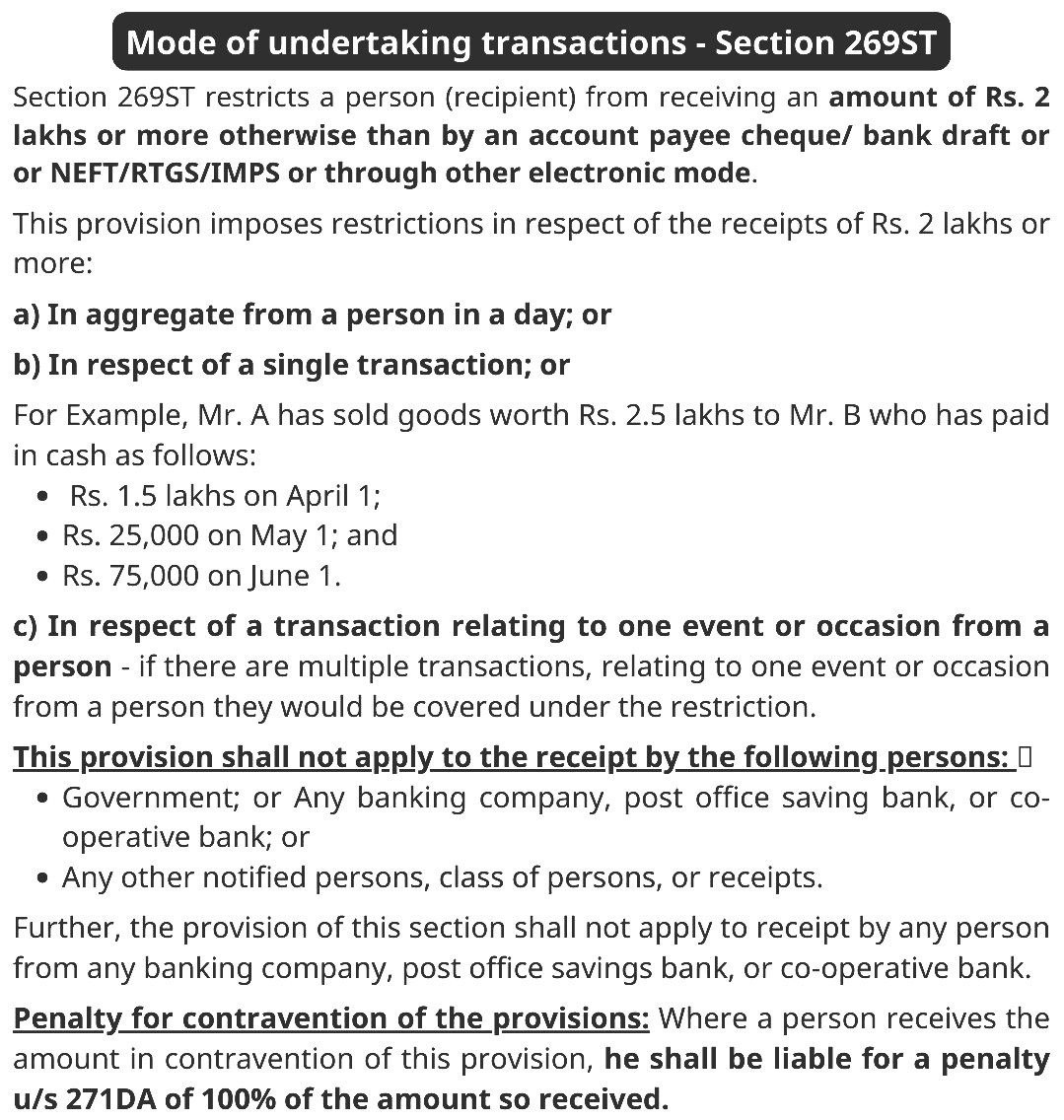

Partner capital introduce not deemed as loan invoke 269SS

Page Contents

CAPITAL INTRODUCED BY PARTNERS IN THE FIRM COULDN’T BE DEEMED AS LOAN TO INVOKE PROVISIONS OF SEC. 269SS

- Section 269SS, read with section 271D, of the Income-tax Act, 1961 – Deposits – Mode of taking/accepting (Amount Contributed by partners of firm)

- Provisions of section 269SS would not be violated when money is exchanged inter-se between partners and partnership firm in spite of fact that partnership firm and individual partners are separate assessees [2015] –

HIGH COURT OF DELHI – CIT v. Muthoot Financiers

FACTS OF CASE

- The assessee-firm was involved in the business of banking. It was registered under the Kerala Money Lending Act.

- During the course of the assessment proceedings, the Assessing Officer found that the firm had accepted payments from the partners in cash.

- Assessing Officer taking a view that the partners and the firm being two distinct and separate entities, they would also fall in the mischief of section 269SS.

- The Assessing Officer thus imposed penalty under section 271D.

- Commissioner (Appeals) upheld the order of the Assessing Officer.

- The Tribunal, however, opined that the amount brought by the partner to the firm could not be said to be a loan. It was also not in dispute that the amount taken was capital of the firm in view of language of the section 269SS.

- Tribunal thus taking a view that amount brought by the partner to the firm in these circumstances, be it in cash could not be said to have violated the terms of section 269SS, set aside the impugned penalty order.

- On revenue’s appeal the High Court Held in favour of assessee

- The question raised is whether in a transaction between the firm and the partner the provision of section 269SS would be attracted and if section 269SS was attracted and therefore violated, whether the assessee would be entitled to benefit of section 273B.

- Emerges position is that there are three different High Courts, which have held that section 269SS would not be violated when money is exchanged inter se between the partners and partnership firm in spite of the fact that the partnership firm and individual partners are separate assessees.

- The opposite view is also possible. Keeping in view that three different High Courts have taken a consistent view of the facts, which are similar to the facts in the present case, which includes the judgment of the Madras High Court as late as in the year 2013, the same line of reasoning given by the Madras High Court in the case of CIT v. V. Sivakumar is followed.

Held

- Having said that, it is clear that any interest, salary, bonus, commission or remuneration paid by a firm to any of its partners should be regarded as a mode of adjusting the amount that must have been taken to have been contributed to the partnership assets by a partner, who can really contribute in kind as well as in money.

- Applying this principle, it is opined that the transaction effected in these cases cannot partake the colour of loan or deposit and as such, section 269SS nor section 271D would come into play.

- It is undisputed fact that the money was brought by the partners of the assessee-firm. The source of money has also not been doubted by the revenue. The transaction was bona fide and not aimed to avoid any tax liability.

- Creditworthiness of the partners and genuineness of the transactions coupled with the relationship between the ‘two persons’ and two different legal interpretations put forward could constitute a reasonable cause in a given case for nor invoking sections 271D and 271E.

- Section 273B would come to the aid and help of the assessee.

- In view of aforesaid, it is held that the appeal filed by the revenue is devoid of any merit and, same is accordingly dismissed.

Violation or contravention of Section 269T

For query or help, contact: singh@carajput.com or call at 011-435 201 94