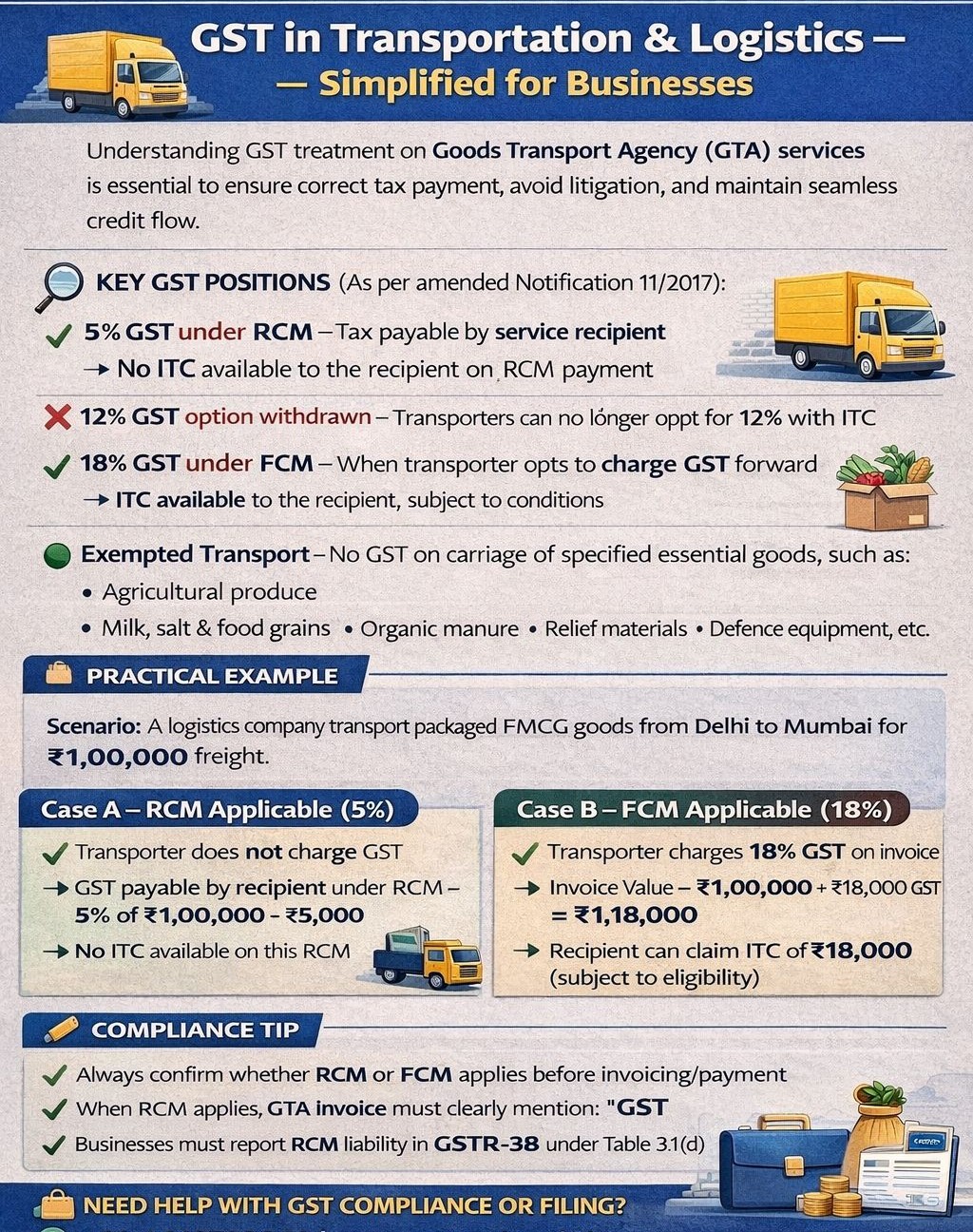

Managing billing under both Forward Charge Mechanism and Reverse Charge Mechanism for a transporter client involves meticulous compliance with GST regulations. Services to unregistered persons or those transporting exempt goods fall under FCM. Services to specified entities (as per RCM rules) fall under RCM.

