Summary of TDS Rate Chart in Budget 2024 w.e.f. Oct 1, 2024

Page Contents

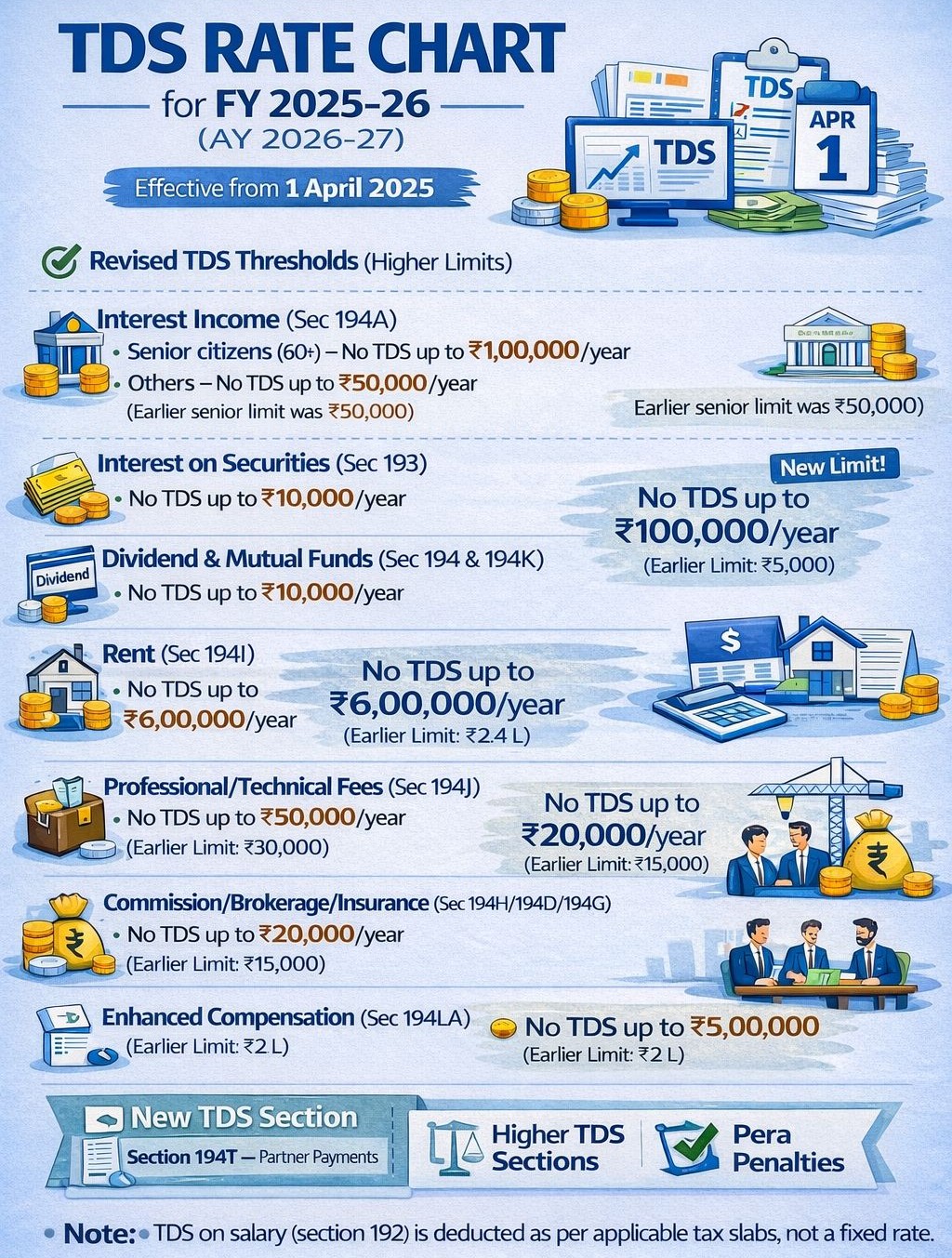

TDS Rate Chart Summary—FY 2025–26 (AY 2026–27)

Effective from 1 April 2025, the chart shows revised higher TDS thresholds, meaning no TDS will be deducted until the income crosses these new limits.

