Compulsory disclosure of Bank Balances in ITR‑4

Page Contents

Compulsory disclosure of taxpayer Bank Balances in ITR‑4

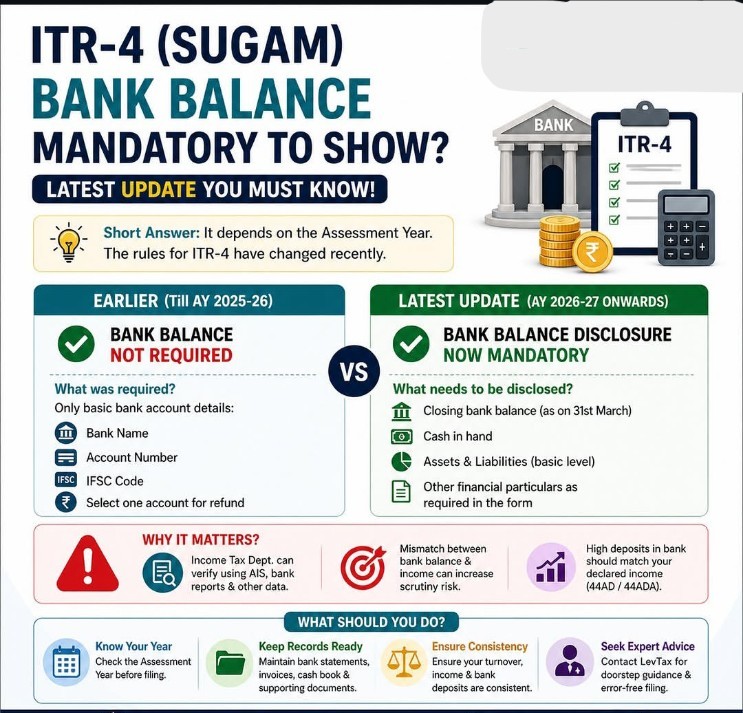

CBDT has introduced a significant compliance requirement via Notification No. 45/2026 dated 30 March 2026. Earlier ITR fillings were required; only bank account details (account number, IFSC, and bank name) were required, and bank balance disclosure was optional. However, now (AY 2026–27 onwards) bank balances must be mandatorily disclosed.

Major Update in ITR‑4 for AY 2026‑27 :

