Overview of the Internal Audit Iceberg Concept

Page Contents

Overview of the Internal Audit Iceberg Concept

Apache Iceberg introduces a powerful feature called Integrated Audits, which allows organizations to validate data before publishing it to production, ensuring high data quality and trustworthiness.

- Internal Audit Iceberg includes a high-performance table format for large-scale analytics. Supports multiple engines like Spark, Trino, Flink, Presto, Hive. & Enables safe concurrent access and SQL-like simplicity for big data.

- Iceberg’s internal audit features allow Scalable validation across large data warehouses, Flexible integration with existing pipelines, Improved trust and reliability in data products

- Why Internal Audits Matter: Internal audits enhance internal controls, which can Detects & prevents errors or fraud. The internal audit ensures compliance—keeping your business aligned with laws & regulations. Internal audit services will improve efficiency that streamlines operations for better productivity & performance.

What They Don’t See – The Hidden Audit Effort

Control Walkthroughs, Evidence Gathering, Documentation Reviews

- Auditors meticulously trace processes, interview stakeholders, and collect supporting documentation.

- They validate control design and operational effectiveness often across multiple systems and departments.

- This includes reconciling inconsistencies, verifying transactions, and ensuring compliance with policies.

Data Analytics, Root-Cause Analysis, Risk Assessments

- Auditors use advanced analytics to detect anomalies, trends, and potential fraud.

- They perform root-cause analysis to go beyond surface-level symptoms and uncover systemic issues.

- Risk assessments help prioritize audit focus areas based on impact and likelihood often under tight deadlines.

Stakeholder Resistance, Ethical Dilemmas, Limited Resources

- Auditors must diplomatically manage resistance to findings and recommendations.

- They navigate ethical gray zones such as conflicts of interest, whistleblower concerns, or sensitive disclosures.

- Often, audits are conducted with limited staff, time, and tools, requiring strategic prioritization and multitasking.

Continuous Follow-Ups, Quality Assurance, Audit Committee Prep

- Follow-up audits ensure that corrective actions are implemented and sustained.

- Quality assurance reviews validate the integrity of audit work before final reporting.

- Preparing for audit committee meetings involves synthesizing findings, aligning with governance priorities, and anticipating tough questions.

The True Value of Internal Audit

- Internal audit is not just about finding faults it’s about building trust, strengthening governance, and enabling better decisions.

- Behind every audit report lies weeks of invisible effort, coordination, and professional judgment.

- Auditors act as guardians of integrity, helping organizations stay resilient, compliant, and forward-looking.

Above the Surface: What People See :

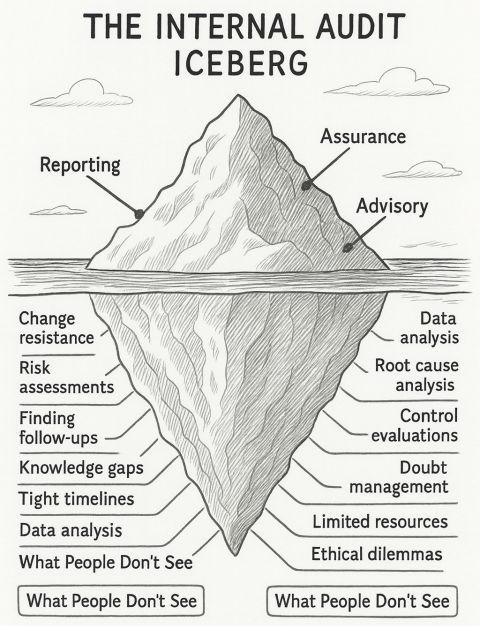

The Internal Audit Iceberg visually represents the visible and hidden dimensions of internal audit work. Most of internal audit’s true value and effort lie beneath the surface, unseen by most stakeholders. While the top of the iceberg (reports, assurance, and advisory work) represents visible deliverables, the vast base reflects the rigorous analysis, professional judgment, and ethical challenges auditors deal with daily. These are the visible deliverables that stakeholders typically associate with internal audit:

- Reporting : Formal audit reports summarizing findings, risks, and recommendations, Executive summaries and dashboards for senior management. & Compliance documentation and audit trails.

- Assurance : Independent evaluations of internal controls, risk management, and governance, Confirmation that processes are functioning as intended, Comfort to stakeholders that risks are being managed.

- Advisory : Strategic advice on process improvements, risk mitigation, and compliance. Participation in committees or working groups, Support during system implementations or organizational changes.

These are the most visible outputs of internal auditing reports, opinions, and advice that stakeholders and management typically recognize.

