ITC on Sale of Demo Cars Supply & GST on sale of used Car

Page Contents

Impact of GST: ITC on Vehicles on Sale of ‘ Demo Cars Supply by Dealers

Overview

Demo cars are being used by car dealerships to demonstrate automotive functionality with a view to encouraging sales. Clients test-drive demo models to experience efficiency and understand the benefits of the vehicle. These cars are used for a limited period of time and will then be sold.

The essence of the demo car: a capital good or a dealer’s input?

Pursuant to section 2(19) of the CGST Act, 2017 “capital goods” means goods, the value of which is capitalized on the books of accounts of a person claiming an input tax credit and which are used or intended to be used in the course or in the course of business.

Asset out in section 2(59) of the CGST Act, 2017 “input” means any goods other than capital goods used or expected to be used by a supplier in the duration of or in the course of trade or business.

Consequently, a test car can be either an input or a capital asset. In compliance with the above definitions, the prototype vehicle can be classified as a capital asset because it is used for market marketing and is not intended for retail sales to consumers. If the demo car is capitalized on the books of the accounts, it will be regarded as a capital asset. If not, it may be input.

Read more:Impact of GST on Textile Industry

Demo car on Taxability and GST Tax

- The car dealer had to have registered demo cars in his title and, by nature of registration, the dealer will become the first holder of such cars and, afterward, the car dealer may sell demo cars and, at the time of sale, the vehicle registration will be transferred to the customer.

- The transfer of the demo car to the client by the car dealer shall be liable to GST and shall be subject to taxation at the rates set for the cars.

- The Government has, however, laid down separate provisions for persons engaged in the purchase and sale of second-hand goods. Although demo cars have been used until the vehicles had been sold by the manufacturer, the rules of the old and used vehicle could be drawn.

Read more:Impact of GST on Hotel Industry

The dealer possesses the following two options:

Option-1

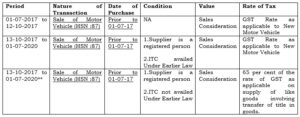

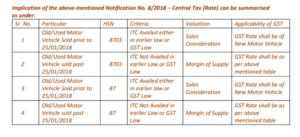

- The dealer may submit the concessional tax rate as specified in Notification No.-8/2018 Central Tax (Rate) dated 25-1-2018 only if no ITC has been claimed by him under the GST or former laws.

- The concessional GST rates are 18 percent for old and used large vehicles (in the case of Petrol LPG / CNG powered motor vehicles with an engine capacity of 1200cc or more and in other motor vehicles with an engine capacity of 1500cc or more) and 12 percent for other old and used vehicles.

- The govt also exempted the compensation cess for all old and used motor vehicles empty Notification No.1/2018 – Compensation Cess (Rate) dated 25-1-2018.

Option-2

- If the dealer seems unable to apply the concessional tax rate as set out in the above-mentioned notification, the dealer shall be permitted to take the ITC at 28 percent on the buy of demo cars and the normal GST rate and, compensation cess ranging from 1% to 22% as the case may be will be applicable.

Input Tax Credit Availability

- At the time of registration and payment, the dealer should have recorded the car as a fixed asset in his accounting records, regardless of whether or not the ITC had been claimed.

- Demo cars are usually purchased on a tax invoice by dealers who are capitalized on their accounting record as capital goods and expressed on the Company’s fixed assets, except the GST component.

- Pursuant to the provisions of the Input Tax Credit given for in Section 17(5) of the CGST Act, the ITC on motor vehicles for the transport of persons is available when such vehicles are used in the further supply of such motor vehicles or for training on the driving of such motor vehicles.

- In addition, the Authority for Advance Rulings, Kerala, held that the input tax paid by the vehicle dealer on the purchase of a motor vehicle used for client display purposes can be used as an input tax credit for capital goods and offset against the output tax payable under the GST. Demo vehicles are either capital goods that are used in the process of operation or are eligible for the production tax credit.

Valuation under the GST Regime

- As per valuation laws, a special method is required in situations where a taxable supply is provided by a person engaged in the purchasing and sale of second-hand products, i.e. used products as such or after some slight processing, that does not modify the value of the goods and that no input tax credit has been used for the procurement of such goods.

- In such cases, the value of the supply shall be the difference between the selling price and the purchase price and shall be ignored if the value of the supply is negative. However, it should be noted that, if ITC is taken, above that the mentioned option-1 concessional rate is not available and the car dealer shall pay an amount equal to the

- on demo cars reduced by the percentage points that may be recommended or the transaction value tax on those capital goods determined as the value of the taxable supply, whichever is higher.

Concluding

- It varies depending on the wholesaler whether he wants to apply the concessional GST rate to the sale of demo vehicles for which he has not been able to make use of ITC and needs to fulfill other prescribed conditions.

- Alternatively, it can make use of ITC and make use of the same with the payment of the output tax liability and during the sale of demo vehicles.

Read Also : Overview of Input Tax Credit

GST Valuation on sale of used motor car/old vehicle

value of valuation of old car i.e. what shall be the value on which GST shall be applicable

As per the GST Notification, the Value of Supply shall be the “Margin of Supply”.

The margin of Supply means:-

1. in case the depreciation Claimed under Section 32 of Income Tax Act 1961:-

Where depreciation has been claimed on the said goods u/s 32 of the Income Tax Act 1961, the Margin of Supply shall be the difference between the Sale consideration received for supply of such goods and the depreciated value of such goods on the date of supply, and the margin of such supply shall be negative then it should be ignore.

2. In all other cases: –

The supply margin is the difference between the selling and purchasing prices, and it is ignored if the margin is negative.

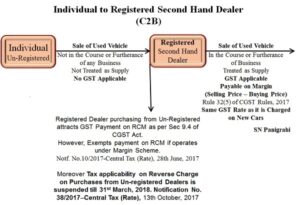

In case old or used car/ vehicle is Sold by Govt of India :-

In case the old/ used card/vehicle’s Supplier is State government, central govt, /Local authority, Union territory of the recipient is –

- In case unregistered person: Unregistered will have to obtain GST registration and pay GST

- in the case of registered person: Registered person will be liable to pay tax on RCM basis.

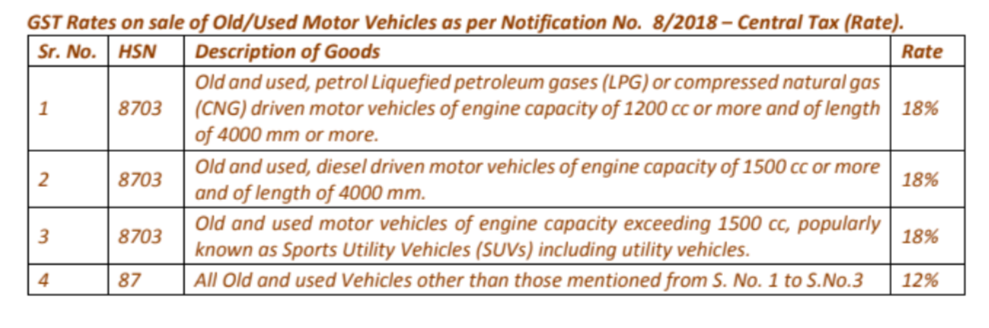

GST Rate on sale of used motor Car/ vehicles

list for the GST tax rate on Sale of OLD/old vehicles/Motor car

Conclusion on GST Applicable provision on GST on sale of old Car/vehicles.

Summary of GST Provisions is compiled here.

Popular Blogs :