Implications Rule 86B in CGST Rules, 2017

Page Contents

Rule 86B, introduced by Notification No. 94/2020 – Central Tax on December 22, 2020, effective from January 1, 2021, limits the use of Input Tax Credit for discharging output tax liability. Registered taxpayers with a monthly taxable turnover exceeding INR 50 lakh are required to pay at least 1% of their OTL in cash, overriding previous rules.

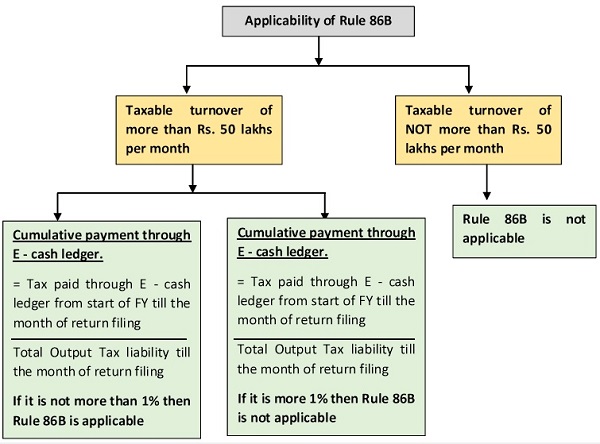

Applicability of Rule 86B:

Applicable to businesses with taxable turnover exceeding ₹50 lakh in a month. Exclusions: Turnover calculation excludes exempt and zero-rated supplies. Taxable Turnover Formula:

Taxable Turnover=Total Turnover−(ZeroRated Supplies + Exempted Turnover ) \ text{Taxable Turnover} = \text{Total Turnover} – (\text{Zero-Rated Supplies} + \text{Exempted Turnover})Taxable Turnover=Total Turnover−(Zero-Rated Supplies+Exempted Turnover)

Restrictions Imposed BY GST Law i.e ITC Utilization Cap: Only 99% of OTL can be discharged through Input Tax Credit. & At least 1% of OTL must be paid via mandatory Cash payment or using the electronic cash ledger.

Implication of Applicability of Rule 86B:

- Genuine businesses with low margins may face cash flow challenges despite maintaining accurate records.

- Businesses must plan tax payments carefully to ensure sufficient cash liquidity. Genuine businesses with low margins may face cash flow challenges despite maintaining accurate records. Businesses must plan tax payments carefully to ensure sufficient cash liquidity.

- Rule 86B curbs fraudulent activities like fake invoicing and generating counterfeit ITC for discharging fake output tax liability. It discourages practices of artificially inflating turnovers for financial credibility.

- Micro and small-scale businesses remain unaffected, as the rule applies only to turnovers exceeding ₹50 lakh/month.

