Expenses Allowable Against Partners Salary

Page Contents

ALLOWABILITY OF SALARY TO PARTNER, IN CASE OF FIRM – BUSINESS EXPENDITURE

No reassessment after 4 years alleging wrong allowance of exp. if assessee had disclosed all material facts

Section 37(1), read with section 147, of the Income-tax Act, 1961 – Business expenditure – Allowability of salary to partner, in case of Firm

Where assessment in case of assessee was completed under section 143(3) wherein assessee’s claim for salary paid to partners was allowed, then in absence of assessee’s failure to disclose all material facts necessary for assessment.

Assessing Officer could not initiate reassessment proceedings on basis of change of opinion that claim for payment of salary was wrongly allowed [2015]-HIGH COURT OF GUJARAT – SKY Diamonds v. Assistant Commissioner of Income-tax

FACTS

The assessment in case of assessee was completed under section 143(3) wherein the assessee’s claim for payment of salary to partners was allowed.

After expiry of four years from end of relevant assessment year, the Assessing Officer initiated reassessment proceedings taking a view that assessee’s claim for payment of salary was wrongly allowed.

The assessee filed instant writ petition contending that since there was no failure on its part to disclose fully and truly all material facts necessary for assessment, impugned reassessment proceedings deserved to be quashed.

The High Court held in favour of assessee that

Section 147 enables the Assessing Officer to reopen the assessment subject to the provisions of sections 148 to 153.

but the first proviso to the very section 147 provides that no action shall be taken under this section 147 after the expiry of the period of four years from the end of the relevant assessment year.

unless any income chargeable to tax has escaped assessment for such assessment year by the reason of failure on the part of the assessee to disclose full and truly all material facts necessary for assessment for the respective assessment year.

The aforesaid shows that unless the case falls in the exceptional category of ‘failure to disclose fully and truly all material facts necessary for the assessment’ the action after the expiry of four years for reopening of the assessment is not permissible.

The assessee’s case was that full and true disclosure of all material facts relevant to the reasons which is the ground for reassessment were disclosed before the Assessing Officer at the time when the scrutiny of the assessment had taken place.

It was submitted that not only that but the audit report was also produced which included the remuneration to the partners and during the course of the assessment, this aspect is deemed to have been considered and the assessment order was passed.

Whereas the revenue is not in a position to dispute the factual aspect that the true disclosure was made by the assessee for the remuneration paid to the partners and computed while computing the business income.

The revenue is also unable to dispute that the audit report showing the aforesaid details were produced.

In view of the above, there was no reason to believe that true and full disclosure was not made by the assessee to come out from the bar of four years as provided by first proviso to section 147.

Once the bar operates upon the power by express statutory provision, the action can be said as without jurisdiction.

If the action of issuance of notice is without jurisdiction, it would be a case for interference under article 226 of the Constitution.

In view of the above, the impugned action under section 147 and consequently issuance of notice under section 148 may not stand in the eye of law. Hence, they are quashed and set aside.

The petition is accordingly allowed.

