INCOME TAX UPDATES : Old vs New Tax Regime

Page Contents

INCOME TAX UPDATES : Old vs New Tax Regime

Choosing between the old and new tax regimes

Choosing between the old and new tax regimes at the beginning of the financial year is crucial for salaried individuals, as it directly impacts the Tax Deducted at Source (TDS) on their salaries. Here’s a detailed overview of the implications and considerations for FY 2024-25:

Understanding the Tax Regimes

Old Tax Regime:

- Features: Includes various deductions and exemptions such as House Rent Allowance (HRA), Leave Travel Allowance (LTA), standard deduction, and deductions under Section 80C (investments in PPF, life insurance, etc.), 80D (health insurance premiums), etc.

- Suitable For: Individuals who can maximize these exemptions and deductions, reducing their taxable income significantly.

New Tax Regime:

- Features: Lower tax rates with no exemptions or deductions. Tax slabs are designed to provide straightforward, lower rates without the need for complex tax planning.

- Suitable For: Individuals who do not have significant investments in tax-saving instruments or prefer a simpler tax calculation process.

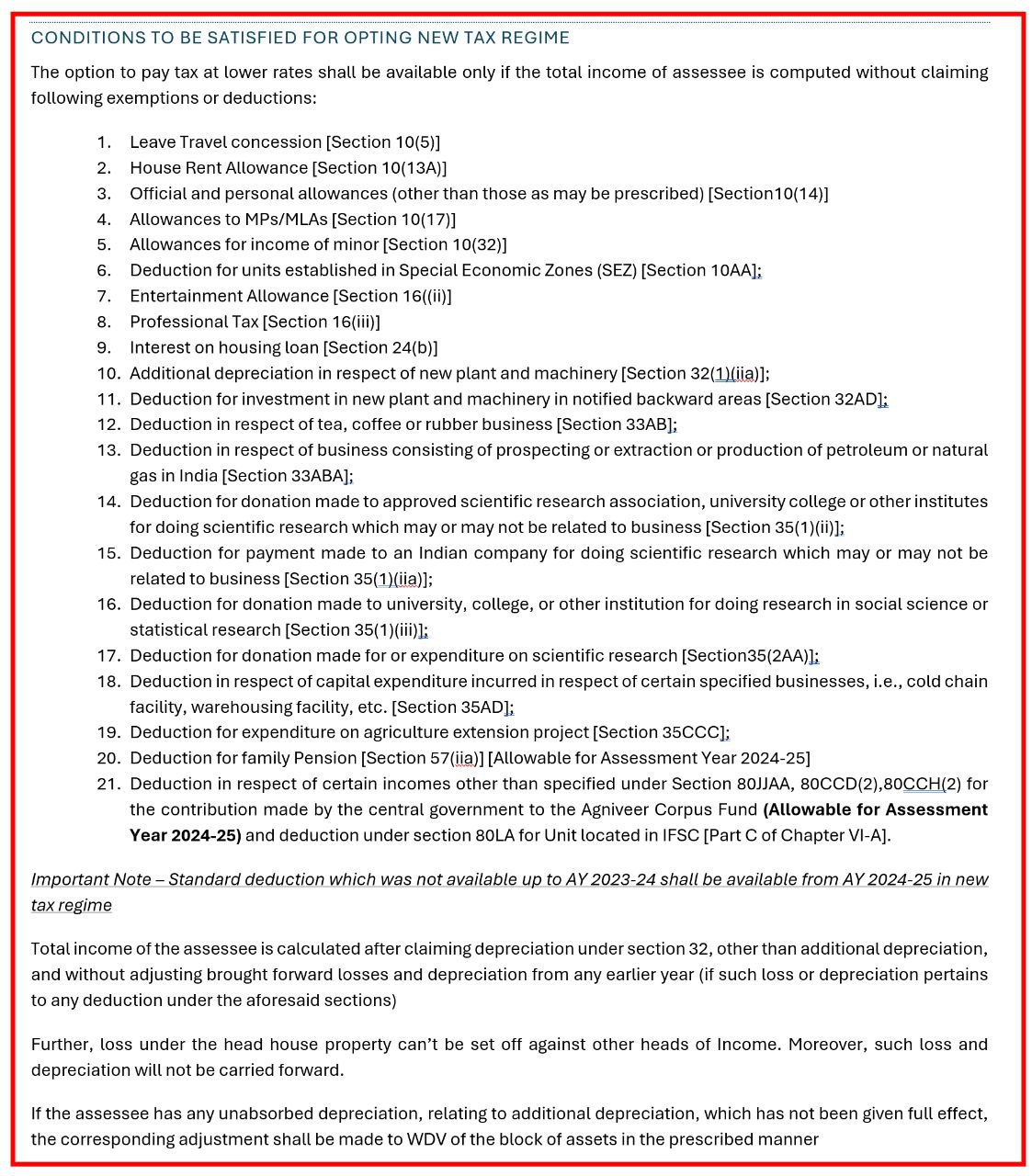

What are basic conditions to optin for New Tax Regime in Assessment Year 2024-25

Implications of Choosing the Wrong Tax Regime

-

- If you opt for the new tax regime but have significant eligible deductions and exemptions under the old regime, you might end up paying higher taxes since these benefits cannot be claimed under the new regime.

