FAQ on Liberalized Remittance Scheme

Page Contents

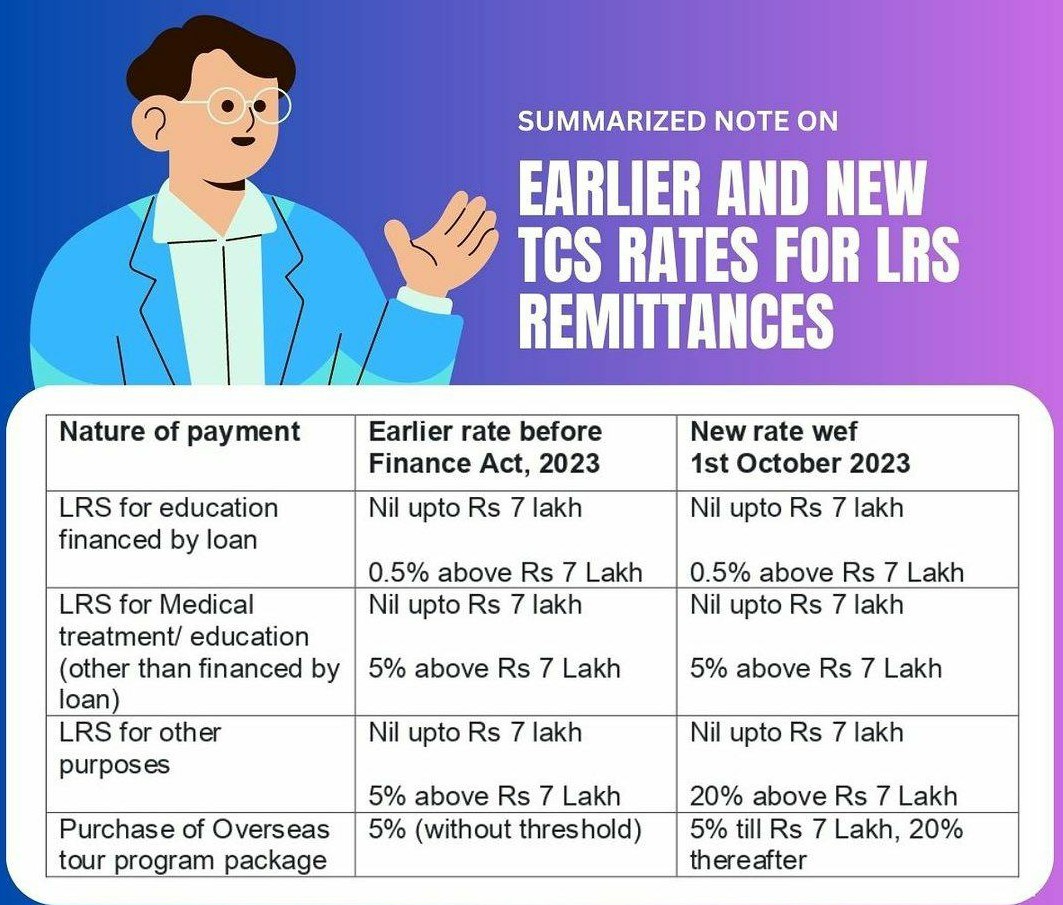

TCS on Fund Transfer Outside India – Under LRS (Liberalised Remittance Scheme)

As per Finance Act 2020 (amended by Finance Act 2023), any remittance of funds outside India under the Liberalised Remittance Scheme (LRS) is subject to TCS (Tax Collected at Source) under Section 206C(1G) of the Income Tax Act.

Key TCS Provisions on Foreign Remittance (as of FY 2024–25):

| Purpose of Remittance | TCS Rate | Threshold |

|---|---|---|

| For medical or education (loan from financial institution) | 0.5% | Above ₹7 lakh/year |

| For medical or education (own funds) | 5% | Above ₹7 lakh/year |

| For other purposes (e.g. investment, gift, maintenance, property purchase, tour, etc.) | 20% | From ₹1 (no threshold) |

-

≤ ₹7 lakh and for education/medical

-

Done through loan from a financial institution

Examples:

-

Gift to NRI Son/Daughter = ₹10 lakh

→ TCS @ 20% on ₹10 lakh = ₹2 lakh

→ Collected by bank/remitting institution at time of transfer -

Sending ₹6 lakh for daughter’s tuition fees abroad (own funds)

→ No TCS (below ₹7 lakh threshold) -

Investment in foreign stocks (₹5 lakh) → TCS @ 20% = ₹1 lakh

TCS on International Credit Card Usage

-

As per Rule 7 of FEMA 2023, use of international credit cards abroad will not attract TCS under LRS for business or personal expenses. However, debit card or forex card remittance still comes under LRS and TCS may apply.

