Consequences of Not Filing Tax return on due date

Page Contents

Consequences of Not Filing ITR on Time

If you are mandated to file an Income Tax Return and miss the deadline, you can still file your tax return as a belated ITR. While it is possible to file a belated ITR, it is important to be aware of the penalties and potential complications that can arise from not filing your Income Tax Return on time. However, filing a belated Income Tax Return has several consequences, including penalties and the loss of certain benefits.

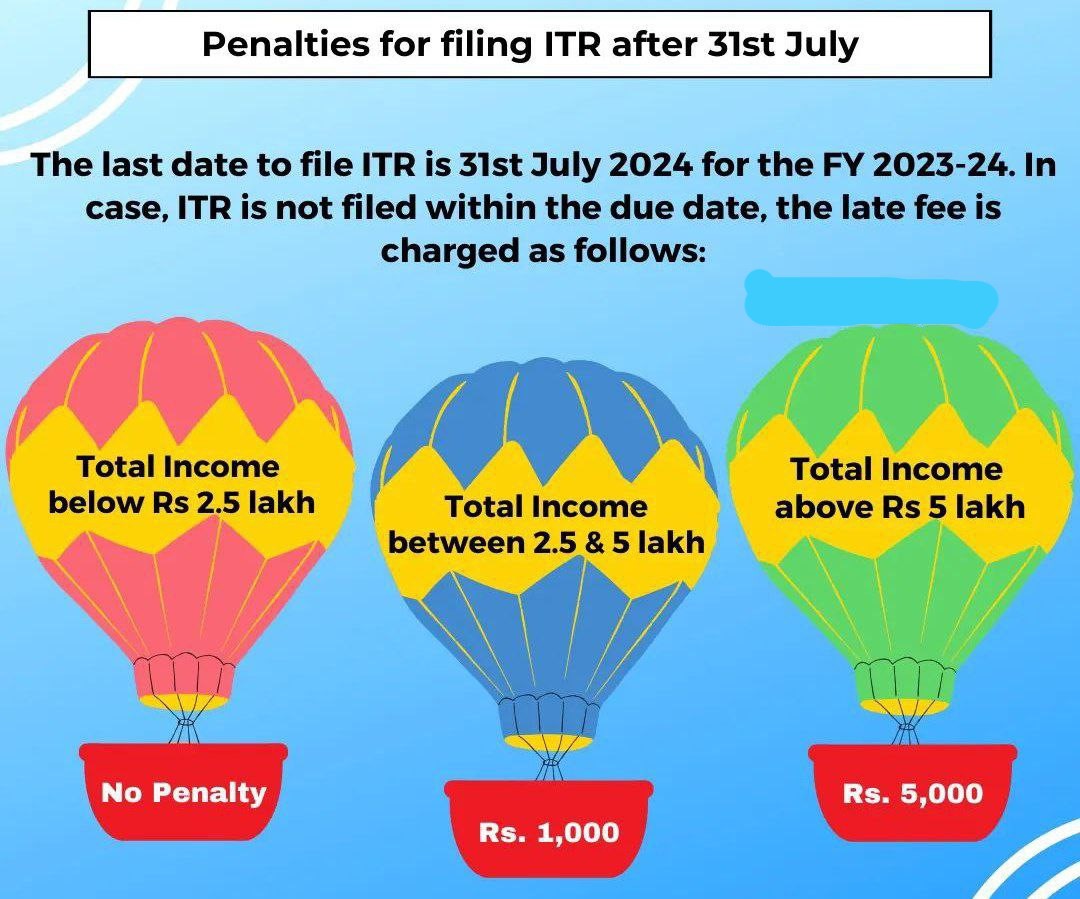

- Penalty Amount on Not Filing ITR on Time : A penalty of INR 5,000 is imposed if the ITR is filed after the deadline (July 31, 2023, for the FY 2023-24). If your taxable income is below INR 5,00,000/-, the penalty amount will not exceed INR 1,000.

- Interest on Tax Due : If you had a tax liability and did not file the Income Tax Return on time, a penal interest of 1% per month or part of the month on the outstanding tax amount will be levied from the due date until the date of filing the return.

- Loss of Carry Forward of Losses : You cannot carry forward certain losses (e.g., business loss, capital loss) to future years if you do not file the ITR by the due date.

- Delay in Receiving Refund : If you are due a tax refund, filing the Income Tax Return late will delay the processing of your refund, resulting in a longer wait for the refund amount.

- Reduced Time for Revision : The time available to revise a belated Income Tax Return is less compared to an ITR filed on time. This can be problematic if you later discover errors or omissions in your filed return.

- Ineligibility for Certain Deductions : You may lose the eligibility to claim certain deductions if you do not file the Income Tax Return within the due date.

- Increased Scrutiny and Notices: Late filing may attract scrutiny and notices from the Income Tax Department, leading to potential audits and additional compliance requirements.

This is a comprehensive overview of the different Income Tax Return forms and their applicability based on the type of income and taxpayer category. This breakdown should help you quickly identify which Income Tax Return form is applicable based on your specific income and situation. Here’s a summary to make it easier to understand:

Form ITR-1 (Sahaj)

- Who Can File:

- Salaried individuals with income from salary or pension.

- Individuals with income from one house property (excluding loss carried forward).

- Income from other sources (excluding lottery winnings or racehorses).

- Agricultural income up to INR 5,000.

Form ITR-2

- Who Can File:

- Residents with foreign assets or signing authority in any foreign account.

- Non-Resident or Not-Ordinarily Resident individuals.

- Individuals with agricultural income exceeding ₹5,000.

- Those who do not have income from business or profession.

Form ITR-3

- Who Can File:

- Individuals running a business as shopkeepers, traders, etc.

- Professionals like doctors, lawyers, consultants, and freelancers.

- Authors, artists, and individuals earning from artistic work.

- Individuals with rental income from commercial properties.

- Income from business/profession (other than presumptive income).

Form ITR-4 (Sugam)

- Who Can File:

- Small business owners opting for a presumptive income scheme under Sections 44AD, 44ADA, or 44AE.

- Freelancers like online content creators, bloggers, vloggers.

- Professionals whose income is computed on a presumptive basis.

- Individuals with a combination of salary and freelancing or part-time business income.

Form ITR-5

- Who Can File:

- Limited Liability Partnerships .

- Partnerships and other types of firms.

- Association of Persons and Body of Individuals.

- Artificial Juridical Persons like universities, temples.

- Estates of deceased or insolvent individuals.

- Business trusts (REITs/InvITs) and investment funds.

Form ITR-6

- Who Can File:

- Companies (except those claiming exemption u/s 11).

- Indian domestic companies and foreign companies.

- Companies not claiming exemption under section 11 for charitable or religious purposes.

Form ITR-7

- Who Can File:

- Individuals receiving income from property held under trust for charitable or religious purposes (Section 139 (4A)).

- Political parties (Section 139 (4B)).

- Scientific research institutions (Section 139 (4C)).

- Universities, colleges, or other institutions (Section 139 (4D)).

Due Dates of Filling of ITR

- Non-audited taxpayers: July 31st of the AY.

- Taxpayers requiring an audit (including companies): September 30th of the AY.