Comprehensive Changes in Form 3CD & related changes

Page Contents

Main Changes in Form 3CD and other changes

This is a comprehensive summary of the amendments in Income-tax (Eighth Amendment) Rules, 2025 to Form 3CD and other changes introduced by Amendments particularly affecting non-residents operating cruise ships, tax audit reporting (Form 3CD), and taxation of buybacks. The amendments to Form 3CD indicate the government’s focus on improving transparency, particularly in areas like cryptocurrency transactions and digital assets. The Income-tax (Eighth Amendment) Rules, 2025 emphasis on penalties for non-compliance means businesses and tax professionals must be extra cautious in ensuring accurate reporting. The mandatory e-filing requirement aligns with the broader push for digital governance, reducing manual intervention and streamlining audit processes. Details are mentioned here under:

Attention all finance & Tax Professionals : Changes in Form 3CD

-

New Section 44BBC for Cruise Ships (Effective from April 1, 2025) : New Clause Inserted: Clause 12: New section 44BBC added alongside 44BBB, 20% of gross receipts from passenger carriage will be deemed as taxable business income for non-residents operating cruise ships. which Aimed at simplifying tax compliance for foreign cruise operators.

-

Changes to Form 3CD for Tax Audits

-

Clause 21: Clause 21 Updated: New row added for expenditure incurred to settle proceedings under law notified by the government. Reporting now required for expenses related to settling legal proceedings for notified contraventions.

- Clauses Omitted from Clause 19: 32AC, 32AD, 35AC & 35CCB – GONE

- Clause 22 Substituted: MSME Act compliance detailed: Disallowance of interest u/s 23. and Amounts unpaid beyond due date under section 15 – to be disclosed & disallowed.

-

Clause 22 (MSME Disclosure):

-

Interest inadmissible under MSMED Act.

-

Total dues to MSMEs and payments made within or beyond the time limit under Section 15 of MSMED Act.

-

-

Clause 26 (Section 43B Adjustments): Clause 26 Modified: Removed lettered sub-points (a) to (g). Replaced “allowed” with “allowable”.Now explicitly covers delayed payments to MSMEs.

-

Removal of Clauses 28 & 29: Related to share transactions under Section 56(2)(viia) & (viib) (likely to reduce redundancy or shift reporting elsewhere).

-

Clause 31 (Loans & Deposits Reporting): Clause 31 Updated: Dropdown-based codes to be used for loans, deposits & repayments. Addition of a dropdown for specifying mode of transaction (Cash, Journal Entry, Asset/Liability Transfer, etc.). Note 1 Inserted – 12 nature codes like Cash (A/B), Journal Entry (I/J), Transfer of Assets (E), etc.

-

Clause 36B (Buyback of Shares Reporting): From October 1, 2024, buybacks will be taxed in the hands of the shareholder as deemed dividend. Details required for buyback of shares u/s 2(22)(iv): Amount received , Cost of acquisition. Clause 36B Inserted Details required for buyback of shares u/s 2(22)(iv), Amount received, and Cost of acquisition

-

Impact Analysis of Changes in Form 3CD:

-

Cruise Operators: 44BBC provides clarity and a presumptive taxation regime for non-resident cruise businesses.

-

Businesses & Auditors: Enhanced MSME reporting ensures better compliance with payment timelines. The additional disclosures, especially regarding related-party transactions and digital assets, suggest that the government is intensifying its monitoring of financial activities to curb tax evasion and ensure compliance.

-

Buyback Taxation: Shift from corporate taxation to individual taxation aligns it with dividend taxation, impacting shareholders.

