GST on sale of all used cars, including electric vehicles

Page Contents

GST on sale of all used cars, including electric vehicles

The 55th GST Council meeting held on December 21, 2024, in Jaisalmer, Rajasthan, introduced a uniform 18% GST rate on the sale of all used cars, including electric vehicles (EVs). This decision standardizes GST on second-hand cars, as previously, EVs were taxed at 12%, while petrol, diesel, and LPG cars were subject to 18% GST. Key Takeaways on GST rate on the sale of all used cars, including EVs

-

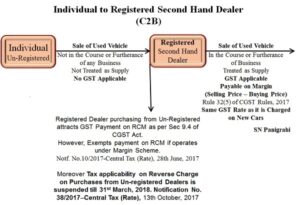

Who Pays GST?

- Only “registered persons” (businesses engaged in buying & selling used cars) are liable to pay GST. Individuals selling used cars to another individual are exempt from GST.

-

When is GST applicable?

- GST is charged only if there is a profit margin on the sale. If a registered person sells a car at a loss (negative margin), no GST applies.

-

Margin Calculation:

- For those claiming depreciation under the Income Tax Act, GST is applied only on the difference between the sale price and the depreciated value.

- For others: GST applies to the difference between purchase price and selling price.

Examples:

📌 Case 1: If a registered person bought a car for INR 20,00,000/-, claimed INR 8,00,000/- depreciation, and later sells it for INR 10,00,000/-, then:

- The car’s depreciated value is INR 12,00,000/-.

- Since the sale price (INR 10,00,000/-) is less than INR 12,00,000/-, the margin is negative (₹-INR 2,00,000/-).

- No GST is charged.

📌 Case 2: If a registered person bought a car for INR 20,00,000/-, claimed INR 8,00,000/- depreciation, and later sells it for INR 15,00,000/-, then:

- The car’s depreciated value is INR 12,00,000/-.

- The profit margin is ₹3 lakh (INR 15,00,000/- – INR 12,00,000/-).

- 18% GST applies on INR 3,00,000/-.

📌 Case 3: If a registered person buys a used car for INR 12,00,000/- and sells it for INR 10,00,000/-, the margin is negative (₹- INR 2,00,000/).

- No GST is charged.

📌 Case 4: If a registered person buys a used car for INR 20,00,000/- and sells it for INR 22,00,000/-, then:

- Profit margin = INR 2,00,000/- (INR 22,00,000/- – INR 20,00,000/-).

- 18% GST applies on INR 2,00,000/-.

GST Valuation on sale of used motor car/old vehicle

Value of valuation of old car i.e. what shall be the value on which GST shall be applicable. As per the GST Notification, the Value of Supply shall be the “Margin of Supply”. The margin of Supply means:-

In case the depreciation Claimed under Section 32 of Income Tax Act 1961:-

- Where depreciation has been claimed on the said goods u/s 32 of the Income Tax Act 1961, the Margin of Supply shall be the difference between the Sale consideration received for supply of such goods and the depreciated value of such goods on the date of supply, and the margin of such supply shall be negative, then it should be ignored.

In all other cases: –

The supply margin is the difference between the selling and purchasing prices, and it is ignored if the margin is negative.

In case old or used car or vehicle is sold by the Government of India: –

In case the old/ used card/vehicle’s Supplier is State government, central govt, /Local authority, Union territory of the recipient is –

- In case unregistered person: Unregistered will have to obtain GST registration and pay GST

- in the case of registered person: Registered person will be liable to pay tax on RCM basis.

Impact of the Decision GST rate on the sale of all used cars, including EVs

- Clarity & Simplification – One uniform 18% rate avoids confusion between petrol/diesel and EV tax rates.

- Lower Tax for EVs – Previously taxed at 12% on the full value, now GST applies only on profit margin.

- Benefit for Individual Sellers – No GST burden for person-to-person sales.

- Boost to Used Car Market – More structured taxation can encourage organized players in the second-hand car industry.

Conclusion on GST Applicable provision on GST on sale of old Car/vehicles.

GST Rate on sale of used motor Car/ vehicles