Salary Rs 12.75 Lakh Still but Have to Pay Tax in FY 2025-26

Page Contents

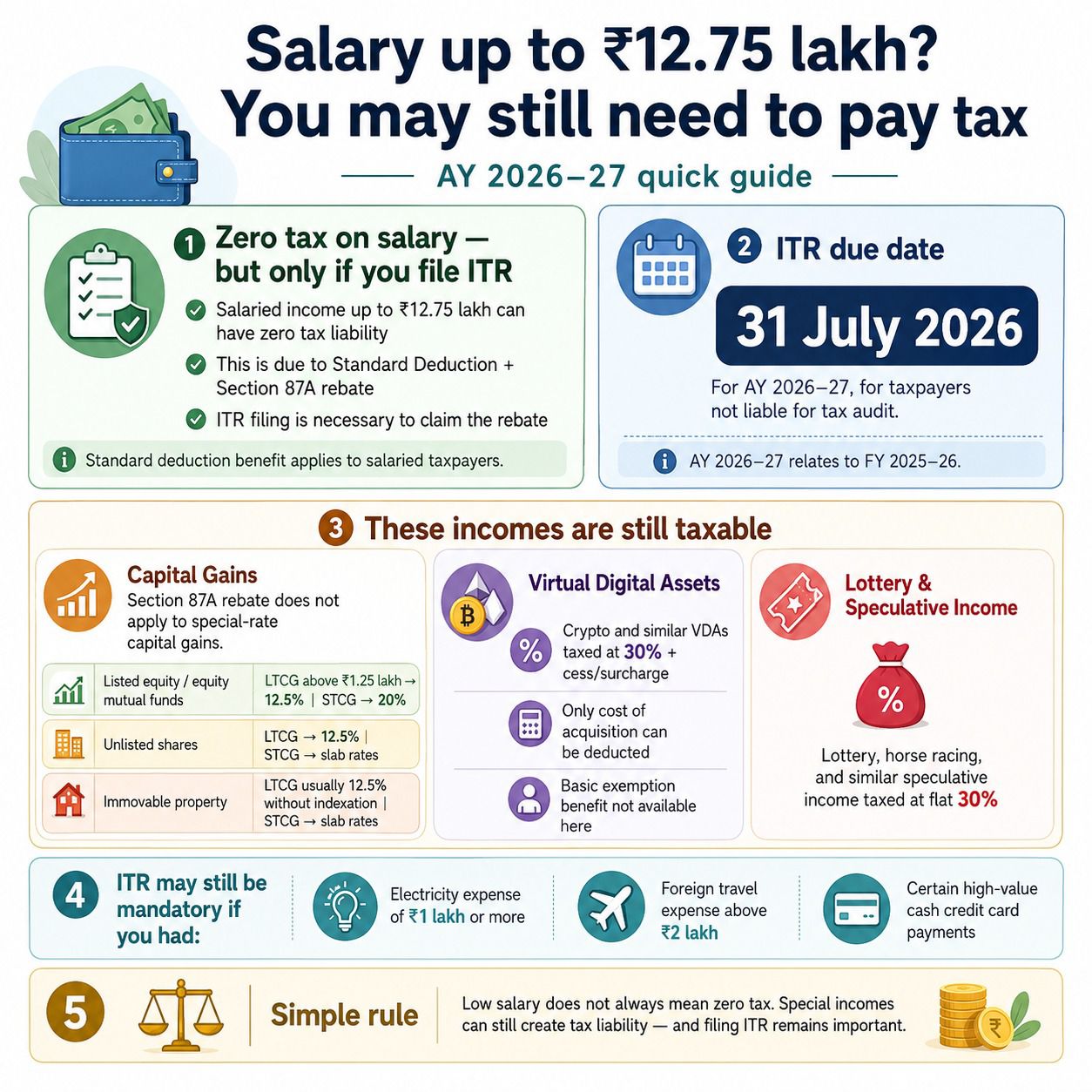

Salary up to INR 12.75 Lakh? You May Still Have to Pay Tax in FY 2025-26 (AY 2026-27)

Many salaried taxpayers believe that income up to INR 12.75 lakh is completely tax-free under the new tax regime. While this is broadly true for pure salary income, there are important exceptions that can still create a tax liability. Understanding these exceptions can help taxpayers avoid surprises while filing their income tax return for AY 2026-27.

