Can Employer Restrict their PF contribution to 1,800/Month

Page Contents

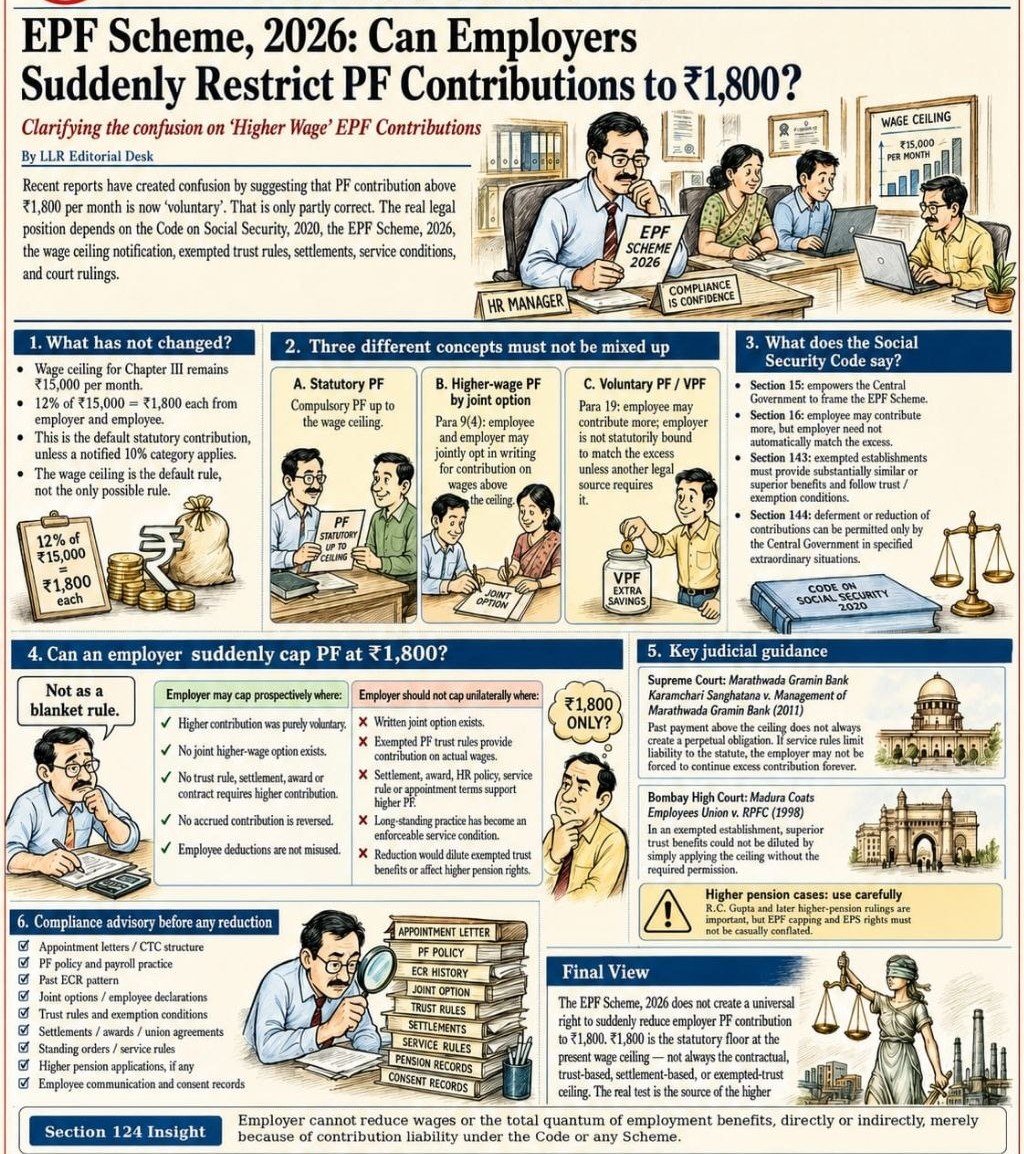

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800?

A question is currently circulating across HR departments, payroll teams, finance functions, and compliance forums: “Can employers now restrict their Provident Fund contribution to ₹1,800 per month?”

The question arises from growing discussions around the EPF Scheme, 2026, and the continuation of the statutory wage ceiling of INR 15,000 per month for PF purposes.

At first glance, the calculation appears straightforward:

- Wage Ceiling = ₹15,000

- Employer Provident Fund Contribution = 12%

- Employee Provident Fund Contribution = 12%

Therefore: INR 15,000 × 12% = INR 1,800

This has led many employers to believe that INR 1,800 is now the maximum amount they are legally required to contribute toward an employee’s Provident Fund account. However, the legal position is far more nuanced.

The INR 1,800 figure represents the statutory contribution under the wage ceiling, but it does not automatically permit every employer to reduce existing higher PF contributions overnight.

Understanding the Source of the Confusion

Recent discussions have created an impression that any Provident Fund contribution above INR 1,800 is purely voluntary and may therefore be discontinued at the employer’s discretion. That understanding is only partially correct.

While the statutory framework recognizes the wage ceiling for compulsory Provident Fund contributions, many employers have historically contributed on actual wages or higher wages due to joint options exercised with employees, employment contracts, company policies, settlements and awards, exempted PF trust rules, and long-standing payroll practices.

As a result, the critical legal question is not “Does the EPF Scheme mention INR 1,800?” Instead, the real question is “What is the legal source of the higher PF contribution?”