Can You Claim Refund of TCS?

Yes, TCS is not a final tax – it is adjustable against your total tax liability while filing your Income Tax Return (ITR). If excess TCS is paid, you can claim a refund. Banks and authorized dealers collect TCS at the time of remittance., Rate varies based on purpose and amount. Declaration of purpose is mandatory for correct rate application.

Frequently Asked on TCS on Liberalized Remittance Scheme.

Questions: 1. what is the effective date of introduction of the tax implications?

The effectiveness of the Tax collected at the source clause on international remittances is updated from 1 April 2020 to 1 October 2020.

Question:2. What all transactions will be affected by this Tax collected at source requirement?

- All remittances in excess of INR 7 lakh in the financial year under the LRS will be liable for 5 percent of TCS, except where the remittance is for education paid out through a loan from any financial institution.

- The rate would then be decreased from 5% to 0.5%.

- The exclusion from TCS for remittances abroad under LRS for sums just under INR 7 lakh in the financial year would not apply if the sum is charged for the purchase of the overseas tour program kit.

Questions:-3. Can GST be applied to the 5% TCS collected?

No GST would refer to the tax collected by the TCS. However, GST will refer to the conversion & remittance service fee of the currency.

Questions:-4. what are the various reasons for which the tax collection applies?

Tax would apply to all remittances from India that come under the Liberalized Remittance Scheme (LRS) of RBI.

Questions:-5. what are the various Purpose permitted under LRS?

Following are the purposes permitted under LRS.

- Private visits to any country (excluding Nepal and Bhutan)

- Donation or charity;

- Study abroad

- Moving overseas to work

- Emigration:

- Maintenance of loyal family members abroad

- Travel for business, or attending a conference or advanced training, or meeting expenses for meeting medical expenses, or checking abroad, or accompanying a patient going abroad for medical treatment/check-up;

- Expenditures for medical care overseas

- Any other current account transaction not protected in FEMA 1999.

Questions:-6. what are the various permissible capital account transactions by an individual for purposes permitted under LRS?

Permissible capital account transactions by an individual under LRS are:

- Investments abroad – acquisition and holding of shares in both listed and unlisted foreign companies or debt instruments; 5 acquisition in qualified shares of a foreign company for the role of the director; acquisition of shares of a foreign company for professional services rendered or in lieu of remuneration of the director; investment in units of mutual funds, venture capital funds;

- Establishment of wholly-owned subsidiaries and joint ventures (with effect from 05 August 2013) outside India for a bonafide company subject to the terms and conditions set out in Notification No FEMA.263 / RB-2013 of 5 March 2013;

- to extend loans, namely loans in Indian Rupees, to non-resident Indians (NRIs) who are relatives.

- the opening of foreign currency accounts with a bank abroad;

- purchase of foreign property;

Questions:-7. What’s Dynamic Currency Conversion (DCC)?

- Many international traders offer the ‘Dynamic Currency Conversion’ facility – which enables customers to make purchase payments directly in their home currency (i.e. Indian Rupees for cards issued in India).

- This service is provided by selected international merchants or websites. The final transaction amount (as determined by the merchant / DCC service provider) must be checked by you before the payment is made. Depending on the sum given by the merchant, Citi will charge you the final amount (Indian Rupees).

- The conversion procedure, the exchange rate, and any markup applied in such cases shall be decided, as the case may be, by the applicable merchant or DCC service provider.

- If we do not opt for DCC, you will be billed in local currency by the merchant. If the local currency is not USD, then the transaction is translated first from the local currency to $ then from $ to INR.

How to avoid TCS on foreign remittance -LRS – Revised Rate