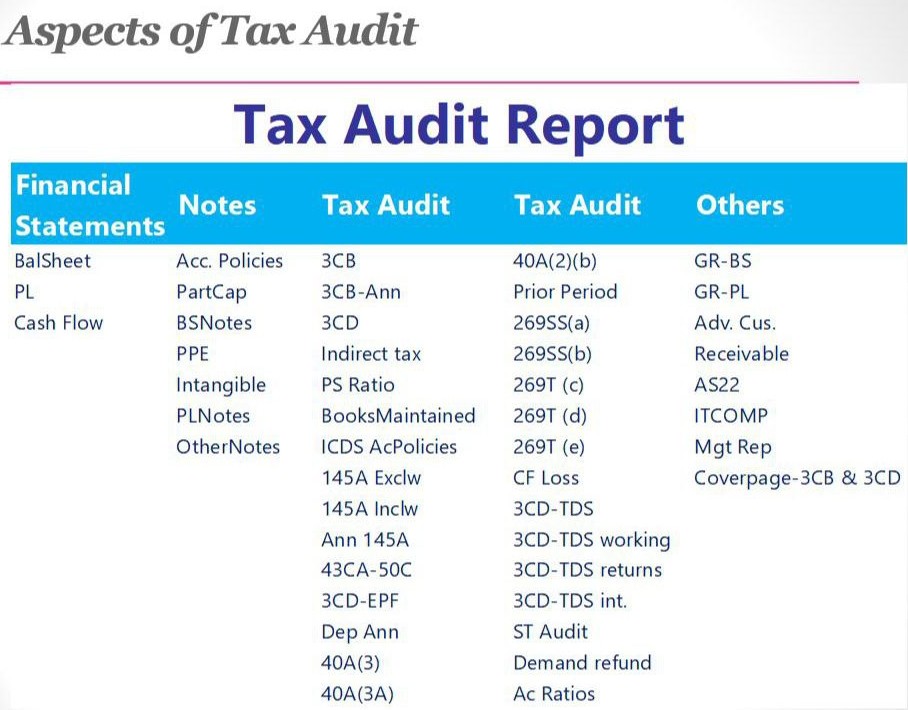

key aspects involved in a Tax Audit Report,

Tax Audit Report linking various financial statements, notes, tax audit references (forms/sections), and other related compliance elements. Here’s a detailed breakdown for better understanding:

Financial Statements & Corresponding Notes

-

Balance Sheet

-

Notes: Accounting Policies

-

Key Tax Audit Forms: 3CB, 3CD

-

Related Sections: 40A(2)(b)

-

Others: GR-BS (General Review – Balance Sheet)

-

-

Profit & Loss (P&L)

-

Notes: PartCap (Partner’s Capital), PLNotes

-

Key Forms: 3CB-Ann, 3CD

-

Relevant Tax Points: Prior Period, Indirect Tax, PS Ratio, Section 269SS(a)(b)

-

Others: GR-PL, AS22 (Accounting for Taxes), ITCOMP (IT Computation), Mgt Rep (Management Representation)

-

-

Cash Flow

-

Notes: BSNotes (Balance Sheet Notes), OtherNotes, Intangible, PPE (Property, Plant & Equipment)

-

Tax Points: CF Loss, Books Maintained, ICDS Accounting Policies

-

Sections: 269T(c)(d)(e), 145A incl./excl., 43CA-50C, 40A(3), 40A(3A)

-

Others: Receivables, Coverage of Form 3CB & 3CD

-

Detailed Tax Audit Checklist (Forms & Sections)

| Type | Details |

|---|---|

| Forms | 3CB, 3CD, 3CD-EPF, 3CD-TDS (working/returns/int.), 3CB-Ann |

| Sections & Concepts | 40A(2)(b), 269SS(a)(b), 269T(c)(d)(e), 145A (Inclw/Exclw), 43CA-50C, ST Audit |

| Others | ICDS Accounting Policies, Depreciation, Accounting Ratios, Demand Refund |

Interpretation of Key Terms

-

GR-BS / GR-PL: General Review of Balance Sheet / Profit & Loss Account

-

AS22: Accounting Standard 22 (Deferred Tax)

-

145A Inclw / Exclw: Reporting under Section 145A for method of accounting

-

ICDS AcPolicies: Income Computation and Disclosure Standards

-

3CD-TDS: Reconciliation of TDS sections under Form 3CD

-

ST Audit: Service Tax Audit

-

Mgt Rep: Management Representation Letter

Usage This below chart is a practical reference during:

-

Preparing Form 3CB & 3CD

-

Reviewing compliance under various Income Tax Sections

-

Auditing Books of Accounts under Section 44AB

-

Ensuring disclosure per ICDS and Accounting Standards

-

Finalizing Audit Reports with Management Notes