GST Implications on pre-packaged & labelled goods

Page Contents

GST Implications on pre-packaged & labelled goods

List of GST-Exempted Food Items in India under the Goods and Services Tax Council framework:

Under GST, basic and unbranded food items are generally exempt to protect consumers, while branded and packaged goods attract GST.

Fresh & Unprocessed Food (Fully GST Exempt – 0%) : These items are exempt if not branded and not pre-packaged & labelled, Fresh fruits & vegetables, Fresh milk (not flavoured), Curd, lassi (loose), Eggs, Fresh meat & fish (not frozen/processed), Natural honey (raw/unprocessed), Whole grains (rice, wheat, maize, barley), Flour (atta, maida, besan – loose), Pulses (loose/unbranded)

GST Rate: 0% : Unbranded Basic Staples (Loose Supply) i.e Loose rice, Loose pulses, Loose sugar, Jaggery (gur), Salt (non-branded) and If pre-packaged & labelled, GST applies (usually 5%).

Certain Dairy & Agricultural Products (Exempt): Fresh paneer (loose), Buttermilk (loose), Raw milk and Natural raw honey. From July 2022 onwards. Even unbranded food items attract GST (usually 5%) if they are pre-packaged and labelled, as per GST amendment rules. Example: Loose rice → 0% GST and 1 kg sealed rice packet (labelled) → 5% GST.

This change significantly impacted kirana traders and FMCG distributors.

Quick Comparison Table List of GST Exempted Food Items in India

| Food Item Type | GST Rate |

| Fresh fruits & vegetables | 0% |

| Loose grains & pulses | 0% |

| Pre-packaged rice/pulses | 5% |

| Branded processed food | 5% / 12% / 18% |

| Restaurant food (non-AC small) | 5% (without ITC) |

On what instances is GST applicable on pre-packaged & labelled goods?

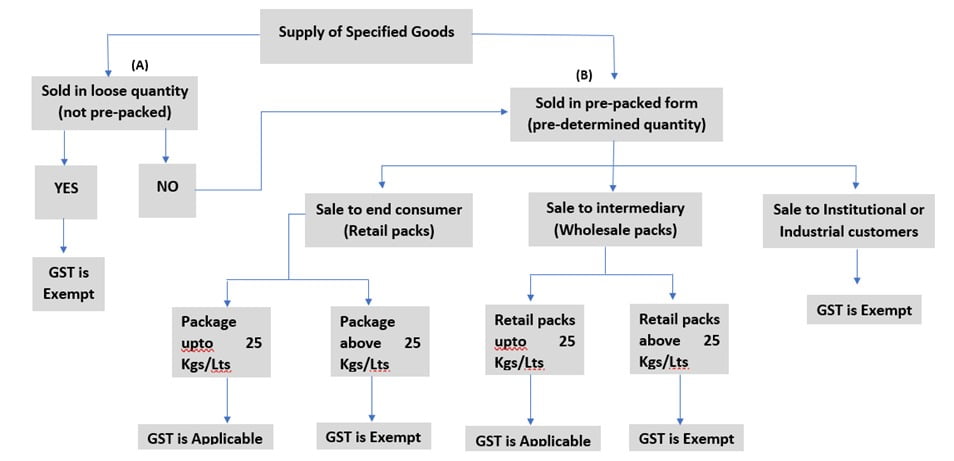

To conclude, Goods and services Tax is applicable on specified food items when they are “prepacked & labelled” as defined in Central Tax (Rate) Notification No. 06/2022. In this reference with the Legal Metrology Act & Packaged Commodities Rules, Goods and services Tax is applicable on pre-packaged commodities that are required to make declarations under Rule 6 of Packaged Commodity Rules. To conclude, Goods and services Tax is applicable on specified goods:

- In case it is packed in bags of 50kg or less in case of agricultural farm produce

- If the packed in bags of 25kg or less for other products

As is clear from frequently asked questions issued by the govt., the intent is to tax all packages less than 25 kg (whether sold to dealers or ultimate consumers). But the legal lacuna discussed under the head “Goods and services Tax Implications on Wholesale Packages” continues to remain (since there have been no clarifications regarding the same from the Govt of India yet).

Instances where pre-packaged goods on which Goods and services tax is not applicable:

- Any commodity with net weight of 10 g / 10 ml or less (except tobacco & tobacco products)

- Other specified food items when packed in bags of more than 25kg

- Sale of pre-packaged food items mentioned above when sold to any industry or institution for use by such industry/institution.

- Any thread which is sold in coil to handloom weavers

- Goods containing scheduled formulations & non-scheduled formulations covered under Drugs (Price Control) Order, 2013, made under U/s 3 of the Essential Commodities Act,

- Agricultural farm produce more than 50 kg.

- Any package containing fast food items packed by restaurant or hotel & the like

- Export of prepackaged & labelled goods specified in table above

Input Tax Credit Implications for businesses on prepackaged goods

- Businesses engaged in taxable supplies of pre-packaged & labeled goods would be eligible to avail of an input tax credit of all input, input services & capital goods subject to fulfilment of conditions & restrictions specified in Sections 16, 17 & 18.