- Conversely, choosing the old regime without sufficient deductions can also lead to higher TDS compared to the new regime.Incorrect TDS deductions reduce your monthly take-home salary. This affects your cash flow and financial planning throughout the year.

- If the wrong regime is chosen, you may need to make adjustments when filing your income tax return, leading to a potential refund or additional tax liability. This can complicate the tax filing process and delay potential refunds.

- Assess your annual income, possible deductions, and exemptions to calculate your tax liability under both regimes. Various online calculators and tools can help with this.

- Analyze your previous year’s tax returns to understand your deductions and exemptions. This historical data can help predict your potential tax savings under the old regime.

- Inform your employer of your chosen tax regime promptly in April. This ensures accurate TDS calculation from the beginning of the financial year.

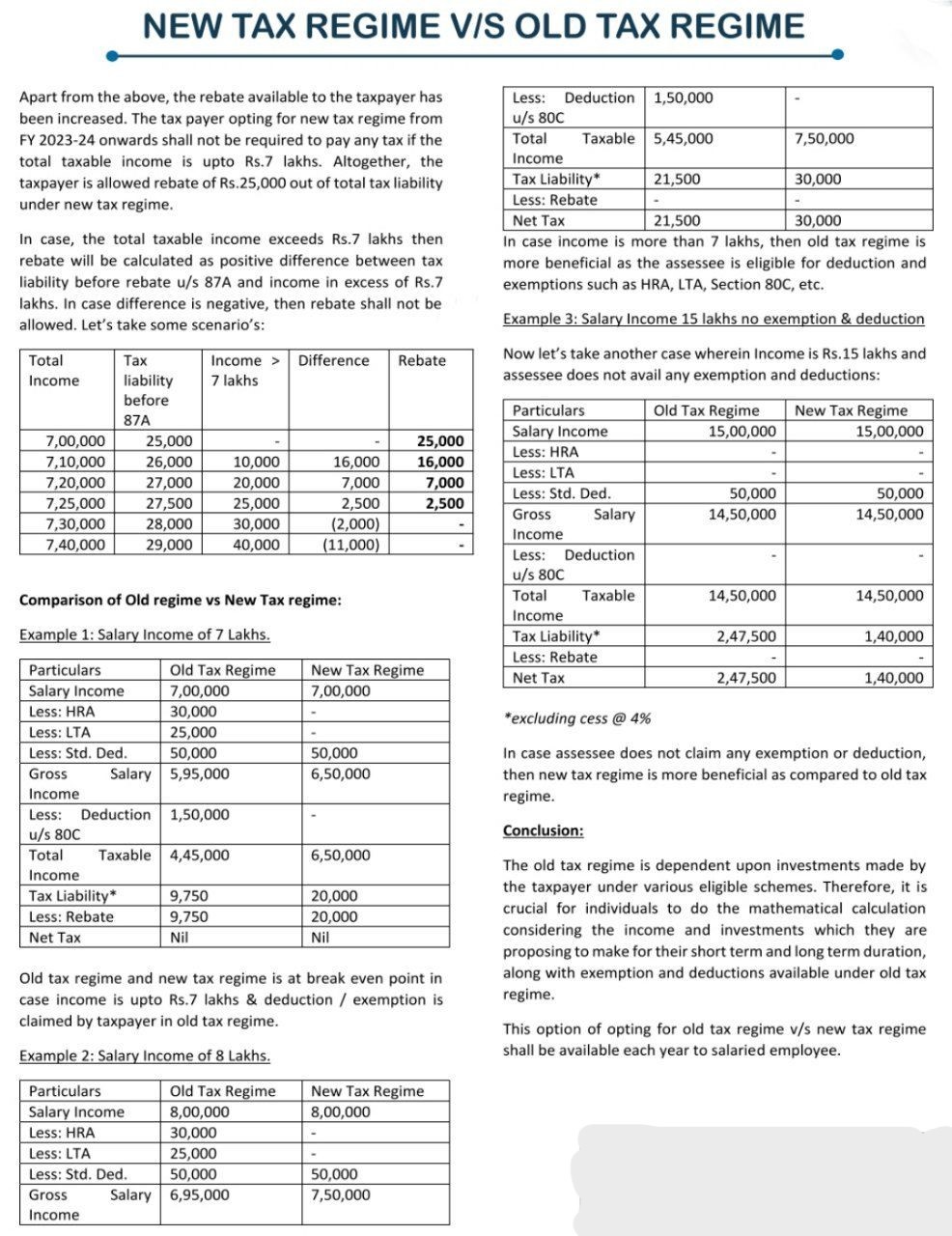

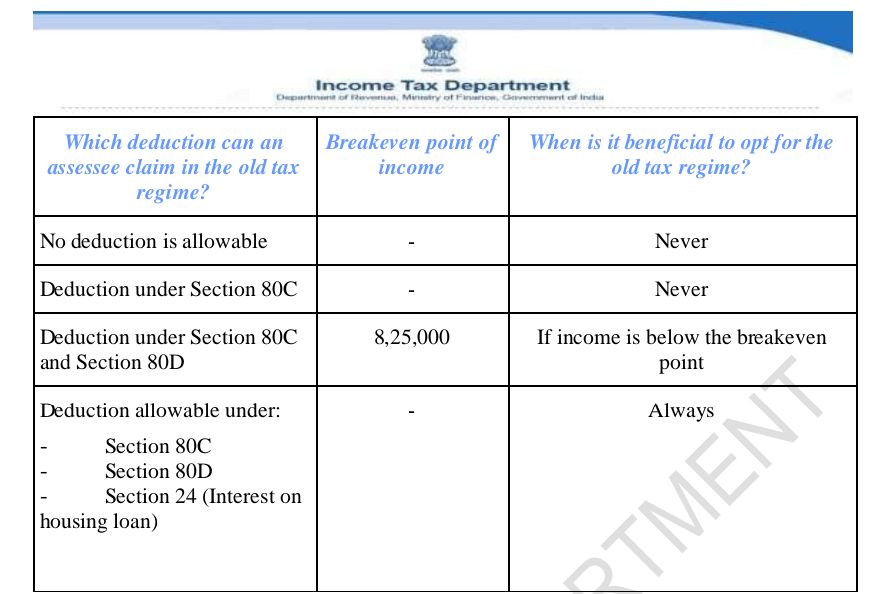