Below the Surface: What People Don’t See

This is the core effort that enables the visible outputs. It’s often unseen, but it’s where most of the value and complexity lies:

-

Change Resistance

- Overcoming organizational reluctance to adopt audit recommendations.

- Navigating organizational inertia and reluctance to adopt audit recommendations.

- Building trust and influencing change without authority.

-

Risk Assessments

- Evaluating and prioritizing risks to focus audit efforts.

- Identifying and prioritizing risks across departments and processes.

- Determining audit scope and focus areas based on risk exposure.

-

Finding Follow-Ups

- Ensuring issues raised are tracked and resolved.

- Tracking resolution of past audit findings.

- Ensuring accountability and closure of issues.

-

Knowledge Gaps

- Bridging skill and information deficiencies.

- Bridging gaps in technical, regulatory, or operational knowledge.

- Continuous learning and upskilling to stay relevant.

-

Tight Timelines

- Working under strict deadlines.

- Delivering quality audits under strict deadlines.

- Balancing thoroughness with efficiency.

-

Data Analysis

- Processing and interpreting large data sets.

- Extracting, cleaning, and interpreting large datasets.

- Using analytics to detect anomalies, trends, or fraud.

-

Root Cause Analysis

- Identifying underlying reasons for issues.

- Going beyond symptoms to uncover the true source of issues.

- Ensuring recommendations address systemic problems.

-

Control Evaluations

- Assessing the design and effectiveness of internal controls.

- Assessing the design and operational effectiveness of controls.

- Testing controls through walkthroughs, sampling, and automation.

-

Doubt Management

- Handling uncertainties in findings or evidence.

- Dealing with uncertainty in evidence, stakeholder responses, or audit scope.

- Exercising professional skepticism and judgment.

-

Limited Resources

- Managing constraints in manpower, tools, and time.

- Operating with constraints in budget, tools, and personnel.

- Prioritizing audits and optimizing resource allocation.

-

Ethical Dilemmas

- Navigating conflicts of interest or sensitive situations.

- Handling conflicts of interest, whistleblower cases, or sensitive findings.

- Upholding integrity and confidentiality under pressure.

- This is the deeper, often invisible effort that makes audit functions effective:

Benefits of Integrated Internal Audits

- No need to write data twice

- No test tables or schema sync issues

- Decouples ETL from validation logic

- Supports multiple audit tools

- Automated cleanup of failed data

The Impact of Internal Audit

- Trust: Audits build confidence in systems, processes, and data.

- Resilience: By identifying and mitigating risks, audits help organizations withstand shocks.

- Improvement: Audits drive continuous improvement through insights and recommendations.

- Decision Support: Audit findings inform strategic and operational decisions.

Why Internal Audit Iceberg Matters

This concept helps organizations, boards, and stakeholders understand why internal audit is not just a compliance exercise, but a strategic function that drives resilience, transparency, and long-term success.

| Above the Surface | Below the Surface |

|---|---|

| Reports, opinions, and recommendations | Risk assessments, data analytics, ethics, process improvements, and change management |

| What management sees | What actually ensures audit effectiveness |

| Tangible deliverables | Intangible value drivers |

Because true audit value lies not in what’s seen, but in what’s done quietly, diligently, and strategically beneath the surface. The iceberg metaphor helps stakeholders understand that audit value isn’t just in the report. it’s in the rigorous process that leads to it. Recognizing the hidden layers fosters appreciation, trust, and better collaboration between auditors and management.

Strengthen Your Business with Rajput Jain & Associates Internal Audit Solutions

A robust internal audit system is vital for business transparency, risk management, & operational efficiency. Without proper audits, organizations risk facing financial discrepancies, compliance issues, & inefficiencies that can impact long-term growth. At Rajput Jain & Associates, we deliver comprehensive internal audit solutions designed to strengthen internal controls, enhance performance, & minimize business risks. following are the Key Benefits of internal Audit of company :

- Aids in business risk mitigation

- Facilitates performance evaluation

- Strengthens internal control mechanisms

- Enhances operational effectiveness & efficiency

- Ensures accuracy & reliability of financial reporting

- Boosts stakeholder confidence

- Promotes legal & regulatory compliance

- Prevents fraud & irregularities

With Rajput Jain & Associates, Clint’s business gains improved financial reliability, minimized risk exposure, & enhanced stakeholder trust paving the way for sustainable growth & operational excellence. Our Areas of expertise are accounts & finance, statutory compliances, purchase & inventory audit, CIRP audit, sales & marketing audit; internal control systems audit, process & system audits, and special purpose audits.

you may also review other blogs about the internal audit.