Changes Relating to Cash Payments/Receipts

Page Contents

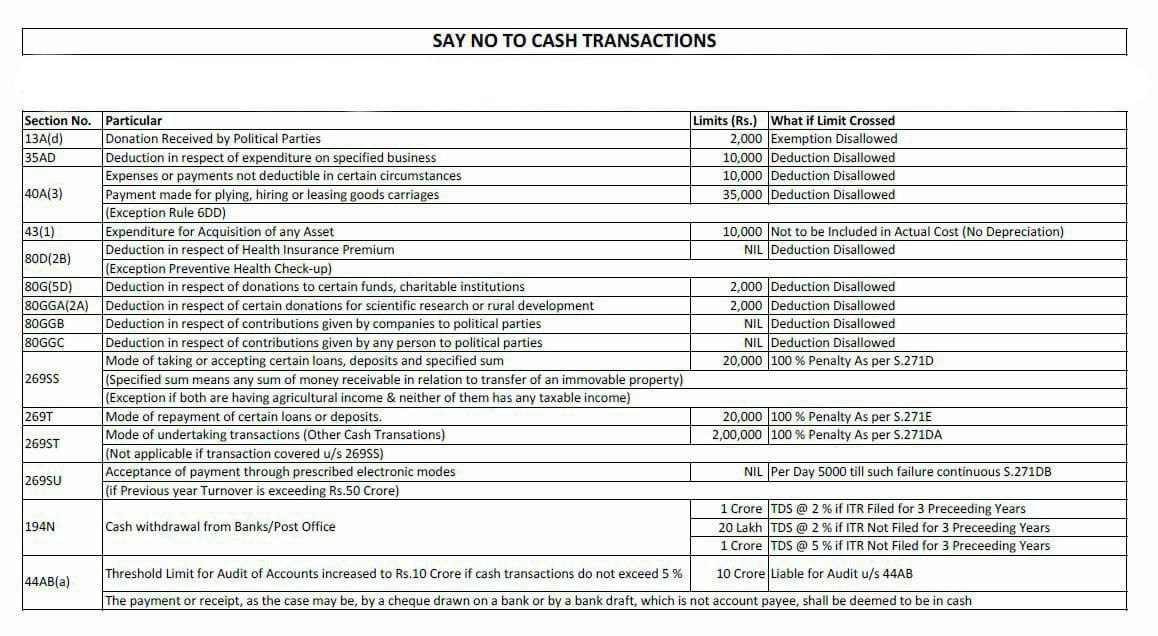

Income Tax Rules – Cash Transaction Limits

Cash Expense Limit – Sec 40A(3)