Unregistered Transporter or Local Truck Carriage Charge

Non-GTA Service: If the transporter is not registered under GST and does not issue a consignment note, the service is not considered as a GTA service. Such transportation services are exempt from GST, and no RCM applies.

GTA Service (with a Consignment Note): If an unregistered transporter issues a consignment note, the service qualifies as a Goods Transport Agency (GTA) service.

- RCM Applicability: The recipient of the service (payer of freight) is liable to pay GST under RCM.

- Input Tax Credit (ITC): The recipient can claim ITC on the GST paid under RCM only if the goods or services are used for business purposes.

Consignment Note Requirement: A consignment note is the primary document that differentiates between a regular transportation service and a GTA service. In the absence of a consignment note, the service is not subject to RCM and is exempt from GST.

Transporter with Transport ID (Registered as GTA)

- GTA Service: If the transporter is registered under GST and provides a consignment note, the service is treated as a GTA service.

- GST Applicability:

- Option 1: Charge GST at 5% without availing ITC (RCM applies): The recipient pays GST under RCM and can claim ITC, subject to business use.

- Option 2: Charge GST at 12% with ITC (FCM applies): The transporter discharges GST under FCM, and the recipient can claim ITC on GST paid, subject to business use.

RCM applies only when: The transporter qualifies as a GTA (issues a consignment note). The recipient is a specified person (e.g., registered entities, factories, societies, partnerships, casual taxable persons, etc.). Unregistered recipients do not fall under RCM for GTA services.

ITC on RCM: The recipient can claim ITC on GST paid under RCM, provided:

- The goods or services are used for business purposes.

- The recipient has valid documentation (e.g., invoice, consignment note, and payment proof).

Special Considerations for Transporters with Transport ID: Such transporters must choose between:

- Charging GST at 5% (RCM applies).

- Charging GST at 12% (FCM applies).

They should declare their choice using Annexure V if opting for FCM.

Use Annexure V for Forward Charge Mechanism

If opting to pay tax under FCM for the financial year, submit Annexure V by the prescribed deadline (28th November 2024 for FY 2024-25).

If GST taxpayer are supplying Goods Transport Agency (GTA) services and wish to opt for paying GST under the forward charge mechanism for the current financial year and onwards, you must file Annexure V on the GST portal by 28th November 2024.

This option is available for the current financial year and will apply for subsequent periods unless a fresh declaration is made to opt out. Filing Annexure V ensures clarity in your tax obligations and prevents disputes regarding the applicable GST mechanism for your services. Forward Charge vs. Reverse Charge: Under the forward charge mechanism, GTA will be responsible for paying GST on the services you provide.

If you choose not to file Annexure V, the reverse charge mechanism will apply, and the recipient of your services will bear the GST liability. Missing the deadline may result in defaulting to the reverse charge mechanism, altering your tax liabilities and compliance responsibilities.

Steps to File Annexure V for Forward Charge Mechanism on GTA services

Here’s a step-by-step guide related File Annexure V on GTA services for Current FY & onwards

- Log in to the GST Portal: Use your credentials to log in to www.gst.gov.in.

- Access Annexure V Form:

- Option 1: When prompted, select Yes if you are a GTA opting for forward charge payment. You will be redirected to the Annexure V form.

- Option 2: Alternatively, navigate manually:

Dashboard > Services > User Services > GTA > Opting Forward Charge Payment by GTA (Annexure V).

- Fill Out the Form: Enter the required details, including confirmation of your intent to pay tax under the forward charge mechanism.

- Submit Before the Deadline: Ensure you complete and submit the form on or before 28th November 2024.

- Acknowledgment: After successful submission, download or save the acknowledgment for your records.

Implications for Recipients: Ensure proper classification of the transport service (GTA or non-GTA). Avail ITC on GST paid under RCM or FCM, aligning with business use and compliance requirements.