GST Registration Document Requirements

Page Contents

GST Registration Roadmap:

A Practical Guide for Businesses. Understanding GST registration can feel overwhelming, but with the right roadmap, it becomes not just simple, but businesses navigate GST registration effectively: GST Registration Matters for business, legal compliance, Input tax credit benefits, Seamless interstate trade, Better vendor & customer trust and a strong foundation for business growth. GST registration is not just a statutory requirement. it’s a strategic business decision. Choosing the right time and the right scheme can save tax, simplify compliance, and unlock growth.

When Is GST Registration Mandatory:

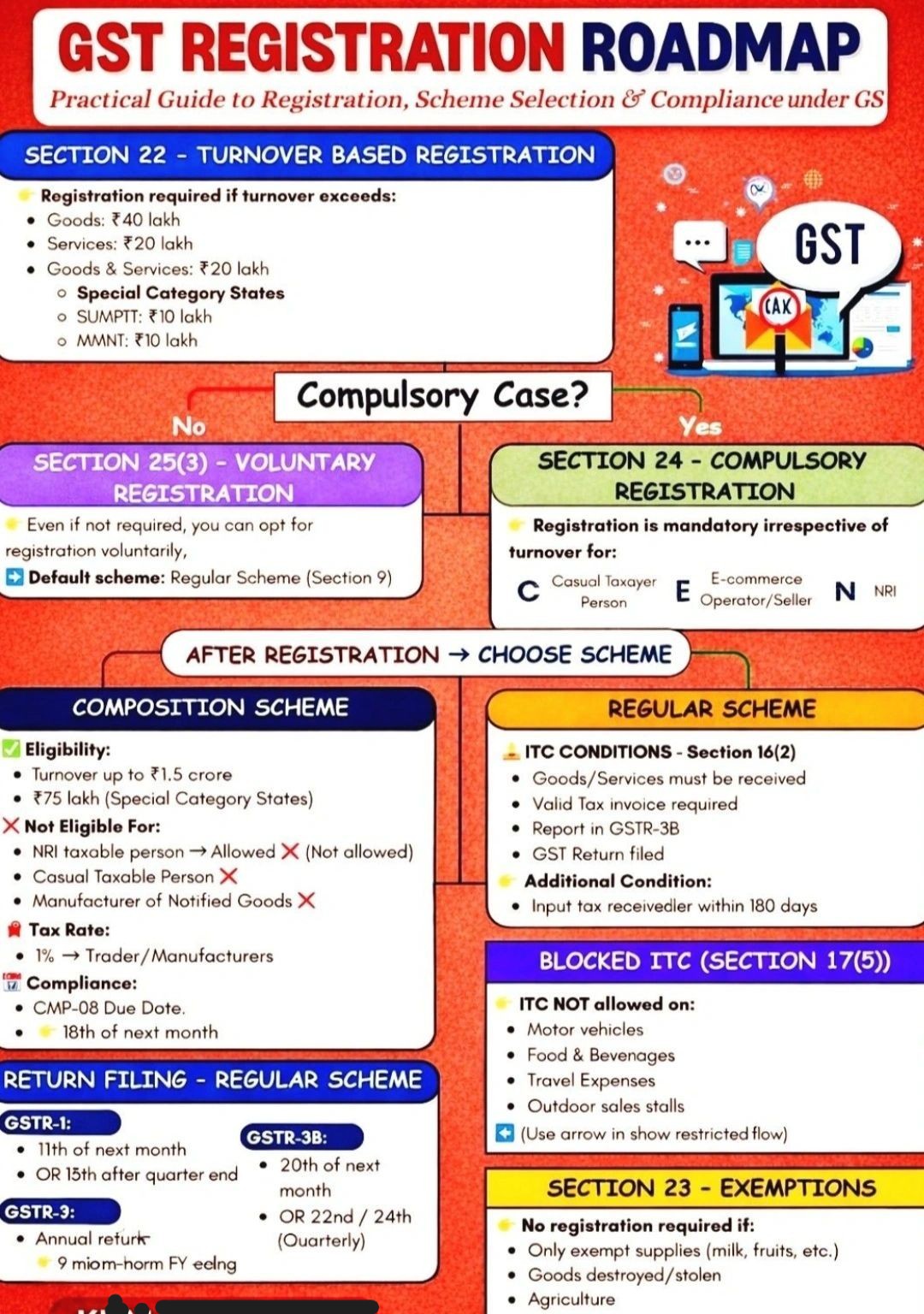

Turnover‑Based Registration — Section 22 : GST registration is compulsory once aggregate annual turnover exceeds

- INR 40 lakh – Supply of Goods

- INR 20 lakh – Supply of Services

- INR 10 lakh—Applicable for special category states.

