Income Tax Deductions while filling ITR in India

Page Contents

Income Tax Deductions Sections 80C to 80U in India for Tax Saving:

The most comprehensive guide for all income tax deductions covered in Chapter VI A of income tax for fiscal year 2020-21, from section 80C to section 80U. (AY 2021-22).

Income Tax Deductions in India

| Sections | Income Tax Deduction for FY 202021 | Who can Invest? | Limit for FY 2020-21 |

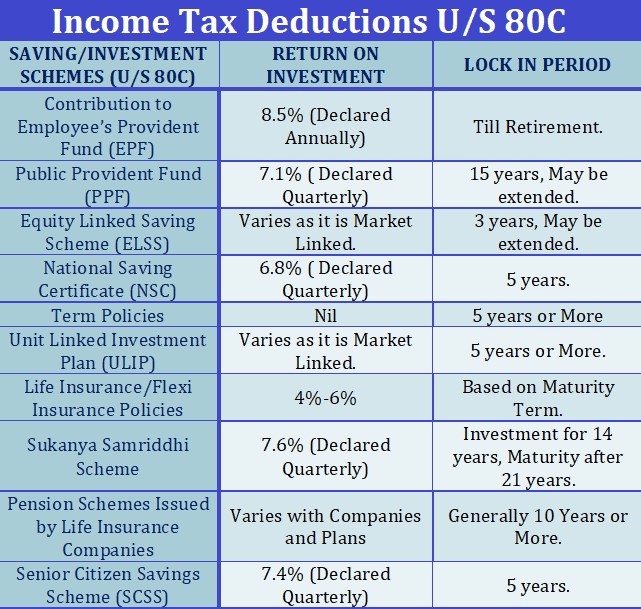

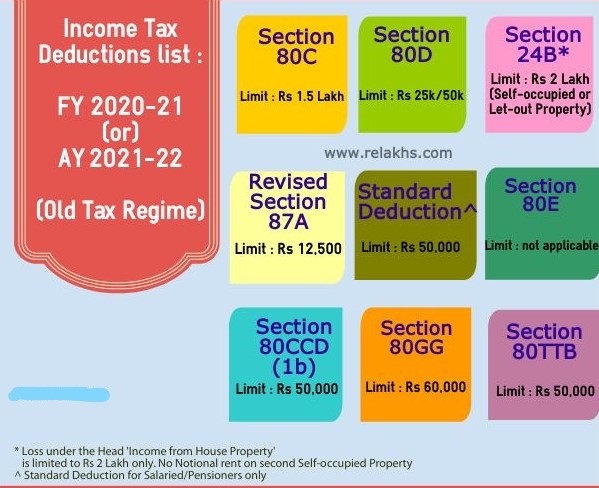

| Section 80C | Investing into very common and popular investment options like LIC, PPF, Sukanya Samriddhi Account, Mutual Funds, FD etc | Individual Or HUF |

Upto Rs 1,50,000 |

| Section 80CCC | Investment in Pension Funds | Individuals | |

| Section 80CCD (1) | Atal Pension Yojana and National Pension Scheme Contribution | Individuals | |

| Section 80CCD(1B) | Atal Pension Yojana and National Pension SchemeContribution | Individuals | Upto Rs 50,000 |

| Section 80CCD(2) | National Pension SchemeContribution by Employer | Individuals | Amount Contributed or 14% of Basic Salary + Dearness Allowance (in case the employer is CG) 10% of Basic Salary+ Dearness Allowance(in case of any other employer) – Whichever is lower |

| Section 80D | Medical Insurance Premium and Medical Expenditure | Individual Or HUF |

Upto Rs 1,00,000 |

| Section 80DD | Medical Treatment of a Dependent with Disability | Individual Or HUF |

Normal Disability: Rs 75000/- Severe Disability: Rs 125000/- |

| Section 80DDB | Specified Diseases | Individual Or HUF |

Senior Citizens: Upto Rs 1,00,000 Others: Upto Rs 40,000 |

| Section 80E | Interest paid on Loan taken for Higher Education | Individual | 100% of the interest paid upto 8 assessment years |

| Section 80EE | Interest paid on Housing Loan | Individual | Upto Rs 50,000 subject to some conditions |

| Section 80EEA | Interest paid on Housing Loan | Individual | Upto Rs 1,50,000/- subject to some conditions |

| Section 80EEB | Interest paid on Electric Vehicle Loan | Individual | Upto Rs 1,50,000 subject to some conditions |

| Section 80G | Donation to Charitable Institutions | All Assessee (Individual, HUF, Company etc) | 100% or 50% of the Donated amount or Qualifying limit, Allowed donation in cash upto Rs.2000/- |

| Section 80GG | Income Tax Deduction for House Rent Paid | Individual | Rs.60,000/- 25% of Total Income Rent paid – 10% of Total Income – whichever is lower |

| Section 80GGA | Donation to Scientific Research & Rural Development | All assessees except those who have an income (or loss) from a business and/or a profession | 100% of the amount donated. Allowed donation in cash upto Rs.10,000/- |

| Section 80GGB | Contribution to Political Parties | Companies | 100% of the amount contributed No deduction available for contribution made in cash |

| Section 80GGC | Individuals on contribution to Political Parties | Individual HUF AOP BOI Firm |