Three PF Concepts Every Employer Must Distinguish

One of the biggest compliance mistakes is treating all PF contributions as identical. In reality, there are three distinct categories.

1. Statutory Provident Fund Contribution

This is the minimum mandatory contribution prescribed under the EPF framework. Under the current wage ceiling:

- Provident Fund is compulsory up to INR 15,000 in wages.

- Employer contributes 12%.

- Employee contributes 12%.

This results in an INR 1,800 employer contribution and an INR 1,800 employee contribution. This remains the default statutory position.

2. Higher-Wage PF Contribution

Many establishments contribute to the Provident Fund on wages exceeding INR 15,000.

Such contributions may arise due to written joint options, historical practice, service conditions, Employment contracts, Internal policies and Settlements with employees or unions. In these situations, higher Provident Fund contributions may acquire legal significance beyond the statutory minimum.

Therefore, an employer cannot automatically assume that higher contributions can be withdrawn without examining the basis on which those contributions were being made.

3. Voluntary Provident Fund (VPF)

VPF is often confused with higher-wage Provident Fund contributions. However, the two are different. Under Voluntary Provident Fund:

- Employees may choose to contribute more than the statutory rate.

- The employer is generally not obligated to match the additional employee contribution.

Unless a separate contractual or statutory obligation exists, VPF does not automatically increase employer liability.

Can Employers Unilaterally Cap Provident Fund Contributions at INR 1,800?

The answer is no, not as a blanket rule. Employers must evaluate the legal foundation of the existing contribution structure before making any changes.

Employer May Consider Prospective Capping Where:

- No written joint option exists.

- Higher contribution was purely voluntary.

- No trust rules require contributions on higher wages.

- There is no settlement, award, or agreement that mandates actual wage contributions.

- No vested employee benefit is being withdrawn.

- Also, no accrued contribution is being reversed.

In such circumstances, a carefully structured prospective change may be possible, subject to legal review.

Situations Where Reduction Can Become Risky

Employers should proceed with extreme caution where

- Written Joint Options Exist: If the employer and employee have jointly opted for a contribution on wages above the ceiling, unilateral withdrawal may be challenged.

- Exempted Provident Fund Trust Rules Provide Better Benefits: Exempted establishments are often governed by trust rules that may prescribe superior benefits compared to the statutory minimum.

- Employment Contracts Promise Higher Provident Fund: Appointment letters and CTC structures may create contractual obligations that cannot be casually ignored.

- Settlements and Awards Govern Contributions: Industrial settlements, awards, and collective bargaining arrangements may provide stronger employee protections.

- Long-Standing Practice Has Become a Service Condition: Consistent contribution on actual wages over a long period can potentially become an enforceable condition of service.

- Higher Pension Rights Are Involved: Reduction of provident fund contributions may have implications on pension entitlements and related employee rights.

What Do the Courts Say?

Indian courts have repeatedly emphasized that Provident Fund disputes cannot be decided merely by looking at the statutory ceiling. The surrounding contractual and service conditions matter.

Supreme Court: Marathwada Gramin Bank Case

In Marathwada Gramin Bank Karmachari Sanghatana v. Management of Marathwada Gramin Bank (2011), the Supreme Court examined issues relating to benefits extended beyond statutory requirements. The ruling highlighted that the existence of statutory minimum obligations does not automatically determine every employment benefit issue.

The legal position must be tested against applicable service rules, policies, and governing arrangements.

Bombay High Court: Madura Coats Case

The Bombay High Court emphasized that in exempted establishments, trust benefits and superior arrangements cannot be diluted casually by merely relying on the statutory wage ceiling. The judgment reinforces the importance of examining the source of employee entitlement before attempting any reduction.

The Section 124 Angle Under the Social Security Code

Another aspect often overlooked is Section 124 of the Code on Social Security, 2020. The provision broadly protects employees against reductions in wages or employment benefits merely because an employer has statutory contribution obligations under a social security scheme.

This becomes particularly relevant where organizations attempt to restructure wages, reduce allowances, alter remuneration packages, and offset Provident Fund costs through benefit reductions. Any such proposal requires careful legal evaluation.

Compliance Checklist Before Any Provident Fund Reduction

Before modifying PF contributions, employers should conduct a detailed review of:

Employment Documentation

- Appointment letters

- Employment contracts

- CTC structures

- HR policies

PF Records

- Past ECR filings

- Historical contribution patterns

- Payroll records

Employee Declarations

- Joint option forms

- Employee consent records

- Higher pension applications

Industrial Relations Documents

- Settlements

- Awards

- Collective bargaining agreements

- Union arrangements

Trust Documentation

- Exempted trust rules

- Trust deeds

- Exemption conditions

Service Conditions

- Existing employment benefits

- Established payroll practices

- Internal regulations

Final Takeaway

The EPF Scheme, 2026, does not create a universal right for employers to suddenly reduce Provident Fund contributions to INR 1,800 per month. While INR 1,800 remains the statutory contribution calculated on the current wage ceiling of INR 15,000, many organizations may have additional obligations arising from joint options, employment contracts, trust rules, settlements, company policies, and long-standing service conditions. Therefore, the key issue is not whether INR 1,800 appears in the scheme.

The real issue is, what is the legal source of the higher Provident Fund contribution?

Before implementing any reduction, employers should undertake a comprehensive legal, payroll, and compliance review. A premature decision to cap Provident Fund contributions may expose the organization to disputes, claims, and litigation.

Golden Rule for Employers

INR 1,800 may be the statutory floor under the wage ceiling, but it is not automatically the contractual, settlement-based, or trust-based ceiling for every establishment.