Clubbing of Income & Tax Logic Behind Gifting Assets

Page Contents

Understanding Clubbing of Income & Tax Logic Behind Gifting Assets

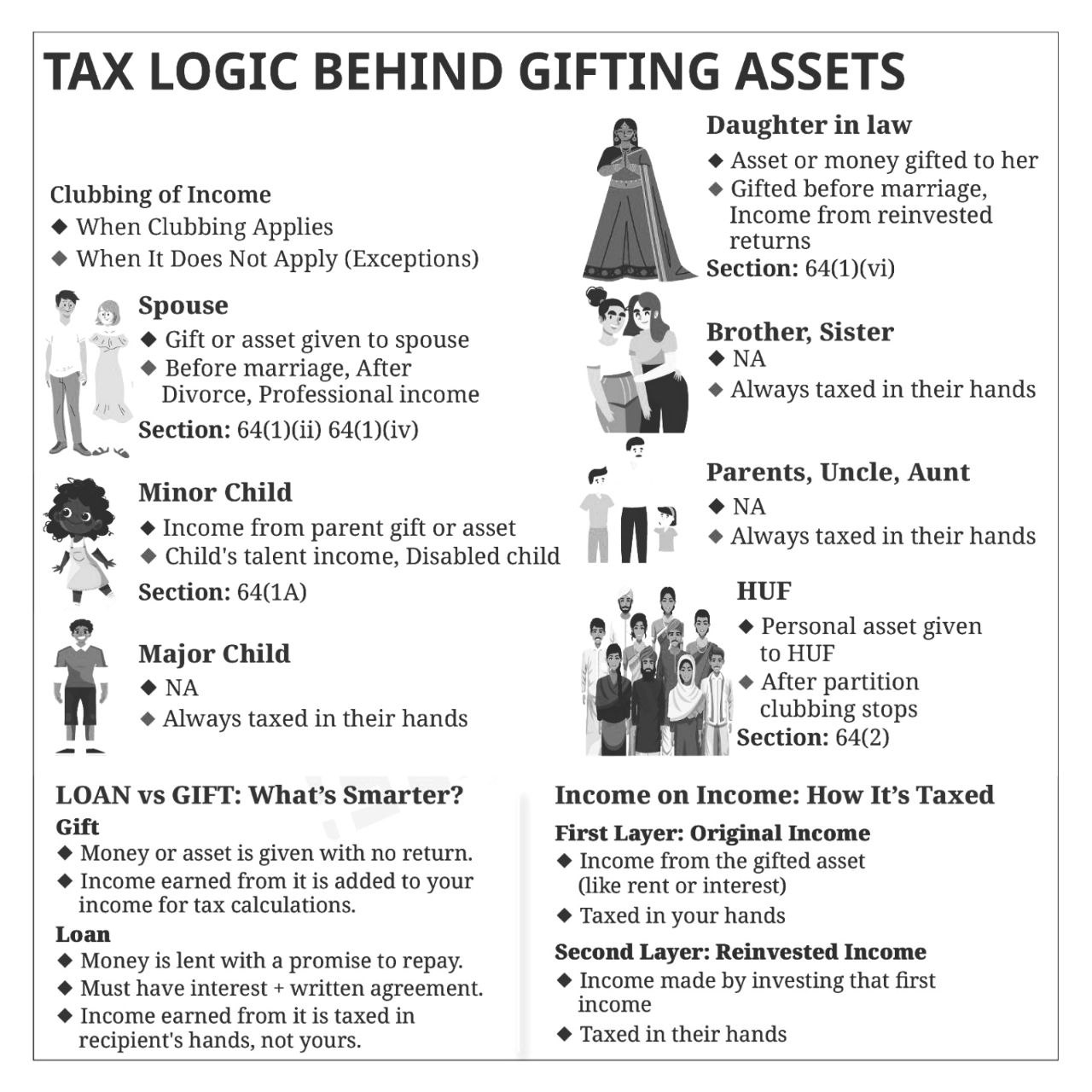

Gifting money or assets to family members is a common tax and estate planning tool. However, many taxpayers assume that once an asset is gifted, all future income automatically becomes taxable in the recipient’s hands. This is not always true. The Income Tax Act contains Clubbing of Income provisions u/s 64, which are designed to prevent tax avoidance by transferring assets to family members in lower tax brackets.

What is clubbing of income?

