Credit Note for Trade/Cash discount tied to Original invoice

Page Contents

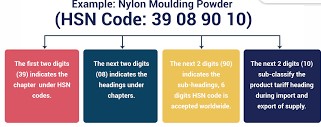

Harmonized system of nomenclature (HSN) in Goods and Services Tax

HSN CODE IS REQUIRED ON ALL B2B INVOICES FOR EVERY TAXPAYER.

HSN codes to be declared under the GST in present circumstances

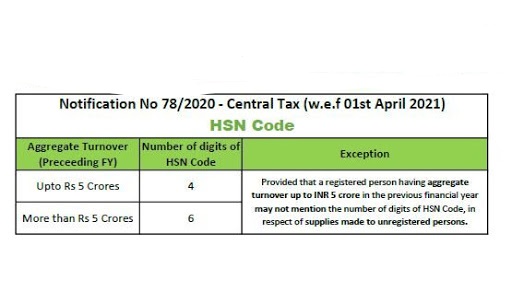

Note: A registered person with a cumulative turnover of up to 5 crores rupees in the past financial year is not required to include the number of digits of the HSN Code in a tax invoice issued in respect of supplies made to unregistered persons.

| Turnover/ Sales | Number of digits of HSN to be declared in Return or invoices |

| Up to 1.5 crore | 4 |

| 1.5 crore- 5 crore | 4 |

| More than 5 crore | 6 |

- Registered persons with a turnover of more than Rs 5 crores will be given an HSN code with up to 6 digits (it was previously 4 digits).

- HSN Code was required for every B2B transaction by every taxpayer, but it was exempt for taxpayers with a turnover of up to Rs 1.5 crore.

- Only B2C sales by taxpayers with a turnover of up to Rs 5 crore are exempt.

Why is HSN essential for the GST?

- The motive of HSN codes is to ensure that GST is systematically and globally established. HSN codes will eliminate the need to upload detailed information about the goods. It will save time and make filing simpler as GST returns are automated.

- The dealer or service provider should provide HSN/SAC with a wise conclusion of sales in its GSTR-1 if its turnover falls within the above slabs.

What are the Rules & nature for Classifying goods under the HSN code?

- In formatting a classification for a specific item, GST Dealers shall apply the General Interpretative Rules (GIR) in a systematic sequential approach. when a classification is done, there is no need to continue applying the remainder of the rules.

- Further Shifting towards the next rule is only essential if the full categorization does not occur from the application of the previous rule. Classification is finally carried out when there is no uncertainty or confusion.

- For the purposes of classification, every other word should take its meaning or be interpreted in its general sense, and not in a technical or strict sense.

Basis of Rule 1 : Titles of sections, chapters, and sub-chapters are provided for ease of reference only. For legal purposes, refer to headings and sub-headings to drive classification.

Basis of Rule 2a : If the goods are incomplete/unfinished and have the characteristics of the finished product, classification is the same as that of the finished product. The heading shall also include removed/unassembled or disassembled parts.

Basis of Rule 2b : Any reference to a material or substance includes a reference to mixtures or combinations of that material or substance with other materials or substances. The classification of goods consisting of more than one material or substance shall take place as per Rule 3.

Basis of Rule 3a : Choosing a specific heading is preferred over a general heading.

Basis of Rule 3b : Mixtures/composite goods should be classified per the material or substance that gives them their essential character.

Basis of Rule 3c : If two headings are equally suited to the item, choose the heading that appears last in numerical order.

Basis of Rule 4 : If goods cannot be classified per the above rules, they are to be classified according to the goods to which they are most akin.

Basis of Rule 5 : Containers specifically designed for the article and suitable for long-term use will be classified along with that article, if such articles are normally sold along with such cases. For example, a camera case would fall under cameras. Packing materials and containers are also to be classified with the related goods except when the packing is for repetitive use.

