All about GST on event entry tickets

Page Contents

All about Goods and Services Tax on event entry tickets—recreational, cultural & sporting services

Meaning of Recreational, Cultural & Sporting Services (SAC 9996) under GST

A variety of leisure, entertainment, cultural, and sports-related services are included by Service Accounting Code 9996 under the Goods and Services Tax. These services are grouped together because they have to do with amusement, cultural enrichment, public entertainment, or watching or participating in sports. According to Goods and Services Tax sources, Service Accounting Code 9996 covers recreational activities, cultural events and performances, sporting events, and sports-related services.

- Recreational Services: According to Service Accounting Code 9996, recreational, cultural, and sporting services are any services that offer leisure or enjoyment (recreational), promote the arts, culture, or heritage (cultural), or entail playing sports or watching sports (sporting). These services are intended for enjoyment, relaxation, or entertainment. Examples (officially listed under Service Accounting Code 9996): Amusement parks & theme parks, water parks, joy rides, go‑karting, and casinos & betting (separately taxed). These services provide fun, enjoyment, and entertainment rather than cultural or sports value.

- Cultural Services: These services pertain to cultural performances, the arts, and history. Performing arts (music, dance, and theater); folk or classical art performances; entrance to museums, zoos, and national parks; and admission to cultural events and circuses are a few examples under Service Accounting Code 9996. When fees fall within specified ranges, many cultural services are free (e.g., classical arts performances up to INR 1.5 lakh).

Sports facilities, athletes, and sporting events are all included in the category of sporting services. Examples under Service Accounting Code 9996 include entrance to sporting events, services rendered to recognized sports organizations by coaches, referees, and athletes; running leisure and sports facilities; and organizing and promoting sporting events.

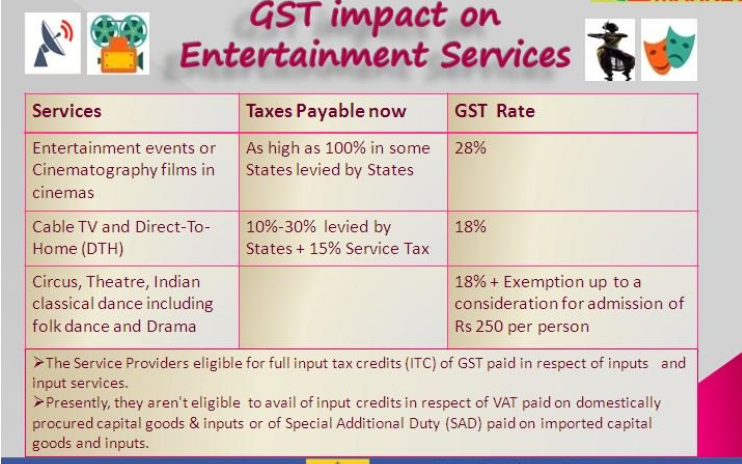

Full Input Tax Credit (ITC) Benefit for Service Providers:

Under Goods and Services Tax law, entertainment service providers can claim full input tax credit on goods purchased, input services used, and other operational costs taxed under Goods and Services Tax. this matters because it reduces the cascading tax effect, lowers the effective cost of operations, and allows more competitive pricing.

Goods and Services Tax has lowered the overall tax burden on entertainment services by replacing multiple, often very high state taxes with a uniform structure. Movie tickets, cable/DTH services, and many entertainment activities now face reduced and simplified taxation, along with ITC benefits for service providers.

Goods and Services Tax Rate for Event Entry Tickets—recreational, cultural & sporting services:

Sports Events

| Ticket Type | Goods and Services Tax Rate | |

|---|---|---|

| Recognized sporting events – Ticket ≤ INR 500 | Exempt (0%) | |

| Recognized sporting events – Ticket > INR 500 | 18% | |

| Premium sporting events (e.g., Premium sports events) | 40% (from 22‑09‑2025) |

Entertainment/Cultural/Amusement Events: For general entertainment entry tickets on entertainment/cultural/amusement events, which include concerts, shows, cultural events, fairs, and amusement events:

| Event Type | Goods and Services Tax Rate | Source |

|---|---|---|

| General entertainment & recreation services | 18% | (Classified under recreational, cultural & sporting services; Premium sports events excepted; SAC 9996) |

| Ticket Type | Goods and Services Tax Rate |

| Recognized sporting events – Ticket ≤ INR 500 | Exempt (0%) |

| Recognized sporting events – Ticket > INR 500 | 18% |

HSN / SAC Code for Event Entry Tickets :

Nearly all activities related to leisure, culture, and sports are covered by Service Accounting Code 9996. Your company probably comes within this category if it provides any enjoyable, artistic, or athletic activities—and using the appropriate Goods and Services Your compliance is kept tidy and stress-free by the tax rate. These categories help identify the applicable Goods and Services Tax rate (0%, 18%, or exceptionally high rates for particular events) and guarantee correct Goods and Services Tax classification. We employ SAC (Service Accounting Code) since event entry tickets constitute a service. General Admission to Events (Concerts, Shows, and Entertainment)

- Service Accounting Code : 9996 – Recreational, cultural, and sporting services (Covers admission to events, shows, entertainment, sports events, etc.)

- Reservation / Booking Charges for Event Tickets : If you charge booking / convenience / reservation fee, Service Accounting Code SAC: 998554 – Reservation services for event tickets, cinema halls, entertainment & recreational services

Most Useful for Practical Billing

| Scenario | GST Rate | Service Accounting Code |

|---|---|---|

| Entry to general events (concert, show, entertainment) | 18% | 9996 |

| Entry to recognized sports event ≤ INR 500 | 0% (Exempt) | 9996 |

| Entry to recognized sports event > INR 500 | 18% | 9996 |

| Premium sports events (IPL etc.) | 40% | 9996 |

| Ticket reservation / convenience fee | 18% | 998554 |

What is NOT considered a premium sports event?

Events like international cricket matches (non-premium sports events), the Indian Super League, Pro Kabaddi, other professional sports leagues, and recognized sports events continue to be subject to the 18% GST slab unless ticket prices are less than INR 500, in which case they are exempt.

What is considered a premium sports event?

Events are considered premium (40% Goods and Services Tax) under the most recent Goods and Services Tax regulations. Events like Indian Premier League games (which are specifically listed) and other high-profile commercial sporting events that the government designates as luxury-category entertainment fall under this category. These events fall under the same 40% tax category as casinos, betting, gambling, lotteries, and online gaming.

Premium sporting events provide substantial commercial revenue and great entertainment value, according to the Goods and Services Tax Council. They are regarded as luxury entertainment rather than necessary cultural or athletic promotion initiatives. They are taxed similarly to other high-value entertainment categories in order to preserve tax neutrality.

- Premium Sports Event = High-value, commercial entertainment + Government-designated luxury category → Goods and Services Tax Rate @ 40%

- Regular Recognized Sporting Event = Non-commercial / sports‑promotion event → Goods and Services Tax tax @ 18% or 0%