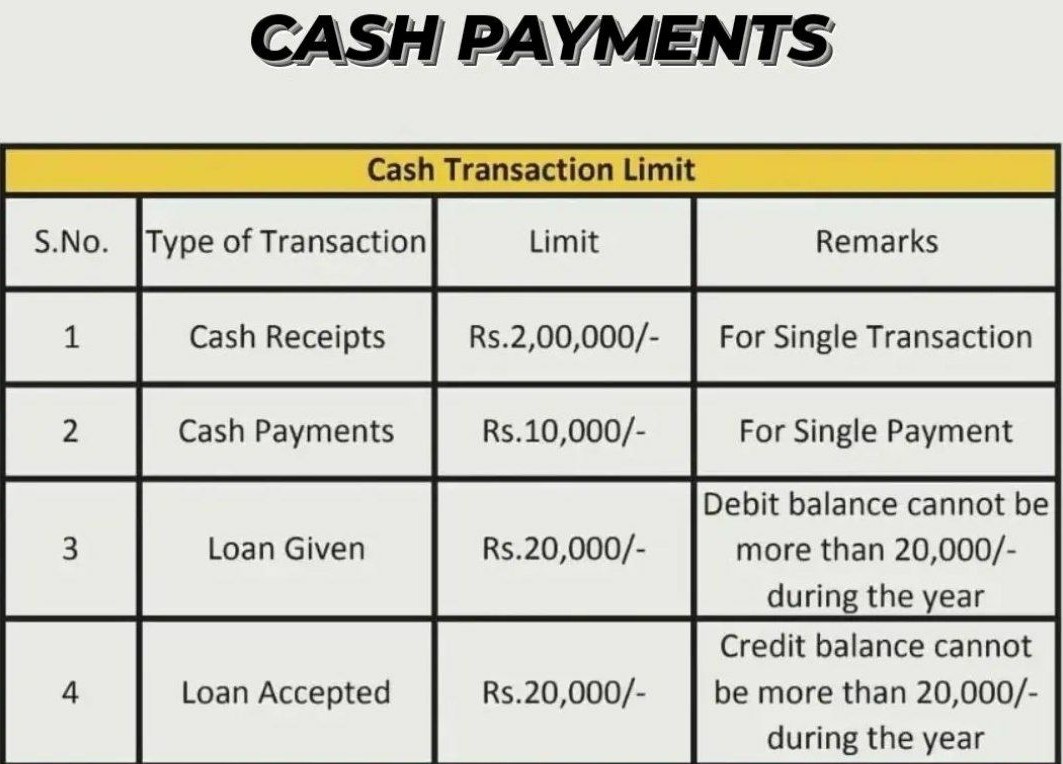

- Cash Expense Limit: Cash payment above INR 10,000/day per person is NOT allowed as expense

- For transporters → limit is INR 35,000/day

- Cash Expense Limit Impact: Expense will be disallowed → higher taxable income

- For example: You pay INR 25,000 cash to a vendor → entire INR 25,000 may be disallowed

Cash Loan / Deposit Acceptance – Sec 269SS

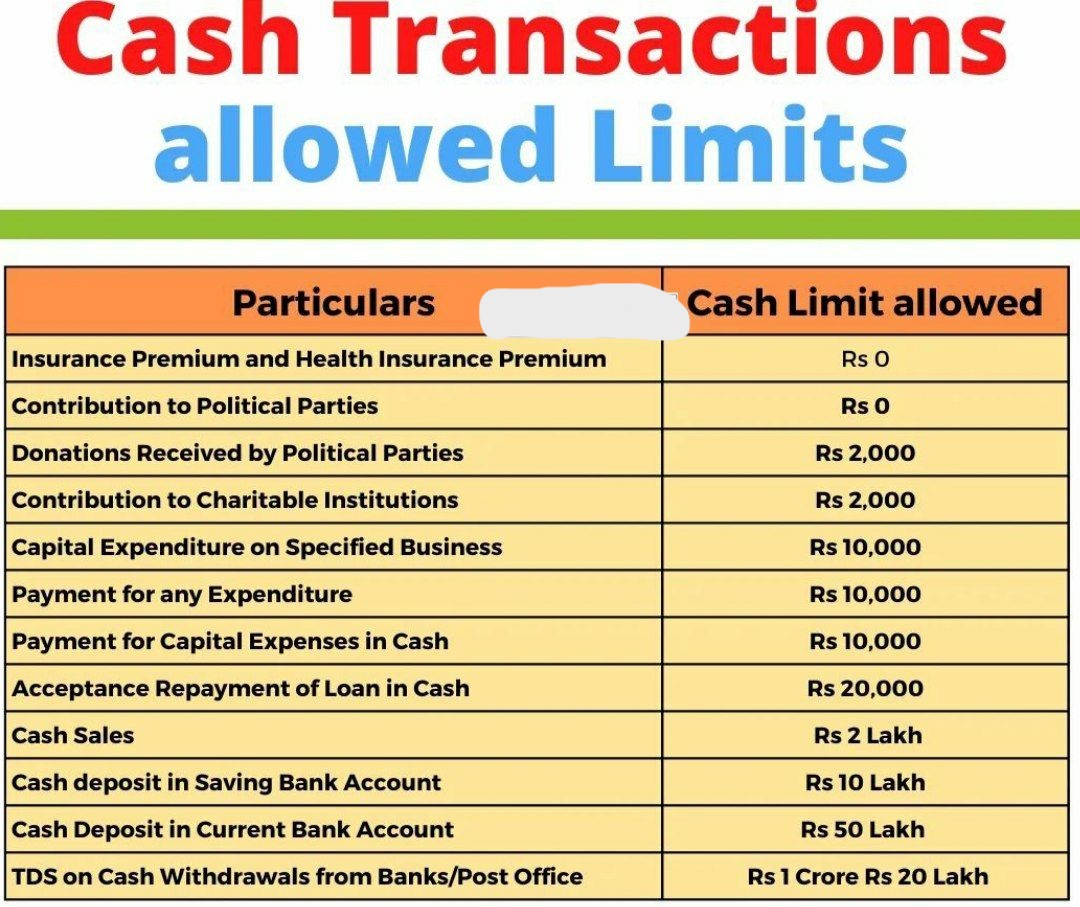

- Cash Loan / Deposit Acceptance cannot accept INR 20,000 or more in cash. Applies to Loans, deposits, and Property advances