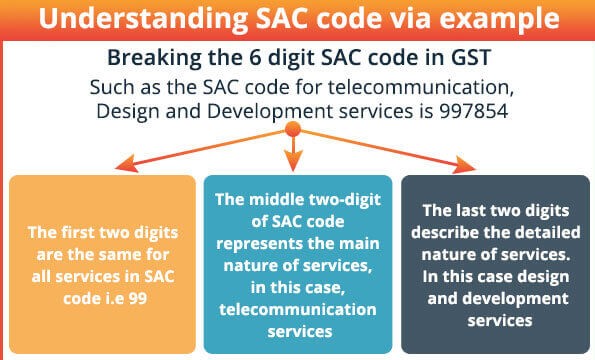

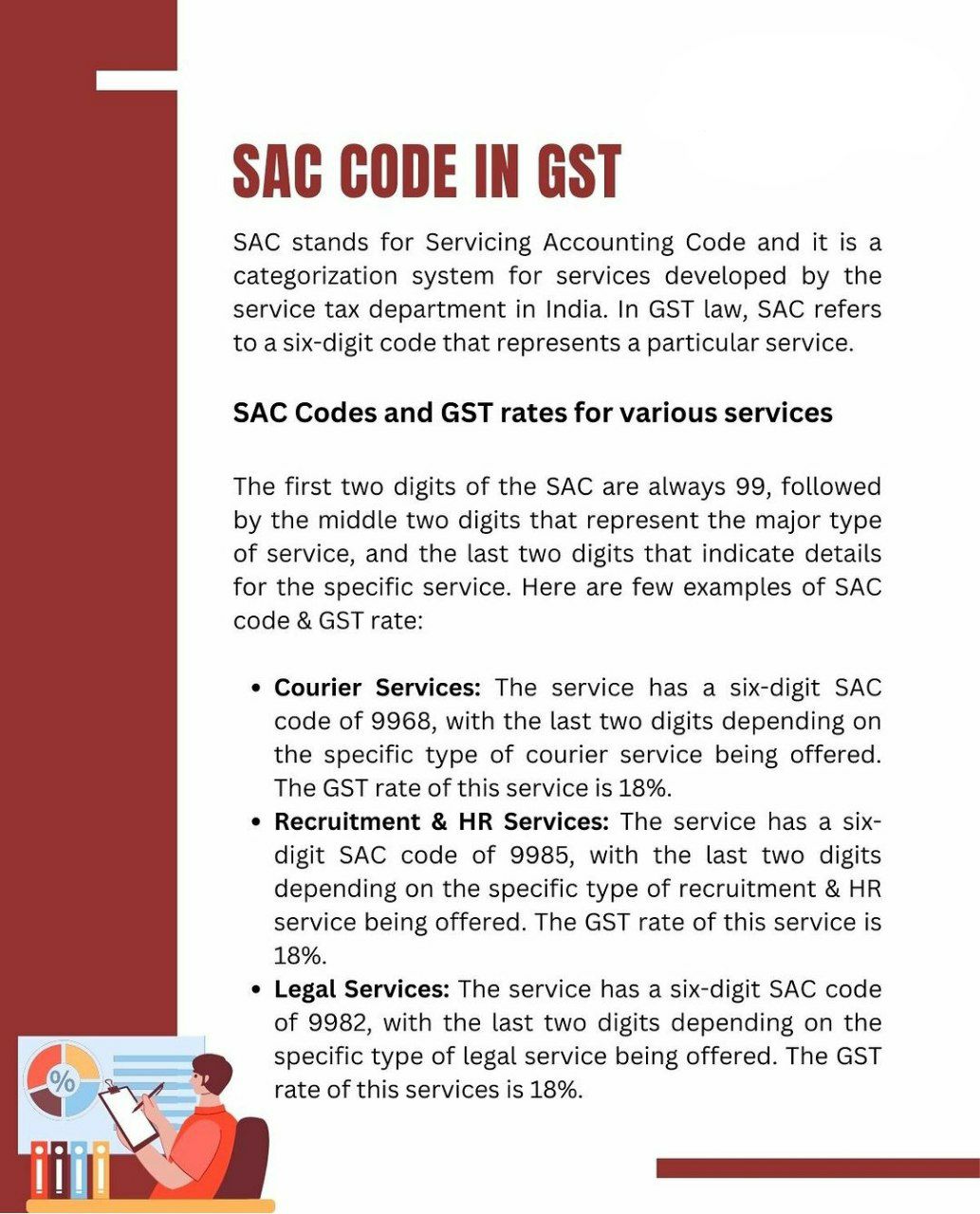

SAC codes(Services Accounting Code):

- Services will be classified as per the Services Accounting Code (SAC). In the case of services, each type of service provided is given a unified code for recognition, measurement, & taxation.

- These are commonly known as Services Accounting Code. It is formulated by the CBEC.

- These codes are a combination of numbers to identify the service type and the rate at which it is to be taxed. SAC Code has been in existence to define proper levy of service tax & each kind/type of service under the GST law.

SAC codes Services Accounting Code for services along with the rate of IGST, CGST, SGAT are mention in the below Link

Provisions on Discounts (Section 15 of CGST Act, 2017):

- Discount Before or At the Time of Supply: Discounts mentioned on the face of the invoice are excluded from the taxable value. The discount must be recorded on the invoice. GST liability is calculated on the reduced value (i.e., taxable value = value after discount).

- Discount After the Time of Supply: Discounts given after supply can also be excluded from the taxable value, provided all the following conditions are met:

-

-

- There is a prior agreement between the supplier and recipient (established before supply) about the discount.

- The discount is specifically linked to a relevant invoice.

- Recipient of the goods/services reverses the Input Tax Credit proportionate to the discount.

-

Categories of Discounts in GST:

- Before or At the Time of Supply:

- Must appear on the invoice.

- Directly reduces the taxable value.

- No Input Tax Credit reversal required.

- After the Time of Supply:

- Requires compliance with all conditions u/s 15(3)(b) of of CGST Act, 2017

- Input Tax Credit attributable to the discount must be reversed by the recipient.

- Typically involves trade schemes, performance discounts, or volume-based rebates.

GST on Trade vs. Cash Discounts:

GST does not distinguish between trade and cash discounts. Both are treated based on their timing relative to the supply:

- Trade Discounts: Generally agreed upon in advance and often linked to bulk purchases or long-term agreements. Can reduce taxable value if recorded as per Section 15(3) of of CGST Act, 2017

- Cash Discounts: Typically for early payment or cash transactions. Treated the same way as trade discounts under GST if the conditions are met.Credit Notes for trade discounts or cash discounts are tied to original invoice

In GST, credit notes for trade discounts or cash discounts are tied to the original invoice, and the SAC (Service Accounting Code) or HSN (Harmonized System of Nomenclature) code used on the credit note must correspond to the one from the original invoice. Here are the key points:

- Reference to the Original Invoice: Credit notes are issued to account for adjustments like discounts, returns, or other changes in the value of goods or services. The credit note must explicitly reference the original invoice number and date to establish the connection.

- SAC/HSN Code Consistency: The SAC/HSN code used on the credit note is the same as that in the original invoice. This ensures uniformity and accurate reporting for GST compliance.

- GST Implications: The credit note also reflects the corresponding GST rates applicable to the goods or services. Adjustments made via the credit note (e.g., reducing taxable value) are reflected in the GST returns to ensure the correct liability or refund.

- Purpose: This mechanism ensures transparency and consistency in tax reporting and prevents mismatches in the GST system.

If you’re issuing a credit note for discounts, ensure it directly corresponds to the original invoice for compliance and smooth reconciliation in GST filings.