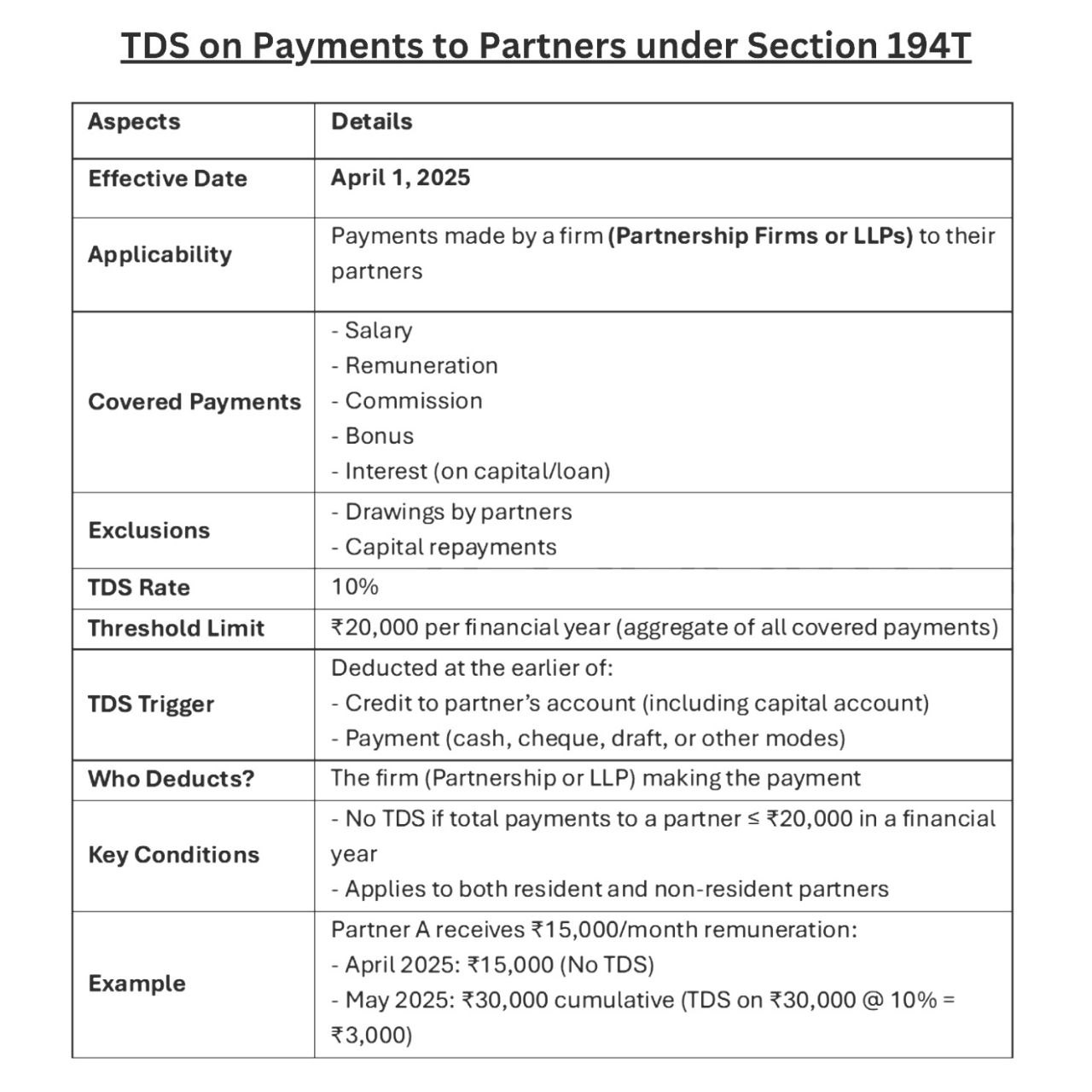

TDS on Payments to Partners under Section 194T

Scope and Applicability: TDS on Payments to Partners

| Particulars | Details |

|---|---|

| Applicability | All Partnership Firms and LLPs |

| Payee | Individual Partners |

| Nature of Payments Covered | Salary, Bonus, Commission, Interest, Remuneration, even if credited to capital account |

| TDS Threshold | ₹20,000 aggregate per financial year (per partner) |

| TDS Rate | 10% |

| PAN Not Available | 20% (as per Section 206AA) |

| TDS Deduction Point | Earlier of: credit or payment |

| Applicable Even If | Partner’s share is credited to Capital A/c |

| Excluded | If total payment/credit to partner does not exceed ₹20,000 during the year |

Relation to Partner Remuneration Limits under Section 40(b)

Section 40(b) still governs the maximum allowable deduction of partner remuneration.

Section 194T now ensures tax deduction at source on such payments, regardless of whether they are fully deductible under 40(b) or not.

| Book Profit (or Loss) | Maximum Deductible Remuneration |

|---|---|

| First INR 3 lakh | INR 1.5 lakh or 90% of book profit (whichever higher) |

| Balance Book Profit | 60% of book profit |

Compliance Checklist for Firms

-

Obtain TAN (if not already held).

-

TDS Deduction at 10% on all covered payments > ₹20,000 annually.

-

Deposit TDS by the 7th of next month.

-

File Quarterly TDS Returns (Form 26Q).

-

Issue TDS Certificates (Form 16A) to partners.

Benefits

-

Closes tax leakage in firm-to-partner payments.

-

Brings parity in taxation for all forms of remuneration.

-

Improves financial discipline and broadens tax base.

Challenges

-

Increased compliance burden, especially for small firms.

-

Potential cash flow issues for partners.

-

Need for educational outreach by tax authorities to ensure smooth rollout.

Difference from Section 192

| Section 192 | Section 194T |

|---|---|

| TDS on Salaries (employee-employer) | TDS on Partner Remuneration |

| Only applies if relationship is that of employer-employee | Applies to all firm–partner relationships |

| Includes deductions and exemptions | Flat 10% TDS on gross payment |

| Not applicable to partners | Specifically targets partners |

Hope the information will assist you in your professional endeavors. For query or help, contact: singh@carajput.com or call at 9555 555 480