Limits for Condonation of Delayed of Refund Claim, C/F Loss

Page Contents

New Monetary Limits for Condonation of Delayed Filing of Refund Claims & C/F Losses

- Central Board of Direct Taxes has issued new monetary limits in respect of condonation of delay in filing refund claim and claim of carry forward of losses u/s 119(2)(b) of the Income-tax Act, 1961. Now Lower Income tax authorities empowered to deal higher refunds w.e.f. 01s June 2023: Circular 7/2023.

- Where the time period of filing of return as per section 139 has expired and assesse couldn’t claim Income Tax refund or loss, due to genuine hardship, section 119(2)(b) empowers claim of refund/ loss as per procedure laid down in Circular 9/2015 dated 09-06-2015.

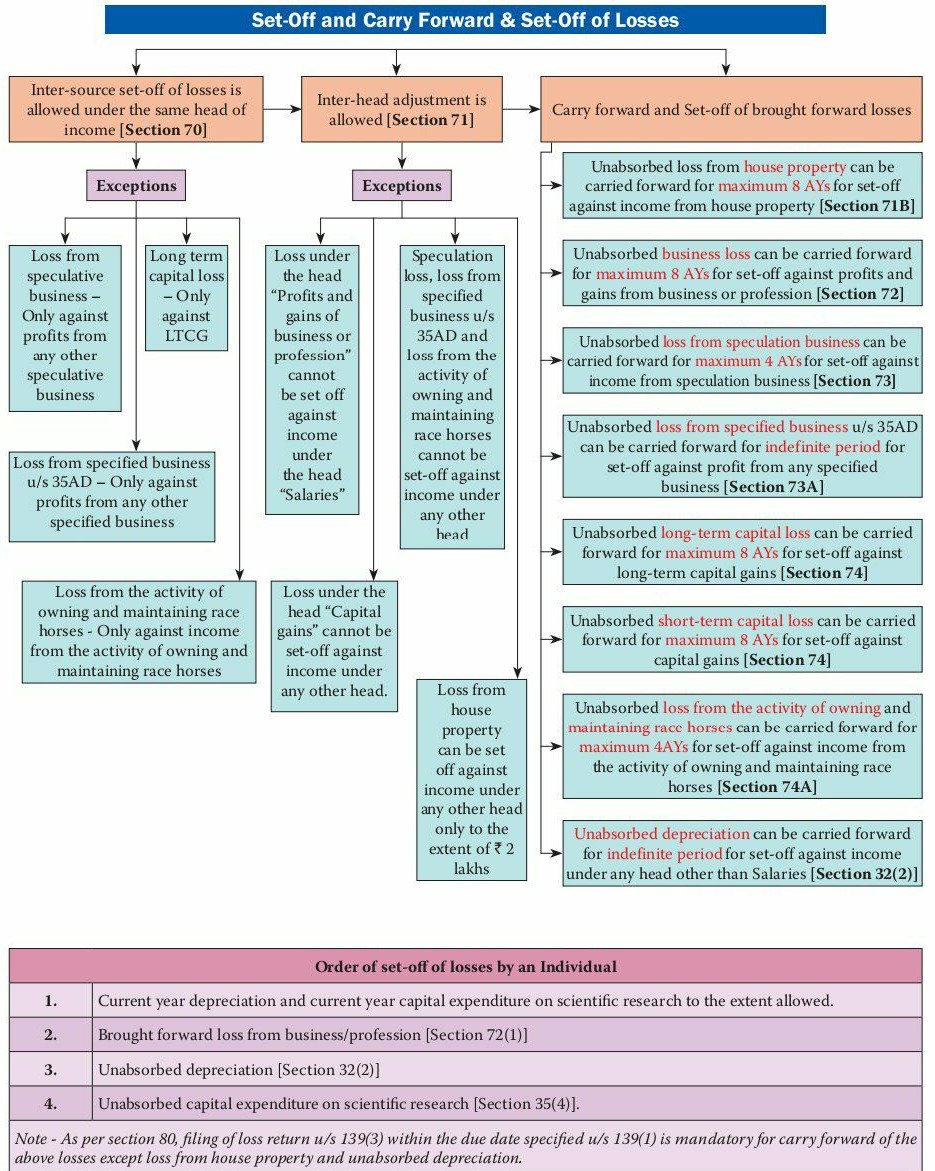

Set-Off and Carry Forward & Set-Off of Losses

Condonation of Delayed income tax refund.

- The Condonation application for claim of refund or supplementary claim of refund or loss has to be made with in six ears (excluding period for which proceedings were pending before Court) from end of relevant Ay & such applications for condonation are required to be processed within Six months from end of month in which application is made.

- Income Tax Refund claims u/s 119(2)(b) can be made only for excess amount of Tax deducted at source / Tax collection at source/advance tax/self-assessment tax. No Interest is allowed on income Tax refund claim or supplementary refund claim.

- Tax authority has to ensure that the refund/loss claim is correct and genuine and there was genuine hardship. The Income Tax authority empowered to deal with delayed refund/loss claim can direct jurisdictional Assesse Officer to conduct enquiry or scrutinize to ascertain correctness of claim.

Increase in Powers to deal refund/loss w.e.f. 01-06-2023.

- Power of Principal Commissioners of Income-tax/Commissioners of Income-tax to deal with claims increased from INR 10,00,000/- to 50,00,000/- per Ay.

- Commissioners of Income-tax power to deal with Income Tax refund/loss claims increased from INR 50,00,000/- to 2,00,00,000/-. Commissioners of Income-tax can’t deal with claims below INR 50,00,000/-.

- Principal Commissioners of Income-tax power to deal with Income Tax refund/loss claims increased from INR 50,00,000/- to 3,00,00,000/-.. Principal Commissioners of Income-tax can’t deal with claims below INR 2,00,00,000/-.

- Central Board of Direct Taxes now shall deal with claims above INR 3,00,00,000/-..only (as against earlier limit of refund/loss claims above INR 50,00,000/-)

Central Board of Direct Taxes also has powers to examine grievances

The Central Board of Direct Taxes also has powers to examine grievances under this Circular for passing or not passing orders by Income Tax authorities.

- Principal Commissioners of Income-tax/Commissioners of Income-tax shall be vested with the powers of acceptance/rejection of claims or applications if the amount of the claims is not exceeds INR 50,00,000/- for any one Ay.

- Chief Commissioners of Income-tax shall be vested with the powers of acceptance/rejection of applications/claims if the amount of claims exceeds INR 50,00,000 However is not more than INR 2 Cr for any 1 Ay.

- Principal Chief Commissioners of Income-tax shall be vested with the powers of acceptance/rejection of such applications/claims if the amount of claims exceeds INR 2 Cr but is not more than INR 3 Cr for any one Ay.

- Claims or applications for amounts more than INR 3 Cr shall be considered by the Central Board of Direct Taxes.

The revised monetary limits for applications/claims in respect of the competent authorities shall be applicable to the applications/ claims filed on and after June 1, 2023. Central Board of Direct Taxes also given guidelines specified in Income tax Circular No. 09 dated 09-06- 2015 shall remain unchanged. Circular No. 07/2023 Date: 31/05/2023