Compulsory disclosure of Bank Balances is now required under the

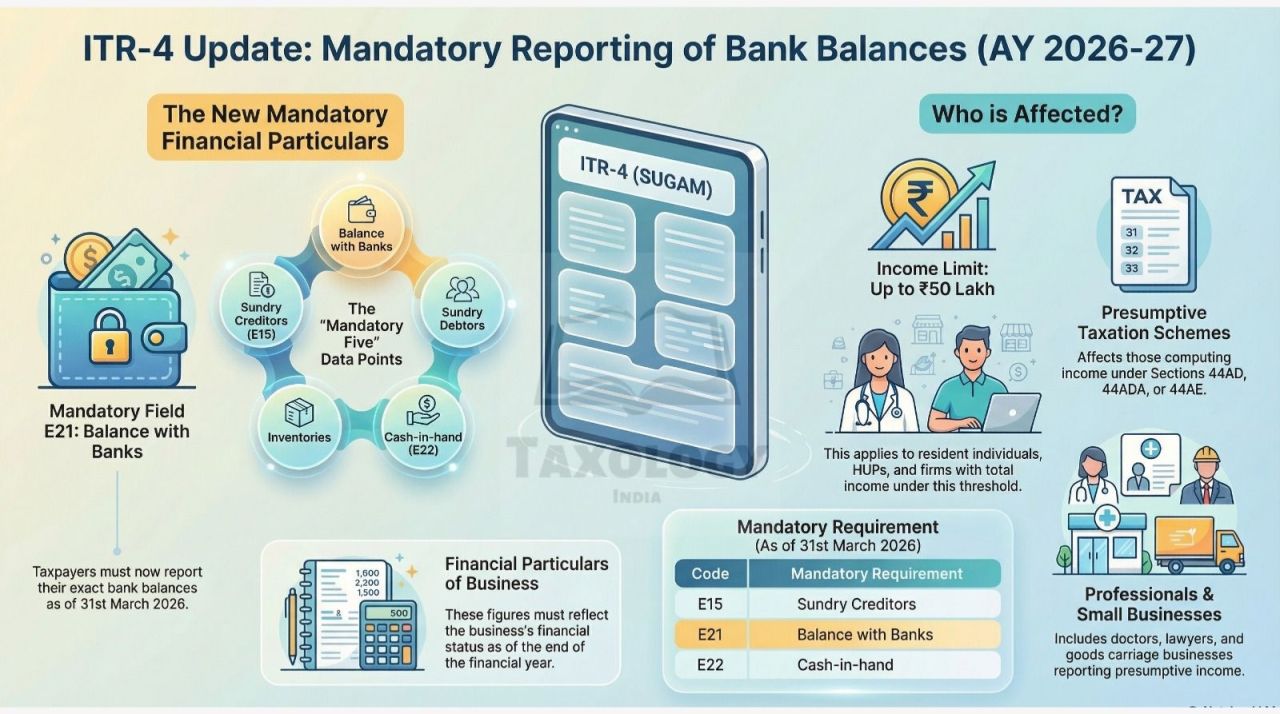

Income from Business or Profession (Schedule BP – Financial Particulars).

| Particulars | Earlier | Now |

|---|---|---|

| Bank account details | Mandatory | Mandatory in ITR‑4 |

| Bank balance disclosure | Optional | Mandatory in ITR‑4 |

Shift to Data‑Driven Compliance: Key Objective :

This change of compulsory disclosure of taxpayer bank balances in ITR‑4 covers small business owners, freelancers/consultants, professionals, and salaried persons with side income. The revamp is aimed at stronger data matching across AIS (Annual Information Statement), TIS (Taxpayer Information Summary), TDS returns, and GST data. Reducing income-reporting mismatches and also enabling automated scrutiny and notices. This is a shift from “self-declaration” → “system-verified reporting.”

Major Changes Across ITR Forms

- Expanded Income Disclosures: Detailed reporting for Long-Term Capital Gains (Sec 112A), F&O trading, intraday, speculative income, crypto transactions, and buyback-related capital losses.

- Mandatory reporting of Foreign Assets & overseas income

- The key objective behind the change is moving towards data-driven tax administration, enabling cross-verification with AIS / TIS and banking transactions, and improving transparency & risk profiling.

- Practical implications of mandatory disclosure of bank balances in ITR‑4 via Notification No. 45/2026 dated 30 March 2026 are increased data analytics by the department, cross-verification with AIS/TIS, and banking data. Likely scrutiny triggers a mismatch between turnover and bank credits and unexplained balances. It allows the department to correlate income vs bank balances and identify mismatches in presumptive income and unexplained deposits or large closing balances. So, indirect scrutiny risk increases if inconsistencies exist. Moreover, that impact on salaried individuals with side income must now track bank balances linked to side income and reconcile freelance receipts and digital platform earnings. Evaluate continued eligibility for the presumptive scheme.

High-Impact & key Changes in ITR‑1 & ITR‑2 and ITR‑3 & ITR‑4

- ITR‑1 (Simplified Return): Now allows up to 2 house properties and LTCG reporting up to INR 1.25 lakh (Sec 112A).

- ITR‑2 : Simplification and no need to split capital gains pre/post July 23, 2024. Expansion for that is detailed reporting of crypto holdings, foreign assets, and deductions.

- ITR‑3 (Business/Profession) : Enhanced reporting of F&O / intraday trades, speculative income, and Stronger Reconciliation with GST & AIS

- ITR‑4 (Presumptive Taxation)—Key Change: Mandatory disclosure of bank balances, earlier optional under Schedule BP, now compulsory reporting.

- Taxpayers are required to reconcile turnover vs bank credits and Bank balances vs declared income and manage multiple bank accounts. So the taxpayer needs proper bank reconciliation & documentation of sources of funds. Taxpayers must avoid data mismatches with AIS.

- For the professional focus areas Review bank balances vs presumptive income and identify red flags before filing. A professional is required to advise on whether the presumptive scheme still fits for the clients.

- These changes will affect small businesses (44AD), professionals (44ADA) and transporters (44AE) as well as freelancers & side-income earners.

- Additional Compliance Requirements: Linking of forms (e.g., Form 10BA) before filing, more granular reporting of deductions and Higher alignment with backend data systems