HOW TO RESPONSE INCOME TAX DEMAND NOTICE

Page Contents

IF a taxpayer income tax return differ from the assessment made by INCOME TAX OFFICER then taxpayer issued income tax demand notice. This notice is issued when the taxpayer has deposit less Tax for which he is liable to pay.

IF You received demand notice then here are the steps for respond the demand notice:-

Step 1: login in www.incometaxindiaefiling.gov.in with user ID, password, and date of birth.

Step 2 : Click on ‘E-file’ and go to ‘Respond to Outstanding Tax Demand’.

- The following details will be displayed –

- Assessment year

- Section code

- Demand notification number

- Date on which demand is raised

- Outstanding demand amount

- Uploaded by

- Rectification rights

- Response – submit and view

Step 3: Click on ‘Submit’ for the relevant assessment year. Choose one of the

options mentioned below-

- Demand is correct

- Demand is partially correct

- Disagree with demand

- Option 1‘Demand is correct,’ :-a pop-up screen appears with a message, ‘If you confirm, demand is correct then you can’t disagree with the demand.’ Click on submit if this is ok according to you. A success message shall appear on your screen.

- If any refund is due, the outstanding amount along with interest will be adjusted against the refund due.

- In any other case, you must repay the demand immediately. For this click on the option of Pay tax then click on confirm You will directly move to TIN website of NSDL where your outstanding tax amount is paid then click on the submit button.

- Option 2:Demand is partially correct, in this option you need to enter the correct amount and incorrect amount . If amount is incorrect then you need to specify at least one reason for it..

- Demand has already been paid – Provide the challan identification number (CIN). Also mention BSR code, date of payment, the serial number of challan and amount. If Challan identification number is not available, mention that demand has been paid by challan and Challan Identification Number is not available. Also mention the date of payment and amount payable.

- Demand has already been reduced by rectification/revision – Provide the date of order, demand amount, details of Assessing officer who has rectified. Next, upload rectification/appeal effect order passed by Assessing officer.

- Demand has already been reduced by appellate order but appeal effect has to be given by the department – Provide the date of order and the appellate order passed by and the reference number of order.

- Appeal has been filed and stay petition has been filed, or stay has been granted by, or installment has been granted by – Provide the date of filing of the appeal, appeal pending with (details of CIT (A), stay petition filed with (details of office). If the stay has been granted, you have to also upload the copy of the stay order.

- Rectification/revised return has been filed at CPC – The following details are required additionally:

- Filing type

- E-filed acknowledgment number

- Remarks (comments, if any of the tax payer)

- Upload challan copy

- Upload TDS certificate

- Upload letter requesting rectification copy

- Upload indemnity bond

- Rectification has been filed with assessing officer – Mention the date of application and remarks.

- Option 4 – Demand is not correct If the taxpayer choose the option of demand is not correct then taxpayer select the option as mention in disagree with the demand.

- Option 3– ‘Disagree with the Demand’ then the taxpayer must provide the details of disagreement along with reasons. The reasons are the same as the mentioned above under ‘demand is partially correct.’ After submitting a response, the success screen would be displayed with the transaction.

If the taxpayer wants to view the response submitted by taxpayer then clicking ‘View’ under the response column and the following details will be displayed

- Serial number,

- Transaction ID,

- Date of response and response type.

If the assessee fails to pay part or whole of the demand raised by INCOME TAX AUTHORITIES under section 156 within 30 days of receipts, is termed as assessee in default.

HOW TO RESPONSE INCOME TAX DEMAND NOTICE

Consequences/Penalty of Assesses in default

If the person to whom the section 156 tax notice for demand has been issued fails to pay the amount demanded within the time limit provided under the section 156 tax notice, then the assessee is liable for following penalties:

Interest u/s 220

Under section 220 interest at the rate of 1% per month or part thereof is payable after the expiry of the 30 days time given in section 156. However, the Principle Chief Commissioner / Chief Commissioner / Principle Commissioner/Commissioner can reduce the interest if he is satisfied with all of the three following conditions that:

(a) Payment of such amount will cause genuine hardship to the assessee;

(b) Default was due to the circumstances beyond the control of the assessee, and

(c) The assessee has co-operated in the inquiry relating to assessment/recovery proceedings

Penalty u/s 221

Under section 221 there is some penalty imposed by the AO on the assessee but it should not be more than the amount demanded in the Demand Notice. Before charging penalty as discussed above, the tax authorities shall give the taxpayer a reasonable opportunity of being heard. No penalty is levied if the taxpayer proves to the satisfaction of the tax authorities that the default was for good and sufficient reason