- Specifically, businesses in such industries would be required to apportion common inputs (such as rent, transportation charges, etc.) between the taxable turnover (supply of pre-packaged goods 25 kg or less) & exempt supplies (supply of pre-packaged goods more than 25 kg).

Input Tax Credit on inputs held in stock

- Business entities which were previously exclusively engaged in supplying exempt goods will now end up being engaged in supplying taxable supplies also due to the implication of GST Central Tax (Rate) Notification No. 6/2022.

In terms of Section 18(1)(d) of the Central Goods and Service Tax Act 2017:

- “Where an exempt supply of goods or services or both by a registered person becomes a taxable supply, such person shall be entitled to take credit of input tax in respect of inputs held in stock & inputs contained in semi-finished or finished goods held in stock relatable to such exempt supply & on capital goods exclusively used for such exempt supply on the day immediately preceding the date from which such supply becomes taxable. Provided that the credit on capital goods shall be reduced by such percentage points as may be prescribed in rule 40 of Central Goods and services Tax rules.

- Moreover, Under Section 18(2) specifies that a registered person shall not be entitled to take Input Tax Credit under section 18(1), in respect of any supply of goods or services or both to him after the expiry of one year from the date of issue of tax invoice relating to such supply.

Thus, Input Tax Credit may be availed on:

- Inputs in stock relatable to such previously exempted supply

- The Inputs in semi-finished goods in stock relatable to such previously exempted supply

- Capital goods exclusively used for such previously exempted supply

- Inputs in finished goods in stock relatable to such previously exempted supply

Rule 40 of Central Goods and services Tax Rules provides for the below following procedures and conditions for availing input tax credit in such cases:

- Input Tax Credit on capital goods u/s 18(1)(d), shall be claimed after reducing the tax paid on such capital goods by 5% points per quarter of a year or part there of from the date of the

- The registered person shall within a period of 30 days from the date of becoming eligible to avail Input Tax Credit shall make a declaration, electronically, on the common portal in FORM GST ITC-01 to the effect that he is eligible to avail Input Tax Credit as aforesaid. This time limit may be extended by the Commissioner by a

- Declaration in ITC-01 shall specify the details relating to the inputs held in stock or contained in semi-finished/finished goods in stock, or as the case may be, capital goods on the day immediately preceding the date from which the supplies made by the registered person become taxable.

- The declaration shall be duly certified by a CA in practice or an ICMAI in practice if the aggregate value of the claim on account of the Central Goods and Services Tax Act, 2017, State Goods and Service Tax, Union Territory Goods and Service Tax & Integrated Goods and services Tax More than INR 200,000/-.

- Input Tax Credit claimed in accordance with the above provisions shall be verified with the corresponding details furnished by the corresponding supplier in GSTR-4/ GSTR-1.

Now, a question arises: can businesses claim Input Tax Credit of inputs held in stock & capital goods through Form ITC-01 (even after expiry of 30 days from date of taxability, i.e., after 17th August 2022)? Please refer to the full-length research paper to know more.

Impact on the Country:

Will this amendment encourage businesses to violate the provisions of Legal Metrology Act?

- Post introduction of this amendment w.e.f. 18th July 2022, it is seen that many industries & businesses have began to pack their products, such as rice, wheat, flour, etc., in packs of 26kg to get Goods and services tax exemption.

- Packing it in 26kg will also get them exempted from declaration requirements under Rule 6 of Packaged Commodities Rules. If few businesses in the industry start packing in 26kg to avoid price rise due to Goods and services tax, the other players will also follow suit in the competitive pressure.

- In such cases, when businesses are prompted to get themselves out of Legal Metrology Act net, due to Goods and services tax implications, will the Government decide to tax such food items irrespective of quantity & delinking it from Legal Metrology law?

- Further, this may also lead to retailers to start selling in loose form. Question arises if this will lead to affecting the quality of the product or increase in adulteration?

Would it lead to an increase in cash business?

- One of the objectives of the introduction of the Goods and Services Tax was to create a transparent economy. The benefit of input tax credit pushed businesses to register under the goods and services tax & disclose their transactions in their returns.

- However, the goods and services tax on pre-packaged food items meant for retail sale goes beyond this objective & aims to tax business-to-consumer transactions where there is no scope for input tax credit benefits.

- Taking into consideration competitive aspects also, businesses may tend to go into unaccounted sales to avoid goods and services tax .

- Compliance of procedures such as Goods and services tax registration & returns and proper accounting of transactions may prompt smaller retailers/wholesalers to resort to unaccounted sales”

Impact on “Poverty line” in India:

- In order to counter Goods and services tax implications, businesses may tend to sell the food items in loose form, which would lead to distribution of sub-standard products in black markets, making it more affordable for those below the poverty line. This may lead to spread of unhygienic living and ill health.

Written by the RJA -Team

RJA give clients adequate guidance & assistance as they deal with internal audits as well as government audits of various corporate solutions (like statutory audits, ROC compliance, business incorporation & company winding-up) in India. Please get in contact with us if you have any questions or would need more information concerning with GST compliance-related consultancy. Contract – 9555 555 480 or singh@carajput.com