Clubbing means that although an asset has been transferred to another person without adequate consideration, the income arising from that asset may still be taxed in the hands of the transferor (giver) rather than the recipient. The law mainly covers transfers to a spouse, minor child, son’s wife (daughter-in-law), AND Hindu Undivided Family. The following are key tax planning takeaways:

Before gifting assets, understand not only whether the gift itself is tax-free but also who will ultimately pay tax on the income generated from that gifted asset. This is where the clubbing provisions of the income tax Act become crucial. The following are tax planning aspects:

- Income is clubbing generally applies for gifts to a spouse, minor child, daughter-in-law, and certain transfers to Hindu Undivided Family..

- Clubbing does not normally apply to gifts made to major children, parents, brothers, sisters, or other relatives not covered by Section 64.

- Only the first layer of income is generally clubbed; income earned from reinvestment of that income is taxable in the recipient’s hands.

- Proper documentation should always be maintained for gifts and loans.

- Tax planning must be based on genuine transactions and commercial substance, not merely on shifting income to lower tax brackets.

Special case of clubbing of income

Gift to Spouse: When Clubbing Applies [Section 64(1)(iv)]:

If an individual transfers money, shares, mutual funds, fixed deposits, immovable property, or any other asset to their spouse without adequate consideration, any income arising from such transferred asset is generally clubbed with the income of the transferor (donor spouse) and taxed in the donor’s hands. For Examples: Interest from gifted money invested in an FD, dividends from shares purchased out of gifted funds, and rent from a property gifted to spouse. And capital gains arising from the transfer of the gifted asset. The following are exceptions—when clubbing does not apply:

- Gift Made Before Marriage: The relationship of husband and wife must exist both at the time of transfer and at the time income arises. Therefore, if the asset was gifted before marriage, subsequent income is taxable in the recipient’s own hands.

- After Divorce: If the marital relationship ceases due to divorce, income arising thereafter is not clubbed and is taxable in the hands of the recipient spouse.

- Transfer for Adequate Consideration: Where the spouse acquires the asset by paying adequate consideration, Section 64(1)(iv) does not apply.

- Transfer in Connection with an Agreement to Live Apart: Assets transferred under a separation arrangement are outside the scope of clubbing provisions.

- Income from Professional Skills or Expertise: Where income is earned by the spouse through their own professional qualifications, technical knowledge, specialised skills, talent, or personal efforts, such income is taxable in the spouse’s own hands and is not clubbed

In case of a gift to a minor child: when clubbing applies:

U/s 64(1A) any income arising from money, investments, property, or other assets gifted to a minor child is generally clubbed with the income of the parent whose total income (before clubbing) is higher. While investment income from gifted assets is generally clubbed with the parent’s income, income generated through the minor child’s own talent, expertise, or disability-related exception is taxed independently in the child’s hands. following Summary

| Particulars | Taxability |

|---|---|

| Income from assets gifted to a minor child | Clubbed with income of the higher-earning parent |

| in case Income earned through acting, singing, sports, talent, or specialized skills | Taxable in minor child’s own hands |

| Income of a disabled child covered under Section 80U | it is Taxable separately in child’s own hands |

Gift to Major Child: Clubbing Does Not Apply:

Once a child becomes a major (18 years or above), assets can be gifted freely. And future income is taxable in the hands of the major child.

In case Gift to Daughter-in-Law: When Clubbing Applies:

Income arising from assets transferred directly or indirectly to the son’s wife without consideration is clubbed with the income of the donor. Relevant Section: 64(1) (vi)

Gift to Brother or Sister: No clubbing provisions apply.

Transfer of Asset to Hindu Undivided Family:

When Clubbing Applies: If a member transfers personal property to a Hindu Undivided Family. without adequate consideration: Income from such transferred assets will be clubbed with the transferor’s income.

- After Partition: Once partition occurs, clubbing ceases; income becomes taxable as per ownership after partition.

Income on Income Concept

- Understanding “Income on Income”: This is one of the most misunderstood concepts.

- First Layer Income: Income directly generated from a gifted asset. Examples: Rent from gifted property, interest from a gifted fixed deposit, and dividend from gifted shares. This income is clubbed wherever Section 64 applies. First Layer Income (Clubbed) : Mr. A gifts INR 10 lakh to his spouse. Fixed deposit Interest = INR 80,000, then INR 80,000 is taxable in Mr. A’s hands.