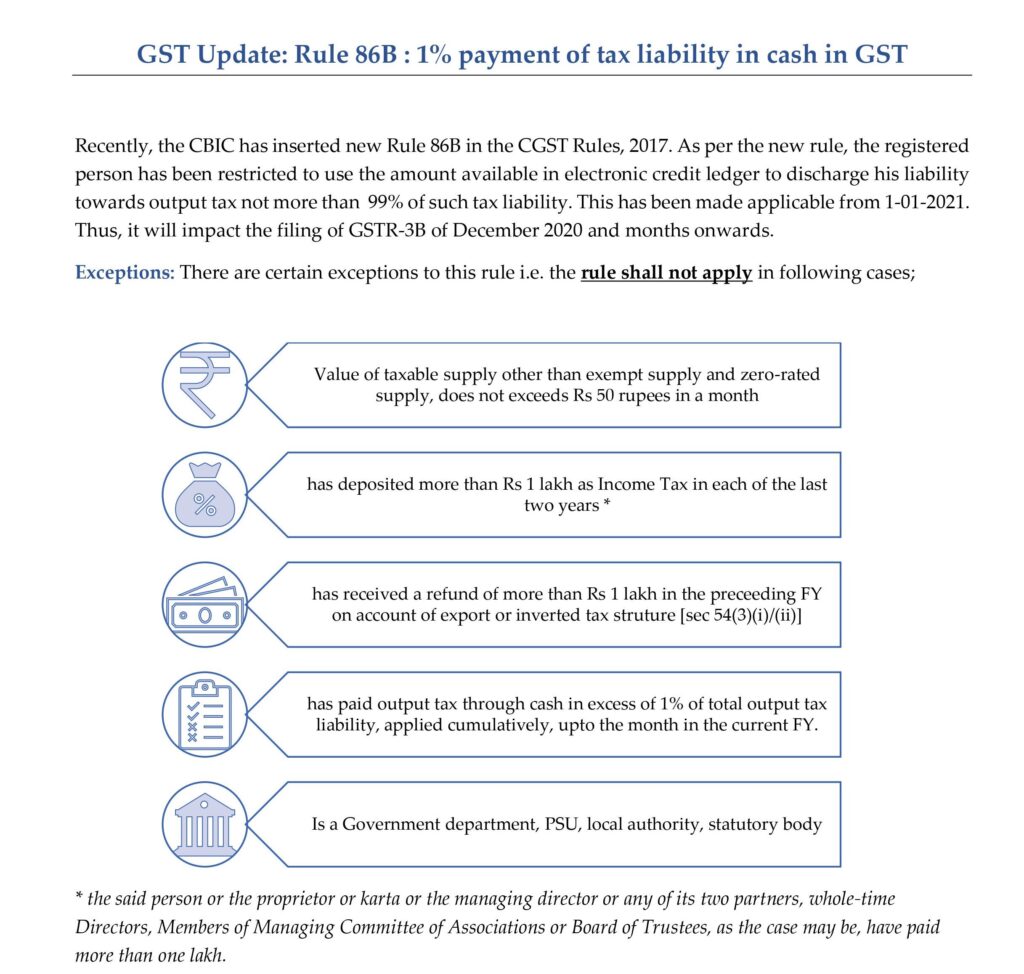

Exceptions to Rule 86B:

In the following cases are exempted (exceptions to Rule 86B) from the 1% cash payment requirement.

- Income Tax Filers: If the registered person (or their key personnel, such as proprietors, directors, or partners) paid income tax exceeding INR 1 lakh in the previous financial year.

- Refund Recipients: Businesses that received a refund of ₹1 lakh or more in the previous financial year for: Unutilized Input Tax Credit due to exports under LUT, or Inverted tax structure.

- Cash Payments in Past Financial Years: If output tax liability was discharged using electronic cash ledger exceeding 1% of total output tax liability in the current financial year. Government Entities i.e., Rule does not apply to local authorities, PSUs, statutory bodies, and government departments.

- Cash Payment and ITC Re-credit: The 1% output tax liability (OTL) paid in cash is eligible for ITC in subsequent periods, as it becomes part of the available ITC after payment. Businesses may face temporary cash outflows and subsequent adjustments, impacting working capital.

- Failure to meet the 1% cash payment requirement in time could lead to:

- Interest on delayed cash payment under Section 50 of the CGST Act (18% per annum).

- Recredit of Input Tax Credit does not eliminate the interest liability on the unpaid cash component.

Remittance of Tax via DRC-03:

- Use Form DRC-03 to voluntarily remit the required 1% cash component along with interest under Section 50 of the CGST Act. Taxpayers must be required to mention in the remarks column. The purpose of the remittance (e.g., compliance with Rule 86B). Details of excess remittance and intent to adjust it in the next month’s GSTR-3B.

- Utilization of Excess Remittance: The excess remitted amount can be claimed as input Tax credit in next month’s GSTR-3B, as it will reflect in the electronic credit ledger.

- Share a copy of the DRC-03 and relevant details with the GST department for transparency and to preempt any compliance queries.