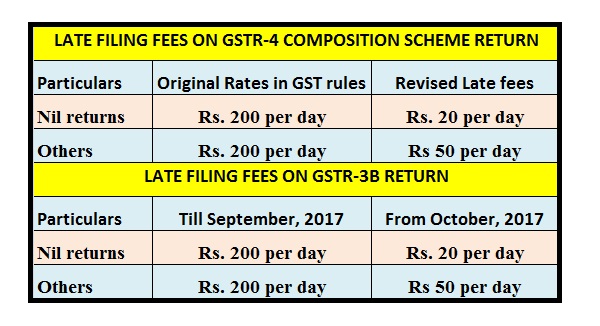

GST: Late fee capped at Rs. 500/- for each GSTR-3B Return

Page Contents

www.carajput.com; GST No late Fees

GST: Late fee capped at Rs. 500/- for each GSTR-3B Return & waives off late filing fee

For each GSTR-3B return, a late fee of Rs. 500/- is capped.

In the perspective of the GST taxpayers’ massive relief the government has chosen to limit, on the basis of the condition that such GSTR-3B reports are filed prior to 30 September 2020, a late maximum fee of Form GSTR-3B to Rs 50/- (only 500) by tax return for the tax period July 2017 to July 2020.

Notice was provided to include zero late fees if no tax liability exists; and if there is any tax liability, the GSTR-3B returns filed by 30 September 2020 will be subject to a maximum late fee of Rs. 500 for such returns.

Thanks to further flexibility in the deferred fee paid for tax periods between May 2020 and July 2020, numerous representations have been issued.

In order to clean up past pendency of returns between July 2017 and January 2020, relief has been issued for February 2020 of April 2020 in addition to previously granted.

In addition, the design and implementation of a standard late payment are easier on an automated common portal.

The late fee for the return is only limited to Rs. 500/- if it is filed before 30 September 2020.

Experts say that Late fee relief to non-filers of GST returns will aid small businesses and boost revenue.

The GST Council, chaired by finance minister Nirmala Sitharaman and made up of state ministers, agreed to introduce an amnesty scheme to give taxpayers respite from late fees for pending returns.

For those taxpayers who did not have any tax burden, the late fine for non-furnishing of GSTR-3B from July 2017 to April 2021 has been restricted at Rs 500 per return.

GST Taxpayers who owe money will be penalised a maximum of Rs 1,000 in late fines if their returns are not filed by August 31, 2021.

GST UPDATE : GST mismatch between GSTR-1 and GSTR -3B.

- Under Section 75(12) relief to taxpayers in case tax officer takes “reasonable time” to explain GST mismatch between GSTR-1 and GSTR -3B.

- Follow up with your suppliers to ensure that they file GSTR-1 by the Timeline due date otherwise GST input tax credit would be denied due to implementation of under Section 16(2)(aa).

- New interest calculator feature has been added In GSTR-3B.

- The appropriate interest applicable, if any, on the tax due declared in the GSTR-3B for a specific tax period shall be determined after the GSTR-3B has been filed. These were auto-populated in the GSTR-3B’s Table-5.1 for the next tax period.

Summary of Important Due date of July and Aug 2020

Popular Article :

Popular Article :