- Cash Loan / Deposit Acceptance Includes both single transactions and aggregate

- Noncompliance of Cash Loan / Deposit Acceptance then Penalty (Sec 271D) = 100% of amount accepted

Cash Loan Repayment – Sec 269T

- Cash Loan Repayment cannot repay INR 20,000 or more

- Cash Loan Repayment in cash Includes: Principal + Interest

- Penalty (Sec 271E) = 100% of amount repaid

Cash Receipt Limit – Sec 269ST :

- Cash Receipt Limit cannot receive INR 2,00,000 or more in cash. Restrictions like In a single transaction, OR per day, OR per event/occasion.

- Penalty (Sec 271DA) = 100% of amount received

- Example: Receiving INR 2.5 lakh cash for sale → full INR 2.5 lakh penalty risk

High-Value Cash Deposits (SFT Reporting)

Banks report to the Income Tax Department:

-

- Savings A/c cash deposit ≥ INR 10 lakh/year

- Current A/c cash deposit ≥ INR 50 lakh/year

- This is reporting only, but Triggers scrutiny / notices, Must match with ITR & AIS and

Property Transactions

- Cash payment ≥ INR 20,000 for property violates Sec 269SS

- Cash receipt ≥ INR 2,00,000 violates Sec 269ST

CHANGES RELATING TO CASH PAYMENTS/RECEIPTS

Cash Payments/Receipts & reporting related to MCA & in ITR with Effect from 01.04.2017

Section 269ST which has been newly inserted provides that no person shall receive an amount of two lakh rupees or more–

- In aggregate from a person in a day

- A respect of a single transaction

- In respect of transaction relating to one event or occasion from a person

Otherwise, than by an account payee cheque or account payee bank draft or use of electronic clearing system through a bank account.

The section is not applicable to the following:

- Government

- Any banking company

- Post office savings banks

- Co-operative banks

- Any other person as notified by the Central Government

Transactions of the nature referred to in Section 271 DA in the Act shall provide for levy of penalty on a person who receives a sum in contravention of the provisions of the proposed section 269ST. The sum equal to the amount of receipt shall be levied as penalty by the Joint Commissioner.

Section 269ST & Section 271D and other cash restrictions:

Section 269ST & Section 271D and other cash restrictions:

Relating to Cash Receipts

1) The provision restricts the receipt of cash above Rs. 2 lacs:

Any person who receives above Rs. 2 lacs in cash will be liable to penalty equivalent to the amount received; however, there is no restriction on payment of cash under this section.

2) Receiving cash in a day from a person above Rs. 2 lacs is not allowed:

The cash receipt of more than Rs. 2 lacs from a single person in a day is not allowed even though the amount has been paid in multiple transactions during the day.

3) A receipt exceeding Rs. 2 lacs for a single transaction or single event is not allowed.

Relating to Cash Payments

1) Cash Payments above Rs. 10000/-:

The earlier provision U/S 40A(3) restricting cash payments above Rs. 20000 for business purposes has also been amended. The limit for payment of expenses by Cash for both capital and revenue expenditures has been reduced from Rs. 20000 to Rs. 10000 per day in aggregate per person.

2) Now cash payments above Rs. 10,000/- shall not be allowed as expenses in the income tax return.

For capital expenditures, the depreciation shall not be allowed on capital assets in case of payment made in cash.

3) Cash donations exceeding Rs.2, 000 will not be eligible for education under Section 80G.

Consequently:

- The limit for receipt of amount in cash has been prescribed as 2, 00,000.

- In case of violation of such a provision, an equivalent penalty shall be leviable under U/s 271DA of Income Tax Act.