- Second Layer Income: Now suppose Wife reinvests INR 80,000 in interest. And earns another INR 8,000 in interest. Then This INR 8,000 is called “income from income.” Second layer income is not clubbed.

| Particulars | Taxable In |

|---|---|

| Interest on gifted Fixed deposit | Transferor spouse bearing the income |

| Interest on reinvested interest | Recipient spouse bearing the income |

Taxable in the wife’s hands. And clubbing applies only to first-generation income. This is known as the income-on-income principle.

Loan vs Gift: Which is Better?

- When Gift: There is no repayment obligation; clubbing provisions may apply. And income may remain taxable in the donor’s hands.

- In case of a loan: There is money given under a proper loan agreement; the borrower is required to repay and ideally carries reasonable interest. Income arising from funds used by borrowers is taxable in the borrower’s hands. Clubbing provisions generally do not apply if the transaction is a genuine loan.

Can Income from Assets Gifted to a Spouse be Clubbed with the Donor’s Income?

Yes, u/s 64(1)(iv) of the Income Tax Act states that if an individual transfers any asset (directly or indirectly) to his/her spouse without adequate consideration, the income arising from such asset is clubbed with the income of the transferor-spouse and taxed in the hands of the donor. following key rule applicable

- Asset gifted to spouse without consideration and

- Income generated from that asset remains taxable in the hands of the spouse who made the gift

This provision applies even if the spouse changes the form of the asset after receiving it.

Change in Form of Asset Does Not Avoid Clubbing: Important Principle

| Asset Gifted | Asset Purchased by Spouse | Taxability |

|---|---|---|

| Cash in hand | Fixed deposit | Income will be clubbed. |

| Cash in hand | Mutual Fund | In this case, income will be clubbed. |

| Cash in hand | Shares | Income will be clubbed. |

| Cash in hand | Debentures | In this case, income will be clubbed. |

| Gold and jewelry | Sold and invested elsewhere | Income will be clubbed. |

The law follows the source of funds, not merely the form of the asset.

Hindu Undivided Family vs. Individual Taxpayer

An Hindu Undivided Family can be beneficial where there are genuine family-owned income sources, such as ancestral property, Hindu Undivided Family investments, or a family business. In other cases, the additional compliance requirements may outweigh any tax advantages.

| Parameter | Hindu Undivided Family | Individual |

|---|---|---|

| Tax Status Applicability | Separate taxable entity with its own Permanent Account Number and income tax return | Taxable in own capacity using personal Permanent Account Number and income tax return |

| Tax Slabs applicable | Entitled to a separate set of tax slabs (subject to the chosen tax regime) | One set of tax slabs per individual |

| Most Suitable For | Income from ancestral property, Hindu Undivided Family-held investments, and family businesses | Salary, professional income, and personally held investments |

| Compliance Requirements | Requires separate books of account, bank account, and tax return filing | Generally simpler, with a single set of records and return |

| Risk Considerations | Artificial diversion of income may attract scrutiny and penalties | Lower risk of entity-related challenges, though regular tax scrutiny still applies |

Exceptions Where Clubbing of Income Provisions Do Not Apply

Basic Key Principle in Clubbing: Provisions are intended to prevent tax avoidance through transfers without consideration. Therefore, where the relationship does not exist, adequate consideration is paid, or income is generated through the spouse’s own professional efforts and skills, clubbing provisions generally do not apply. The clubbing provisions under Section 64 generally do not apply in the following situations:

- Gift Made Before Marriage: Where an asset or amount is transferred to a person before the marriage takes place, the income subsequently earned from such asset is not subject to clubbing after marriage.

- Transfer Made After Divorce: If the transfer of an asset takes place after the marital relationship has legally ended, the income arising from the transferred asset is taxable in the hands of the recipient and not in the hands of the transferor.

- Income Earned Through Personal Skill or Professional Expertise: Income derived by the spouse from the application of professional knowledge, technical qualifications, specialized skills, talent, experience, or personal efforts is assessed in the spouse’s own hands and is not covered by clubbing provisions.

- Transfer for Adequate Consideration: Where an asset is transferred in exchange for adequate and genuine consideration, the transaction is treated as a bona fide transfer and the clubbing provisions are not attracted.

| Situation | Clubbing Applicable? |

|---|---|

| The taxpayer made an asset that was gifted before marriage | In thus case No clubbing |

| Asset transferred after divorce | No clubbing |

| In case the Income earned by spouse through profession, skill, talent or technical expertise | In this case No clubbing |

| if the taxpayer made the Asset transferred for adequate consideration | No clubbing |