- The threshold applies PAN‑India, not state‑wise.

Compulsory Registration — Section 24 : Irrespective of turnover, GST registration is mandatory for e‑commerce sellers & operators, casual taxable persons, non‑resident taxable persons, persons liable to reverse charge, and agents supplying on behalf of registered persons.

Voluntary Registration—Section 25(3) : Businesses may opt for GST registration voluntarily, even below threshold limits, to Claim Input Tax Credit (ITC), Deal with GST-registered clients, Enhance business credibility and Enable expansion to new markets

GST Registration Document Requirements

Summary of the GST Registration Document Requirements as per Instruction No. 03/2025-GST: (As per Instruction No. 03/2025-GST)

| Circumstance | Documents Required |

|---|---|

| Owned Premises | Any ONE of the following: ✓ Property Tax Receipt ✓ Municipal Khata ✓ Electricity Bill ✓ Water Bill ✓ Similar document under State laws |

| Rented Premises (Unregistered Rent Agreement) | 1. Unregistered Rent Agreement 2. Any ONE ownership proof of lessor: ✓ Property Tax Receipt / Electricity Bill / etc. 3. Lessor’s ID Proof |

| Rented Premises (Registered Rent Agreement) | 1. Registered Rent Agreement 2. Any ONE ownership proof of lessor: ✓ Property Tax Receipt / Electricity Bill / etc. |

| Electricity/Water Bill in Applicant’s Name | 1. Utility Bill (Electricity/Water) in Applicant’s Name 2. Rent Agreement ✓ No Lessor documents required |

| Premises Owned by Spouse/Relative | 1. Consent Letter (plain paper) 2. Owner’s ID Proof 3. Any ONE ownership proof: ✓ Property Tax Receipt / Electricity Bill / etc. |

| Shared Premises (Registered Rent Agreement) | 1. Registered Rent Agreement 2. Any ONE ownership proof of lessor: ✓ Property Tax Receipt / Electricity Bill / etc. |

| Shared Premises (Unregistered Rent Agreement) | 1. Unregistered Rent Agreement 2. Any ONE ownership proof of lessor: ✓ Property Tax Receipt / Electricity Bill / etc. 3. Lessor’s ID Proof |

| Shared Premises (No Agreement) | 1. Consent Letter from Owner 2. Owner’s ID Proof 3. Any ONE ownership proof: ✓ Property Tax Receipt / Electricity Bill / etc. |

| Rented/Leased without Agreement | 1. Affidavit (on non-judicial stamp paper before Magistrate/Notary) 2. Utility Bill in Applicant’s Name |

| SEZ Units | ✓ SEZ Certificate or Letter issued by Government of India |

After Registration: Choose the Right Scheme : Composition Scheme : Best suited for small businesses with limited compliance needs Turnover limit: Up to INR 1.5 crore, lower tax rates, simplified returns; however, No ITC claim, not available for e‑commerce sellers, non‑resident taxable persons, and inter‑state suppliers.

Regular Scheme

Ideal for growing and scalable businesses:

- Input Tax Credit available

- Mandatory tax invoices

- Regular return filing

- Suitable for B2B transactions and exports

Blocked ITC — Section 17(5) : Input Tax Credit cannot be claimed on certain expenses, including motor vehicles & conveyance, food & beverages, outdoor catering, travel & tourism, and personal or non‑business expenses. Proper expense classification is critical to avoid ITC reversal and penalties.

GST Return Filing – Regular Scheme

- GSTR‑1 – Monthly / Quarterly (Sales details)

- GSTR‑3B – Monthly / Quarterly (Tax payment)

- Annual Return (GSTR‑9) – Yearly compliance

- Late filing attracts interest & late fees and blocks ITC for recipients.