Which regime is beneficial for AY 2024-25?

NEW VS OLD TAX REGIME after Budget2023 announcement for diff salaried incomes

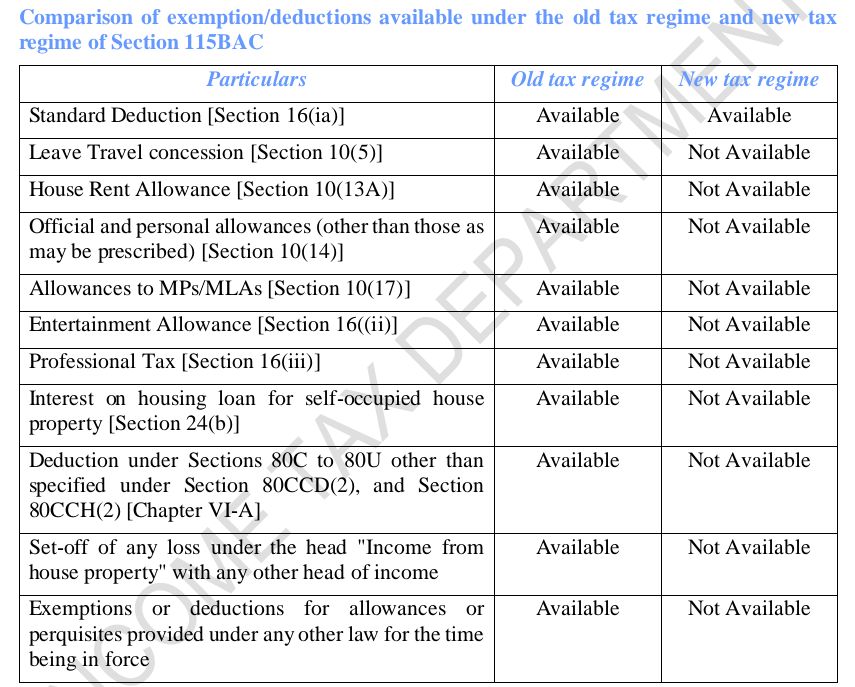

Comparison of exemption/deductions available under the old tax regime and new tax regime of Section 115BAC for AY 2024-25

Assumption- 80C investment 1.5 lac ( even other than Home loan) & 80D Mediclaim 25000 is claimed

Sum-Up

- New regime is default setting- You have to file form for opt old one

- For ppl having housing loan – Always Old regime is beneficial

- For ppl having NO housing loan – New regime is beneficial – It doesn’t make diff whether You are paying 80C+80D full

- Buis. ppl will have slight higher tax than above working as they wont get standard deduction of 50000

- Choosing the right tax regime is essential to manage your tax liability efficiently. Evaluate both regimes based on your financial situation and potential deductions.

- Making an informed choice in April will ensure proper TDS, better monthly cash flow, and smoother tax filing at the end of the financial year.