The INR 12.75 Lakh Tax-Free Myth Explained

- Following the changes announced in the Union Budget, salaried individuals under the new tax regime can effectively have zero tax liability on salary income up to INR 12.75 lakh, thanks to Rebate U/s 87A and Standard Deduction available to salaried taxpayers. However, there is one critical condition:

- Taxpayer must file your income tax return to claim the rebate. Many taxpayers mistakenly assume that no tax is payable under all circumstances if their total income is below INR 12.75 lakh. This is not entirely correct.

Why Filing ITR is Still Important

- Even when tax liability becomes nil due to the Section 87A rebate, filing the return remains important because It is necessary to claim the rebate, it serves as proof of income, It helps in visa applications and loan approvals, and It establishes tax compliance records. For AY 2026-27, taxpayers not liable for audit are generally required to file their income tax return by 31 July 2026.

Incomes That Can Still Attract Tax

1. Capital Gains Can Still Trigger Tax Liability

Capital Gains Tax Rates Applicable for AY 2026-27 Despite Salary Being Below INR 12.75 Lakh. Many taxpayers assume that if their salary income is within ₹12.75 lakh, they will not pay any tax. But Section 87A rebate does not fully eliminate tax on certain capital gains taxed at special rates. Section 87A rebate is generally not available against tax payable on special-rate capital gains. So even if the taxpayer’s salary is below INR 12.75 lakh, the taxpayer may still have to pay tax on it. The following table explains the applicable tax treatment:

Listed Equity Shares

| Particulars | Details |

|---|---|

| Holding Period | More than 12 months = Long-Term Capital Asset |

| Long-Term Capital Gain Tax Rate | Gains up to ₹1.25 lakh exempt; gains exceeding ₹1.25 lakh taxable at 12.5% |

| Short-Term Capital Gain Tax Rate | 20% |

Example: If you earn INR 2 lakh, a long-term capital gain from listed shares of INR 1.25 lakh is exempt, and INR 75,000 is taxable at 12.5%.

Listed Equity-Oriented Mutual Funds

| Particulars | Details |

|---|---|

| Holding Period | More than 12 months |

| Long-Term Capital Gain Tax Rate | Taxable at 12.5% on gains exceeding ₹1.25 lakh |

| Short-Term Capital Gain Tax Rate | 20% |

This includes most equity mutual funds where a substantial portion is invested in equity shares.

Listed Debentures

| Particulars | Details |

|---|---|

| Holding Period | More than 12 months |

| Long-Term Capital Gain Tax Rate | 12.5% without indexation benefit |

| Short-Term Capital Gain Tax Rate | normal tax slab rates |

Listed Shares and Equity Mutual Funds

- Long-Term Capital Gain exceeding INR 1.25 lakh – taxable at 12.5%

- Short-Term Capital Gain – taxable at 20%

- The Finance Act has removed indexation benefits for many assets, making gains taxable at a flat rate.

Listed Preference Shares

| Particulars | Details |

|---|---|

| Holding Period | More than 12 months |

| Long-Term Capital Gain Tax Tax Rate | 12.5% without indexation |

| Short-Term Capital Gain Tax Rate | normal tax slab rates |

Debt Mutual Funds and Market-Linked Debentures

| Particulars | Details |

|---|---|

| Holding Period | More than 24 months |

| Long-Term Capital Gain Tax Rate | Acquired before 1 April 2023: 12.5% without indexation; acquired after 1 April 2023: gains taxable at slab rates |

| Short-Term Capital Gain Tax Rate | Taxed at normal tax slab rates |

These investments no longer enjoy the traditional long-term capital gain benefits available earlier.

Unlisted Shares

| Particulars | Details |

|---|---|

| Holding Period | More than 24 months |

| Long-Term Capital Gain Tax Rate | 12.5% without indexation |

| Short-Term Capital Gain Tax Rate | Taxed at slab rates |

Unlisted Shares

- Long-Term Capital Gain – taxable at 12.5%

- Short-Term Capital Gain – taxed at applicable slab rates

This category includes shares of private limited companies and startups.