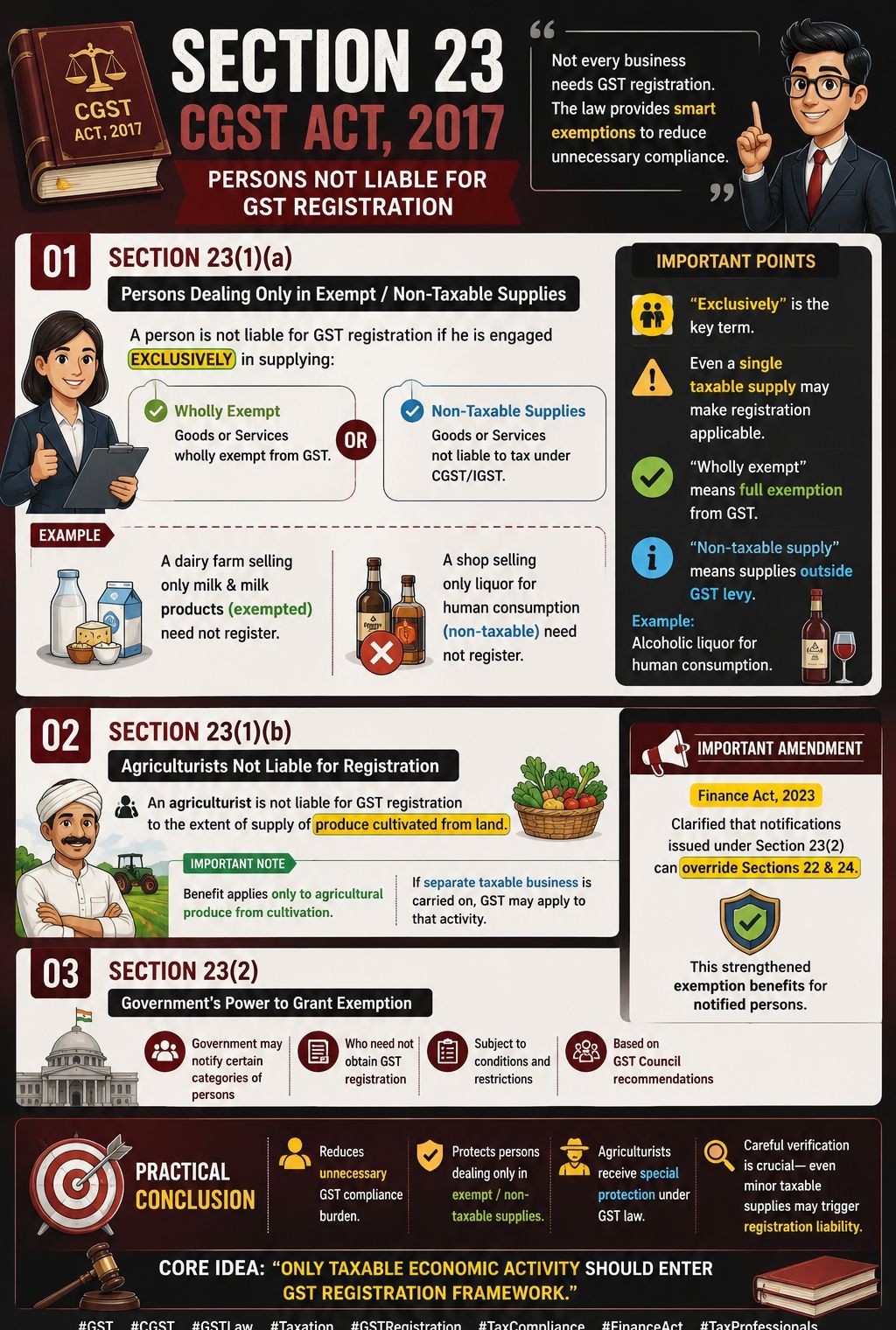

- Exemptions from GST Registration — Section 23 : GST registration is not required if the business deals exclusively in Exempt goods or services, agricultural activities, and activities notified by the government (specific cases).