100% of the amount contributed. No deduction available for contribution made in cash |

| Section 80IA | Profits and Gains from Industrial Undertakings engaged in infrastructure development, etc. | Industrial Undertakings engaged in specified businesses | 100% of the profit for 10 consecutive years out of 15 years beginning from year of commencement |

| Section 80IAB | Profits and Gains to SEZ Developers | SEZ Developers | 100% of the profit for 10 consecutive years out of 15 years beginning from year in which SEZ has been notified by CG |

| Section 80IAC | Eligible startups | Company or LLP engaged in eligible business subject to some conditions | 100% of the profit for 3 consecutive years out of 7 years beginning from the year of commencement |

| Section 80IB | Profits and Gains from certain Industrial Undertakings other than infrastructure development undertakings | Specified Industrial Undertakings | 25%, 30% or 100% of the profit for such periods as may be specified subject to certain conditions |

| Section 80IBA | Profits from Housing Projects | Individual HUF AOP BOI Company Firm Any other person engaged in the business of Housing Projects as may be specified |

100% of the profit |

| Section 80IC | Certain Undertakings in Special category States | Certain Industrial Undertakings | Sikkim – 100% of profit for 10 years Himachal Pradesh/ Uttaranchal 100% of the profit (For fIncome tax Dept. t 5 years) 25%(For next 5 years), (30% in case of Companies) North Eastern States – 100% of the profit for 10 years |

| Section 80ID | Profits and Gains of Hotels/Convention Centres in specified area | Hotel or Convention Centre | 100% of the profit for 5 consecutive years beginning from the year of operation |

| Section 80IE | Certain Undertakings in North Eastern States | Undertakings engaged in manufacture/ provision of specified goods/ services or undertake substantial expansion, in North Eastern States | 100% of the profit for 10 consecutive years beginning from the year of commencement or completion of expansion, as may be applicable |

| Section 80JJA | Profits and Gains of Specified Business | Specified Business | 100% of the profit for 5 consecutive years beginning from the year of commencement |

| Section 80JJAA | Employment of New Employees | Employer who was subject to tax audit u/s 44AB | 30% of additional employee cost for 3 years including the year in which employment is provided |

| Section 80LA | Certain Income of Offshore Banking Units in SEZ and IFSC | Offshore Banking Units in SEZ or Unit of IFSC | Offshore Banking Unit – 100% of the income (For 5 consecutive years 50% of the income (For next 5 years) IFSC – 100% of the income for 10 consecutive years out of 15 years beginning from the year in which permission is obtained |

| Section 80PA | Certain income of Producer Companies | Producer Companies engaged in eligible business | 100% of the profit |

| Section 80RRB | Royalty on Patents | Individuals (Indian citizen or foreign citizen being resident in India) | Rs.3,00,000/- Or Specified Income – whichever is lower |

| Section 80QQB | Royalty Income of Authors | Individuals (Indian citizen or foreign citizen being resident in India) | Rs.3,00,000/- Or Specified Income – whichever is lower |

| Section 80TTA | Interest earned on Savings Accounts | Individual Or HUF (except senior citizen) |

Upto Rs 10,000/- |

| Section 80TTB | Interest Income earned on deposits(Savings/ FDs) | Individual (60 yrs or above) | Upto Rs 50,000/- |

| Section 80U | Disabled Individuals | Individuals | Normal Disability: Rs. 75,000/- Severe Disability: Rs. 1,25,000/- |

Difference between Section 80TTB and Section 80TTA

| Particulars | Section 80TTB | Section 80TTA |

| Specified income | Interest on all kinds of deposits | Interest on savings A/c only |

| Applicability | Applicable to senior citizens | Applicable to individuals and HUF except for senior citizens |

| Limit of deduction | Upto Rs 50k | Upto Rs 10k |

Learn how the medical bills of your elderly parents can help you save money on your taxes:

Learn how the medical bills of your elderly parents can help you save money on your taxes.

