Savings Account Rules for Transactions to Avoid Tax Scrutiny

Page Contents

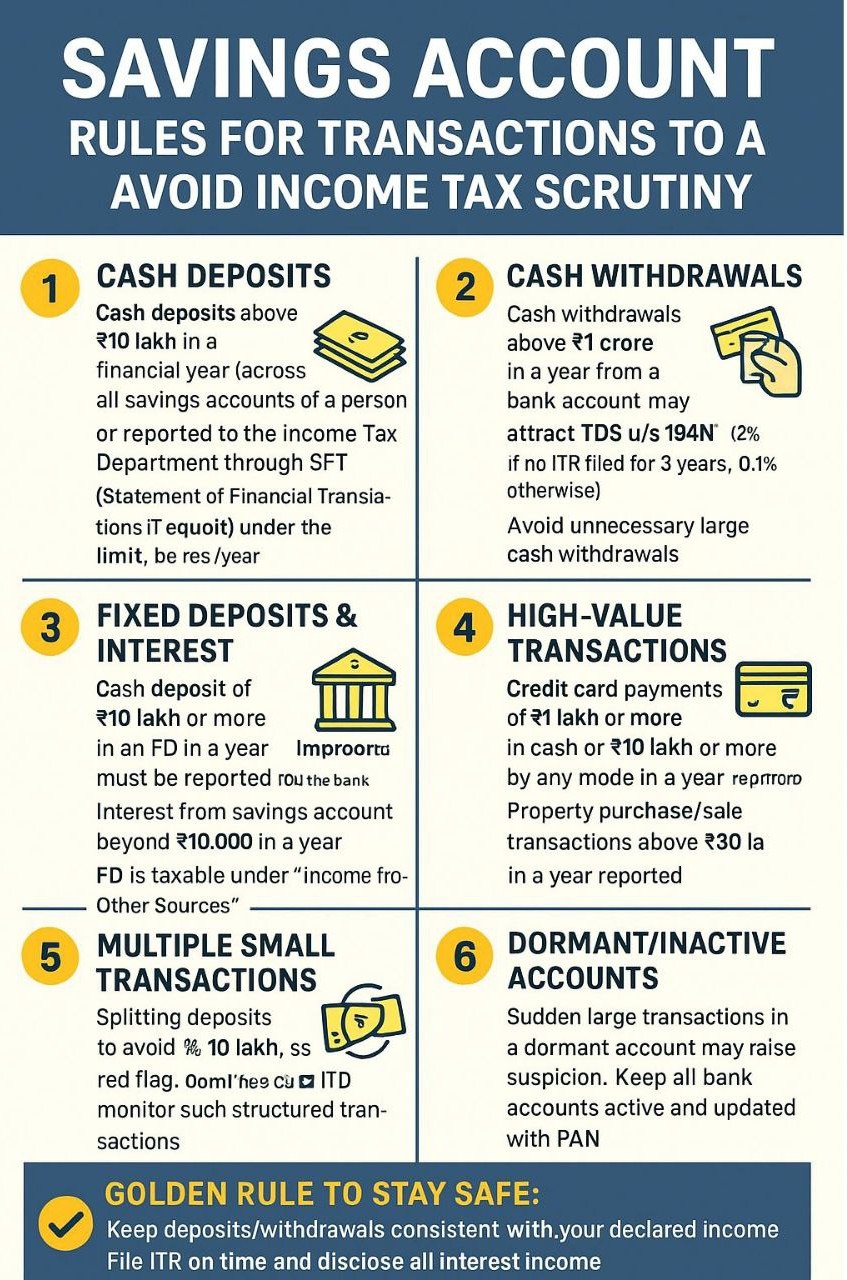

Savings Account – Rules for Transactions to Avoid Income Tax Scrutiny

The Income Tax Department monitors high-value transactions through banks’ Annual Information Statement (AIS) & SFT reporting. Certain activities in savings accounts can attract scrutiny if they appear unusual or exceed prescribed limits. Keep your financial transactions transparent, documented, and consistent with your declared income. If you anticipate high-value transactions, plan them properly and ensure correct disclosure in your Income Tax Return.

Best Practices & Rules to Follow – Tax Dept monitors high-value transactions

- Cash Deposits : Cash deposits above INR 10 lakh in aggregate in a financial year in savings accounts are reported to the IT Department. For current accounts, the threshold is INR 50 lakh. Avoid splitting large cash deposits across different accounts – banks still report PAN-linked totals.

- Cash Withdrawals : Cash withdrawals above INR 1 crore per year (INR 20 lakh in some cases without PAN/Aadhaar) attract reporting and may be subject to TDS under Section 194N. So in case Withdrawals > INR 1 crore/year are reported. If PAN/Aadhaar not provided, threshold drops to INR 20 lakh/year. May attract TDS under Section 194N.

- PAN Requirement : Any cash deposit or withdrawal exceeding INR 50,000 in a day requires furnishing PAN. Always quote PAN correctly to avoid mismatches.

- Large Fund Transfers : Frequent or unexplained large RTGS/NEFT/IMPS/UPI transfers to/from savings accounts may raise suspicion if not supported by income proofs or ITR filings.

- Fixed Deposits : Aggregate FD deposits of INR 10 lakh or more in a financial year are reported by banks. Interest earned is taxable and must be disclosed in ITR, even if TDS is deducted.

- Credit Card Payments : Credit card bill payments of INR 1 lakh or more in cash, or INR 10 lakh or more in total (non-cash) in a year are reported. Ensure consistency with declared income.

- Investments & Securities : Purchase of mutual funds, bonds, shares above INR 10 lakh in a year is reported. Source of funds must align with declared income.

- Property-Related Payments : Any transaction of INR 30 lakh or more towards purchase of immovable property is reported. So Any payment > INR 30 lakh for property purchase is reported.

- Multiple Small Transactions : Frequent small deposits/withdrawals structured to avoid thresholds (“smurfing”) can also attract scrutiny. Frequent small transactions to avoid thresholds can still trigger scrutiny.

- Consistency with ITR : Ensure that savings account transactions (credits/debits) match with your ITR disclosures, especially for freelancers, professionals, and small business owners. Maintain documentary evidence (invoices, salary slips, investment proofs) for large inflows.

Red Flags On Monitors high-value transactions That May Trigger Scrutiny

- Large cash deposits without matching declared income.

- High-value transactions inconsistent with your ITR.

- Multiple accounts used to spread deposits/withdrawals.

- Frequent cash dealings instead of digital transactions.

In summary Taxpayer must maintain large cash deposits without matching income, High-value transactions inconsistent with ITR, Use of multiple accounts to spread transactions, Preference for cash over digital payments.

Basic Savings Bank Deposit (BSBD) accounts

New RBI rule effective from 1 April 2026 regarding Basic Savings Bank Deposit (BSBD) accounts. (Effective Date: 1 April 2026). Highlights of the New RBI Rule.

- No Cash Deposit Fees : BSBD account holders will not be charged for cash deposits at branches, ATMs, or business correspondents.

- Digital Banking Access : No restrictions on mobile and internet banking. Banks must provide these services without imposing limits.

- No Account Access Restrictions : Banks cannot restrict account access based on income level or customer profile.

- Objective of Changes

- Improve convenience

- Reduce banking costs

- Ensure financial inclusion