- If a person accepts amount of Rs.2, 00,000 or more

By Cash either in one transaction or

From one person in aggregate in a day or

In relation to one event or occasion from a person

He/she shall be liable for an equivalent amount of penalty under Section 271DA.

- Since cash receipts exceeding Rs. 2 lacs have been made liable for equivalent penalty the TCS provisions requiring collection of tax @ 1% on cash sales exceeding Rs. 5 lacs in case of bullion/jewelry and Rs. 2 lacs in case of other goods/services have been withdrawn.

CASH REPORTING REQUIRED IN INCOME TAX RETURN FORM ITR-1 & ITR-4S INTRODUCED FOR AY 2017-18

CBDT notified the ITR forms for assessment year 2017-18 on 1st April 2017. ITR form 1 which is for person having taxable income less than 50lacs and ITR 4S for deemed income under Section 44AD are introduced, requiring declaration of cash deposited during the demonetization period i.e. 09.11.16 to 31.12.16.

Column Part-E of the ITR-1 form is added, requiring information on cash deposits during such period if the “aggregate cash deposits” during this period were Rs 2 lakhs or more.

CASH REPORTING AS PER MCA

The Ministry of Corporate Affairs has made an amendment in the Companies Act, 2013 to add provisions for companies to disclose details of SBN in the balance sheet held and transacted during the demonetization period from 08-11-2016 to 30-12-2016.

1) The following clause shall be inserted in Schedule III, in Division I, in Part I under the heading “General instructions for preparation of Balance Sheet” in paragraph 6:

“Every company shall disclose the details of Specified Bank Notes (SBN) held and transacted during the period from 8th November, 2016 to 30th December, 2016 as provided in the Table below:

| SBNs | Other Denomination Notes | Total | |

| Closing cash in hand as on 08.11.2016 | |||

| (+) Permitted receipts | |||

| (-) Permitted payments | |||

| (-) Amount deposited in Banks | |||

| Closing cash in hand as on 30.12.2016 |

For the purposes of this clause, the term ‘Specified Bank Notes’ shall have the same meaning provided in the notification of the Government of India, in the Ministry of Finance, Department of Economic Affairs number S.O. 3407(E), dated the 8th November, 2016.”.

2) The following clause shall be inserted in the principal Act, in Schedule III, in Division II, in Part I under the heading “General instructions for preparation of Balance Sheet” in paragraph 6:

“Every company shall disclose the details of Specified Bank Notes (SBN) held and transacted during the period 08/11/2016 to 30/12/2016 as provided in the Table below:

| SBNs | Other Denomination Notes | Total | |

| Closing cash in hand as on 08.11.2016 | |||

| (+) Permitted receipts | |||

| (-) Permitted payments | |||

| (-) Amount deposited in Banks | |||

| Closing cash in hand as on 30.12.2016 |

For the purposes of this clause, the term ‘Specified Bank Notes’ shall have the same meaning provided in the notification of the Government of India, in the Ministry of Finance, Department of Economic Affairs number S.O. 3407(E), dated the 8th November, 2016.”.

3) MCA has also made amendments in the Companies (Audit and Auditors) Rules, 2014 to add provisions for auditors to report on company disclosure of SBN during demonetization period from 08-11-2016 to 30-12-2016.

In rule 11, the following clause shall be inserted:

“Whether the company had provided requisite disclosures in its financial statements as to holdings as well as dealings in Specified Bank Notes during the period from 8th November, 2016 to 30th December, 2016 and if so, whether these are in accordance with the books of accounts maintained by the company.”

We should always use banking channels (RTGS/NEFT/cheque). We should Stay Compliant via Use digital payments / banking routes, maintain proper invoices & supporting documents, Avoid splitting transactions artificially, Reconcile with AIS / Form 26AS and Consult your CA regularly

Cash transactions are heavily restricted. Violations = 100% penalty + tax scrutiny risk. Then most penalties arise from Property deals, Loan entries in books AND Cash sales beyond INR 2 lakh. Even genuine transactions can attract penalty if mode is cash

Read more about: What is core Business Activity GST

Read more about: Important decisions made at the 43rd GST Council meeting

FOR FURTHER QUERIES CONTACT US: W: www.carajput.com E: singh@carajput.com T: 9-555-555-480