ITR-2 vs ITR-3 Inconsistencies: Foreign Listed Share Reporting & FA

Page Contents

Inconsistency in ITR Forms – Intentional or Merely an Oversight?

The issues highlighted are genuine practical concerns arising from the current design of the ITR utilities and instructions. Based on the presently available ITR forms and the underlying legal provisions, the following analysis may be relevant.

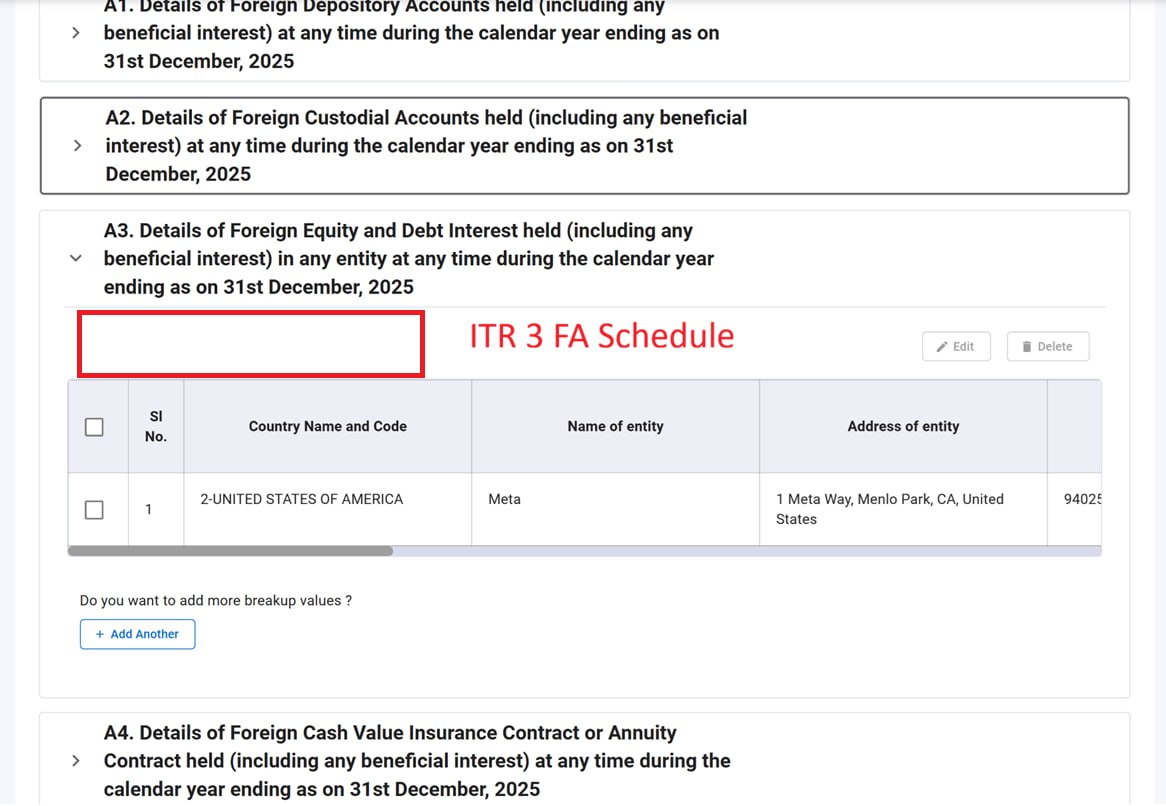

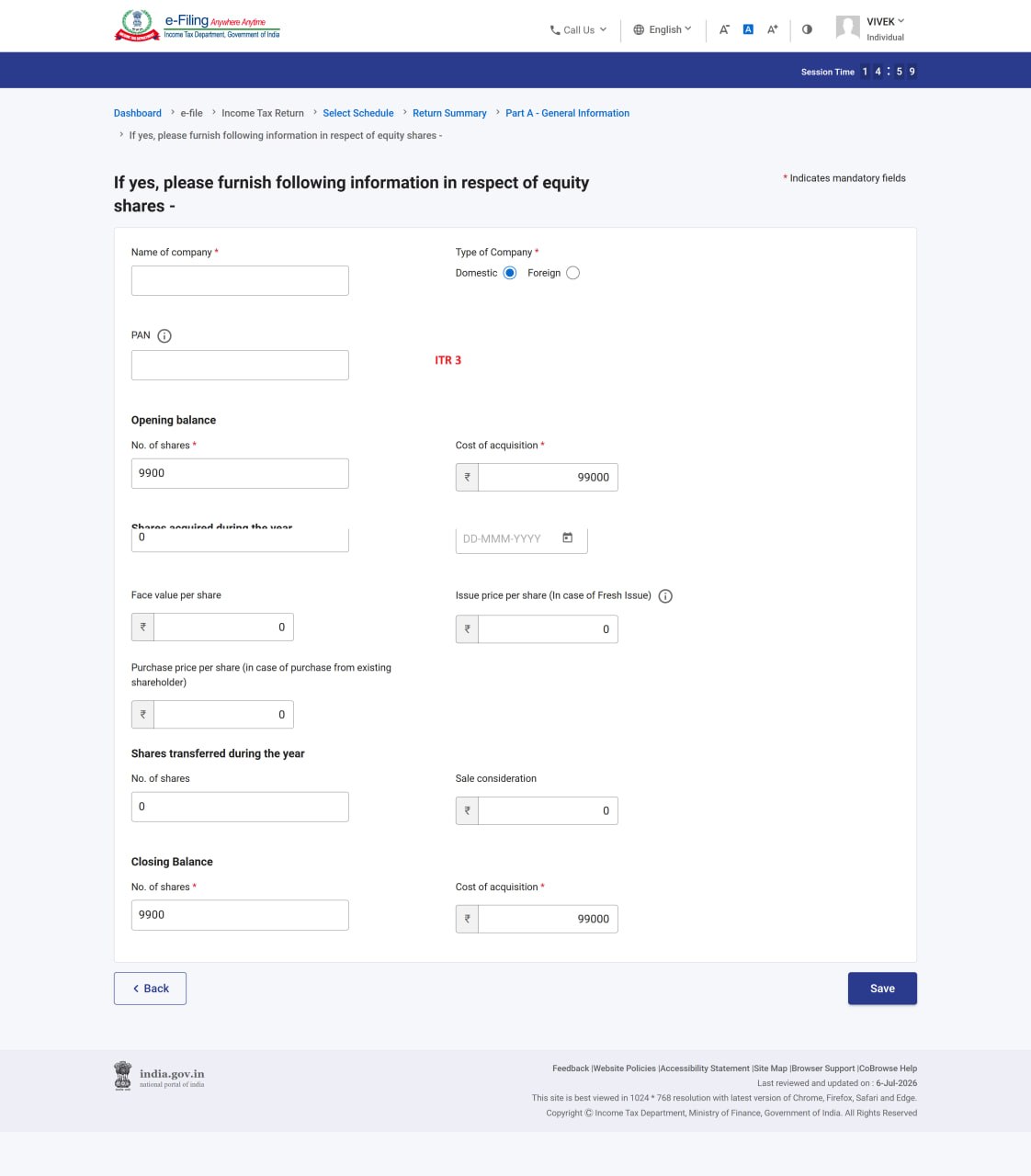

Unlisted Equity Share Schedule – ITR-2 vs ITR-3

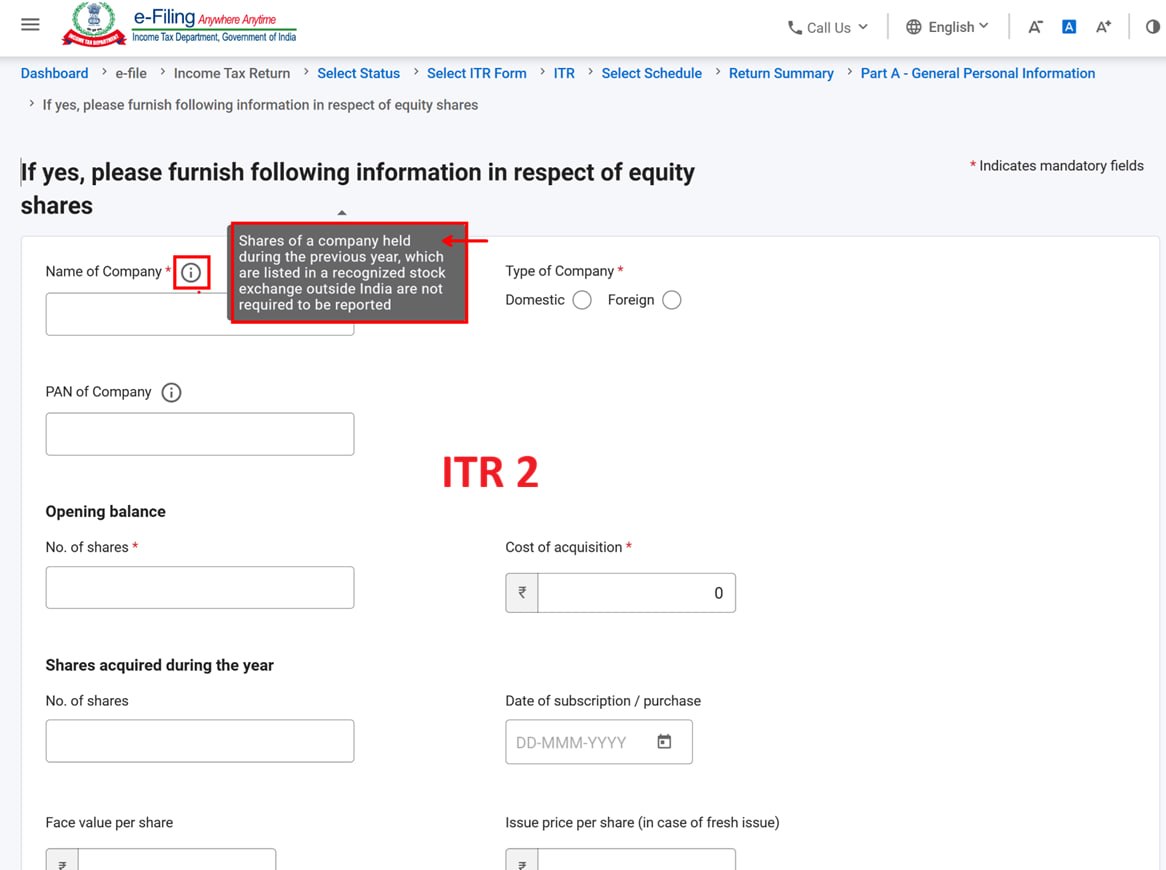

In ITR-2, the instructions specifically clarify that shares listed on a recognized foreign stock exchange are not required to be reported in the “Unlisted Equity Shares” schedule. However, a similar clarification does not presently appear in ITR-3.

From a legal and disclosure perspective, this distinction appears difficult to justify because:

- A share listed on NASDAQ, NYSE, LSE, or any recognized foreign stock exchange is fundamentally a listed security.

- The purpose of the Unlisted Equity Share schedule has historically been to capture holdings in companies whose shares are not publicly traded.

- Merely changing the ITR form (ITR-2 to ITR-3) should not alter the character of the asset.