Maintaining good health is undoubtedly the season’s theme. With the second wave of COVID underway, health insurance appears to be an inevitable requirement that also provides tax benefits under Section 80D.

The catch is that health insurance premiums for senior citizens are either prohibitively expensive or unavailable, particularly for those with pre-existing conditions. Don’t panic — did you know that even your elderly parents’ medical expenditures can help you save money on taxes?

Let’s take a look at how this works.

- Medical expenses incurred by senior citizens aged 60 and up are eligible.

- This deduction may be claimed by the individual (senior citizens) or by the family (parents, spouse, or dependent children).

- The person claiming the deduction is not covered by any health insurance.

- All medical expenses, from consultation fees to medications, or the purchase of devices such as hearing aids, are allowable. A proof of identification will be required.

- Most importantly, cash payments are not permitted.

- Medical expenses incurred by senior citizens aged 60 and up are eligible.

- This deduction may be claimed by the individual (senior citizens) or by the family (parents, spouse, or dependent children).

- The person claiming the deduction is not covered by any health insurance.

- All medical expenses, from consultation fees to medications, or the purchase of devices such as hearing aids, are allowable. A proof of identification will be required.

- Most importantly, cash payments are not permitted.

- The medical expense limit remains the same as the one allowed for health insurance, which is Rs. 50000 per year for parents and Rs. 50000 per year separately for self, spouse, or dependent children ( if senior citizen).

This year, because there are many cases of people incurring expenses for Covid-related treatments, make sure you take advantage of this benefit to save money on taxes.

Major Change in income tax rules for FY 2021-22

Major Changes to the FY 2021-22 income tax rules.: In general, in the February budget, the government makes changes to the tax rules. These changes take effect in April from the next financial year.

Take note and plan your taxes more effectively.

- Choosing a tax regime: Taxpayers had the option of choosing between two tax systems in last year’s budget. This is the second year in which you must make a decision. What exactly is the distinction between the two? The old regime had various exemptions but had higher tax rate slabs; the new regime has lower tax rate slabs but no specific deductions or exemptions. Choose the correct slab to get the most out of your investment.

- Revised tax returns or late returns file less time to: Every year, tax returns are due by July 31st. You could file it until the 31st of March of the Assessment year and pay a small late fee, or you could revise your return. The period for revising forms or filing late taxes has shrunk by three months this financial year. You only have until December 31st to complete your task.

- The income of the dividend will be shown on the ITR: Dividend distribution tax was levied on companies till FY 2019-20, and dividend income from domestic companies was free up to Rs. 10 lakh, however beginning FY 2020-21, dividends will be completely taxable at the slab rate, with no dividend distribution tax to pay. So, check your Form 26AS for TDS against dividend income, reconcile it with the credit of dividend amount in your account, and pay up tax according to your slab.

- Take advantage of pre-filled ITR forms: To make tax filing easier and more transparent, your ITR forms will be pre-filled with information about capital gains from listed securities, mutual funds, dividend income, interest from banks and post offices, salary income, and so on.

- Interest on voluntary contributions to the EPF that exceed a certain threshold is taxed: Until F.Y.2020-21, interest generated on provident funds was completely tax-free. The FM announced in Budget 2021 that interest income on voluntary contributions to EPF exceeding Rs 2.5 lakh would be taxed. However, if your company does not contribute to EPF, this ceiling was raised to Rs 5 lakhs. As a result, if your EPF/VPF deposit exceeds the specified maximum, interest income will now be taxable. This will be implemented in April of this year. As a result, make sure to budget for your contributions and taxes.

- ULIPs are subject to a tax: If the premium paid for a ULIP policy did not exceed 10% of the total assured, the maturity proceeds were tax-free. But everything changed with the last budget! This provision will apply only if the total premium for all ULIPs you have purchased in a year does not exceed Rs 2.5 lakhs. This rule applies to ULIPs purchased after February 1, 2021.

- In some cases, senior citizens over the age of 75 are exempt from filing an ITR: If a senior citizen’s only source of income is a pension and bank interest, they are exempt from filing IT returns if certain conditions are met.

Date: 20 May, 2021: The Department of income tax extends the dates following

- Income Tax Return Date from 31 July 2021 extended to 30September21 and further extended till 31st dec 2021.

- The deadline for submitting Form-16 has been extended back to 15th July, 21 from 15th June, 21.

- Now, instead of 31 May 21, the TDS return for Q4 may be filed by 30 June 21.

Popular Blogs:

- How to file a return of TDS online

- New revise TDS/TCS due date for filing Return and Payment for the year 2020

- key features of TCS on goods sale section-206c

For query or help, contact: singh@carajput.com or call at 9555555480