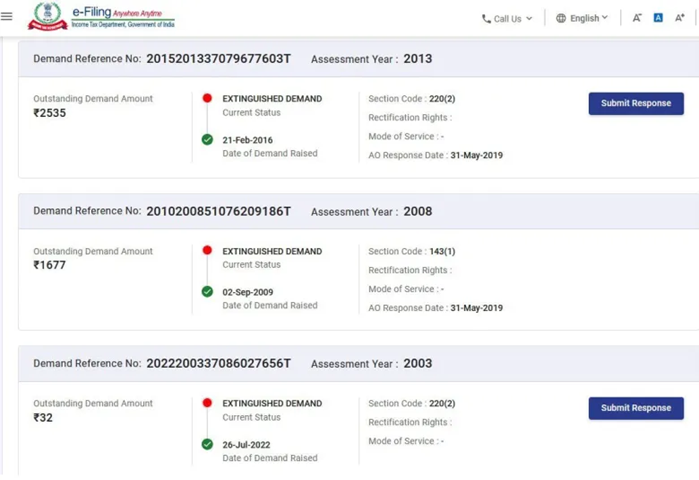

Income Tax Dept Initiates Closure of Old Demands through Tax Portal

The Income Tax Dept has started the process of closing previous demands via Income Tax Portal in an effort to streamline tax operations and improve taxpayer convenience. This project is a critical step towards achieving the goals set forth in the Interim Budget 2024, which include decreasing the backlog of unpaid tax requests and guaranteeing increased effectiveness in tax administration.

As the Pic showing that the income Tax demands above INR 25k are closed.

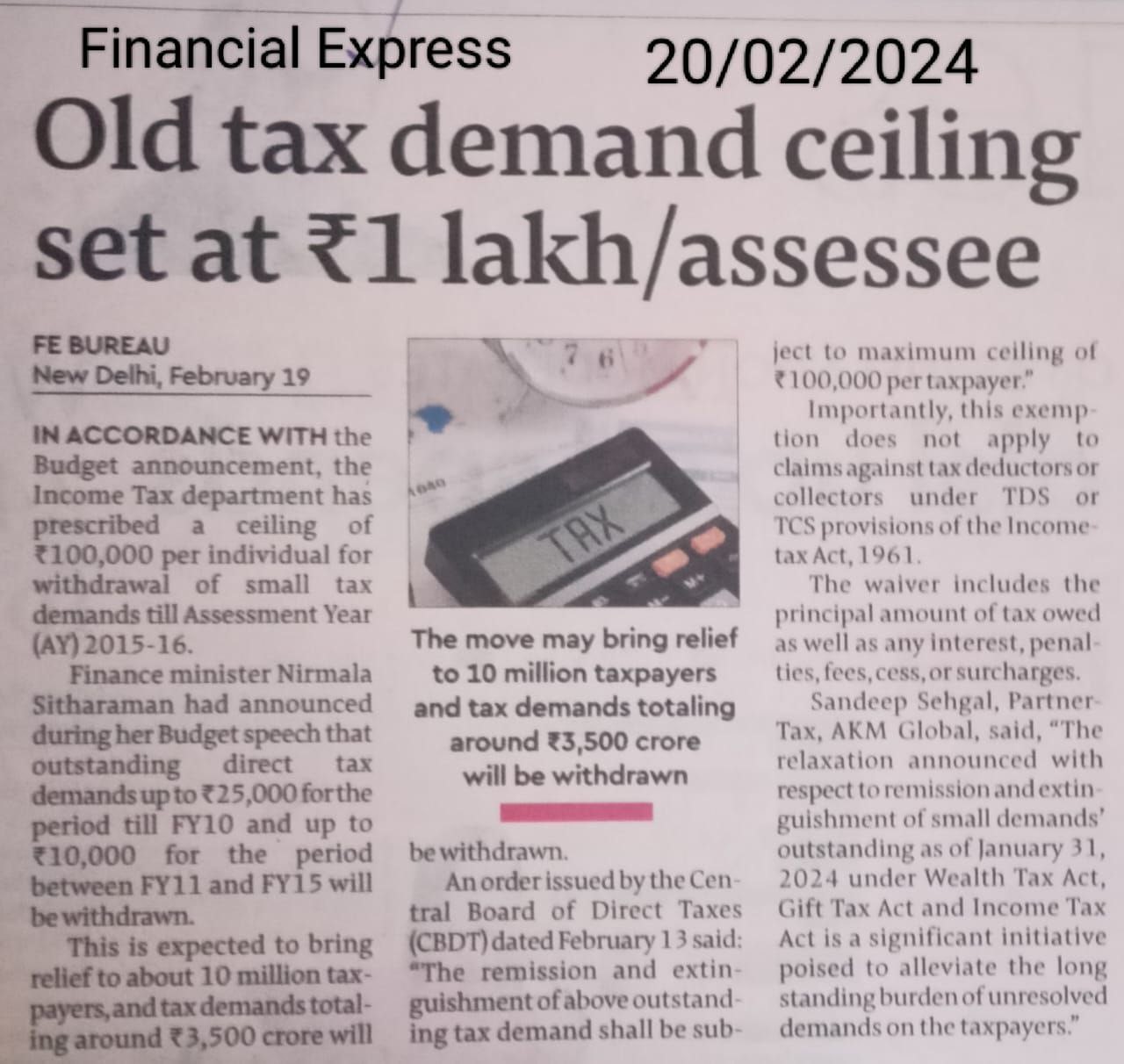

Old Tax Demand Ceiling set at Rs. 1,00,000/ Assessee

CBDT waive-off Income Tax Demands