Therefore, the more reasonable interpretation is that the omission in ITR-3 is likely a drafting or instruction gap rather than a substantive change in reporting requirements.

Taxpayers holding US-listed stocks and filing ITR-3 should continue to disclose such investments in the Foreign Asset (FA) Schedule wherever applicable, but there is a strong argument that they should not be treated as “unlisted equity shares” merely because the ITR-3 instructions lack the clarification available in ITR-2.

Foreign Asset (FA) Excel Upload – ITR-2 vs ITR-3

Another notable inconsistency is the utility functionality:

- ITR-2 Utility permits import/upload of foreign asset details through Excel.

- ITR-3 Utility currently lacks a corresponding import facility.

This difference creates compliance challenges because ITR-3 filers often have more complex reporting requirements than ITR-2 filers. Persons with foreign shares, ESOPs, foreign bank accounts, foreign pension plans, and overseas investments may need to manually enter large volumes of data. And the absence of an import facility increases the compliance burden and the risk of data-entry errors.

There appears to be no policy rationale for allowing Excel import in ITR-2 but denying the same convenience in ITR-3. Accordingly, this looks more like a utility limitation or implementation oversight than an intentional policy decision.

Two inconsistencies in ITR-2 vs ITR-3

The two inconsistencies indicate that the utilities may not yet be fully harmonized across forms. Until CBDT issues a clarification or releases an updated utility:

- US-listed and other foreign-listed shares should generally be regarded as listed securities and disclosed appropriately in the Foreign Asset Schedule.

- Taxpayers filing ITR-3 should carefully verify foreign asset disclosures because the absence of an Excel import facility increases the possibility of reporting errors.

- Professional judgment and proper documentation should be maintained where disclosure positions are taken based on the substance of the law rather than wording differences between ITR forms.

The differing treatment between ITR-2 and ITR-3 regarding foreign-listed shares, and the absence of the FA upload facility in ITR-3, appear more likely to be drafting/utility inconsistencies rather than deliberate policy changes. A Central Board of Direct Taxes clarification or revised utility would help eliminate ambiguity and avoid unnecessary compliance challenges for taxpayers holding foreign investments.