Unlisted Debentures and Bonds

| Particulars | Details |

|---|---|

| Holding Period | More than 24 months |

| Long-Term Capital Gain Tax Rate | Not applicable in most cases |

| Short-Term Capital Gain Tax Rate | Taxed at slab rates irrespective of holding period |

Immovable Property

| Particulars | Details |

|---|---|

| Holding Period | More than 24 months |

| Long-Term Capital Gain Tax Rate | Property acquired on or after 23 July 2024: 12.5% without indexation. Property acquired before 23 July 2024: taxpayer may opt for 20% with indexation (subject to applicable provisions) or 12.5% without indexation where permitted. |

| Short-Term Capital Gain Tax Rate | normal tax slab rates |

Immovable Property

- Long-Term Capital Gain generally taxable at 12.5% (without indexation)

- Short-Term Capital Gain taxable according to slab rates

- Illustration : Suppose Salary Income is INR 11 lakh and Long-Term Capital Gain from shares: INR 2 lakh. Even though salary income may qualify for rebate, tax on long-term capital gain may still be payable.

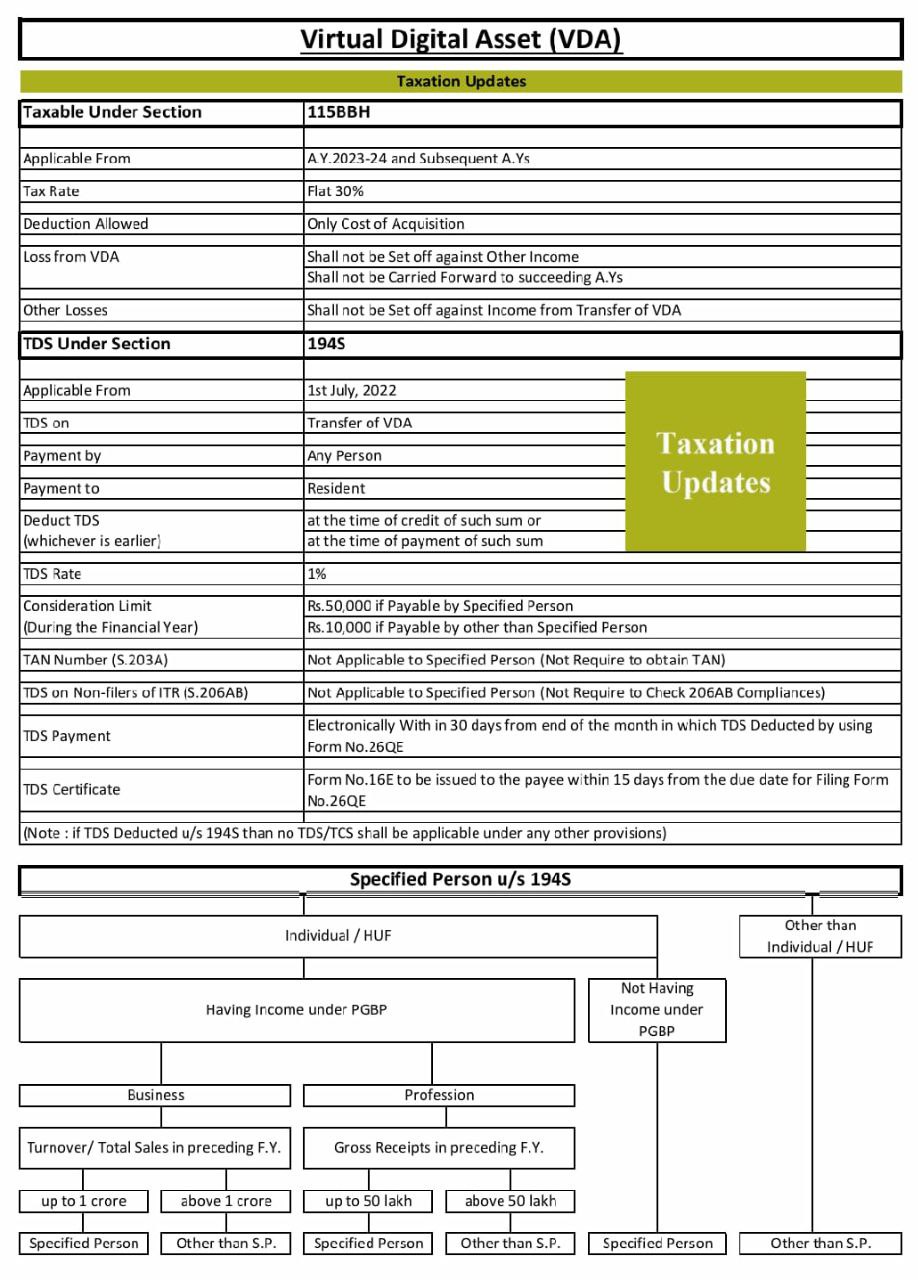

2. Virtual Digital Assets (Crypto Income):

Income from cryptocurrencies and other virtual digital assets continues to be taxed at a special rate. The tax rate is a flat 30% tax and Applicable cess and surcharge extra Key Restrictions: Only the cost of acquisition can generally be deducted. Losses cannot be set off against other income and basic exemption, and rebate benefits do not provide relief against this special-rate tax. Example: If a taxpayer earns Salary: INR 10 lakh and Crypto Profit: INR 1 lakh. Tax may still be payable on the crypto income despite salary income being within the rebate threshold.

3. Lottery, Horse Racing, and Similar Winnings:

Income from Lottery, Online gaming winnings, Horse racing, Crossword puzzles, Other specified speculative winnings is taxed at a flat 30% rate. Section 87A rebate generally does not eliminate this tax liability.

Cases Where Income Tax Return Filing May Still Be Mandatory

Many taxpayers believe that if taxable income is below the exemption limit, filing is not required. This is not always correct. ITR filing may become mandatory if a taxpayer has undertaken specified high-value transactions. Even if taxable income falls below the threshold, income tax return filing may still be compulsory under certain circumstances. ITR Filing May Still Be Mandatory Even Below Basic Exemption Limit, Examples include:

- High Electricity Consumption: If electricity expenditure exceeds the prescribed limit (commonly INR 1 lakh or more), filing requirements may arise. If electricity expenditure during the year is ₹1 lakh or more, filing may be required.

- Foreign Travel: Foreign travel expenditure above prescribed limits may trigger mandatory filing obligations. If expenditure on foreign travel exceeds ₹2 lakh, return filing may become compulsory.

- High-Value Transactions:

- Examples include Large bank deposits, Specified financial investments, Certain high-value credit card spending, and other prescribed transactions may require return filing even where income is otherwise not taxable.

Common Misconceptions related to Filing Income Tax Return

Myth 1: Income Below INR 12.75 Lakh Means No Income Tax Return

- Reality: Filing may still be necessary to claim a rebate or comply with reporting requirements.

Myth 2: Capital Gains Become Tax-Free

- Reality: Special-rate capital gains can continue to attract tax.

Myth 3: Crypto Income Gets Covered by Rebate

- Reality: VDA income is taxed separately at 30%.

Myth 4: Lottery Winnings Are Tax-Free Due to Rebate

- Reality: Lottery and similar winnings remain taxable at special rates

Key Takeaway

Zero tax liability up to INR 12.75 lakh applies primarily to regular salary income under the new tax regime so “income up to INR 12.75 lakh is tax-free” applies primarily to salary income under the new tax regime, subject to conditions and proper income tax return filing. Filing ITR is necessary to claim the rebate; Section 87A does not generally apply to income taxed at special rates. Tax may still be payable on capital gains, crypto (VDA) income, lottery winnings, and horse racing and similar speculative income. Before assuming that no tax is payable, taxpayers should carefully evaluate the nature of their income, not just the amount.

Simple Rule : Low income does not always mean zero tax. Special-rate incomes such as capital gains, crypto profits, and lottery winnings can still create tax liability, making Income Tax Return filing essential for AY 2026-27