Interest Income — Section 194A

Senior Citizens (60+) : No TDS up to INR 1,00,000/year (Earlier limit: ₹50,000)

Others : No TDS up to INR 50,000/year

Interest on Securities—Section 193

- No TDS up to INR 10,000/year

Dividend & Mutual Funds — Sections 194 & 194K

- No TDS up to INR 10,000/year

Winnings from Online Games — Section 194B/194BA (Updated)

New Threshold: No TDS up to INR 1,00,000/year (Earlier limit: INR 5,000)

Rent — Section 194I

Plant & Machinery (P&M): No TDS up to INR 6,00,000/year (Earlier: INR 2,40,000)

Land, Building, Furniture, Fittings: No TDS up to INR 6,00,000/year

Professional / Technical Fees — Section 194J

- No TDS up to INR 50,000/year (Earlier: INR 30,000)

Technical/Managerial/Consultancy Contracts (10% TDS category):

- No TDS up to INR 20,00,000/year (Earlier: INR 1,50,000)

Commission / Brokerage / Insurance — Sections 194H, 194D, 194G

- No TDS up to INR 20,000/year (Earlier: INR 15,000)

Enhanced Compensation — Section 194LA

- No TDS up to INR 5,00,000 (Earlier: INR 2,00,000)

New TDS Section Introduced- Section 194T — Partner Payments

(Details not shown on chart; applies to certain payments made to partners by firms)

TDS on salary (Section 192) continues to be deducted as per tax slabs, not at a fixed rate.

Tax Deducted at Source rates chart proposed in Union Budget 2024 have been approved in the Finance Bill:

Budget 2024 introduced several tax reforms & Income Tax amendments, which were ratified in the Finance Bill and became effective from Oct 1, 2024. Some of the key changes include revised TDS rates and adjustments to other tax rules, impacting a variety of sectors & Payment categories. The above changes are significant for individuals, businesses, and e-commerce operators, impacting rent payments, commissions, bond earnings, share buybacks, and more. It’s important to stay updated and comply with these revised regulations. Below is a Summary of these changes in TDS rate Chart proposed in Budget 2024 w.e.f. Oct 1, 2024

-

Revised Tax Deducted at Source Rates (Effective from October 1, 2024)

-

- Section 194DA: Tax Deducted at Source on payments related to life insurance policies has been reduced from 5% to 2%.

- Section 194H: Tax Deducted at Source on commissions paid has been reduced from 5% to 2%.

- Section 194-IB: Tax Deducted at Source on rent payments by individuals or HUFs (Hindu Undivided Families) has been reduced from 5% to 2%.

- Section 194M: Tax Deducted at Source on certain payments by individuals or HUFs has been reduced from 5% to 2%.

- Section 194G: Tax Deducted at Source on commission for the sale of lottery tickets has been reduced from 5% to 2%.

- Section 194-O: Tax Deducted at Source for e-commerce operators on payments made to e-commerce participants has been significantly reduced from 1% to 0.1%.

- Section 194F: Tax Deducted at Source on payments from the repurchase of units by Mutual Funds or Unit Trust of India has been omitted.

-

Floating Rate Bonds Tax Deducted at Source

-

- From October 1, 2024, 10% Tax Deducted at Source will be applied to interest earned from specified central and state government bonds, including floating rate bonds.

- A threshold limit of Rs 10,000 applies, meaning no Tax Deducted at Source will be deducted if annual income from such bonds is less than Rs 10,000.

- Buyback of Shares

-

- As of October 1, 2024, income from share buybacks will be taxed at the shareholder level, similar to dividends. The shareholder’s acquisition cost of the shares will now be considered when calculating capital gains or losses, likely resulting in a higher tax burden for investors.

- Increased Securities Transaction Tax

-

- Futures transactions will now have an Securities Transaction Tax of 0.02%, and Options transactions will have an Securities Transaction Tax of 0.1%, effective from October 1, 2024.

- Income receipts from share buybacks will also be taxed in the hands of the beneficiaries.

- Tax Deducted at Source on Sale of Immovable Property (Section 194-IA)

-

- Tax Deducted at Source of 1% will be deducted on transactions involving the sale of immovable property exceeding INR 50 lakh. This applies collectively in cases where there are multiple buyers or sellers, ensuring the threshold limit considers the total transaction amount.

- This rule is effective from October 1, 2024.

TDS threshold rationalization w.e.f. April 1, 2025- Budget 2025

Taxpayers may permanently lose TDS credits. 6 Year time limit for Revising TDS return

The amendment in the Budget 2024 introducing a six-year time limit for revising TDS returns has significant implications. The cut-off date of March 31, 2025, for financial years 2007-08 to 2018-19, is crucial for taxpayers and deductors. If corrections are not made in time, taxpayers may permanently lose TDS credits, leading to additional tax liability and potential double taxation. For affected taxpayers, it’s advisable to:

- Verify Form 26AS and AIS to check for missing or incorrect TDS credits.

- Contact deductors to ensure any errors in TDS filings are corrected before the deadline.

- Follow up on pending corrections with the deductor or file grievances with the TRACES portal if needed.

Since there was previously no time limit, some taxpayers might have relied on future corrections to claim TDS credits. The new restriction makes proactive action essential.