Choosing Between New Tax Regime & Existing Old Regime

Page Contents

Choosing Between the New Tax Regime & Existing Old Regime

In case Salaried Taxpayers, They Choose the old regime at the beginning of the FY and inform the employer; can change choice when filing the return. & In case Non-Salaried Taxpayers, They Choose the regime when filing the tax return; once opted out of the new regime, cannot switch back. Planning: Essential to compare both regimes and plan investments and tax payments accordingly. Use Form 10IEA if opting for the old regime. Proper planning and understanding of the rules can help taxpayers maximize their tax benefits under the chosen regime.

For Salaried Taxpayers:

- The new tax regime is the default from Financial Year 2023-24. At the beginning of Financial Year 2023-24, a salaried taxpayer can opt for the old regime and inform their employer. Once the choice is made, it cannot be changed during the financial year through the employer.

- The employee can change their choice when filing the income tax return in July 2024. The due date for filing the tax return for Financial Year 2023-24 (Assessment Year 2024-25) is 31st July 2024, unless extended.

- If an employee does not choose the old tax regime at the beginning of the financial year, the employer will deduct TDS under the new tax regime by default.

- A salaried taxpayer can choose the new tax regime in one year and switch to the old regime in another year when filing returns.

For Non-Salaried Taxpayers:

- Non-salaried taxpayers must choose the new regime when filing their tax return. No need to declare or intimate their choice during the year.

- Non-salaried taxpayers (those with income from business or profession) cannot switch between regimes every year. Once they opt out of the new tax regime, they cannot opt-in again in future years.

Tax Planning and Intimation- Choosing Between New Tax Regime or Existing Old Regime :

- From a tax planning perspective, choosing the tax regime at the beginning of the financial year is essential. Compare tax liabilities under both regimes to make an informed decision.

- Form 10IEA- If intending to opt for the old tax regime, the taxpayer must furnish Form 10IEA to the income tax department before filing the return.

- Investment and Tax Calculations- Investments, TDS, or advance tax payable calculations should be planned according to the chosen regime.

Choosing Between the New Tax Regime & Existing Old Regime

The choice between the new and old tax regimes depends largely on the total deductions you can claim. Here is a detailed comparison based on the deduction amounts:

- Total Deductions Less Than ₹1.5 Lakhs: Under the New Tax Regime. The new regime offers lower tax rates and becomes beneficial when deductions are minimal. Taxpayers with fewer deductions can take advantage of the concessional rates without losing much in terms of deductions.

- Total Deductions Exceeding ₹3.75 Lakhs: Choose the Old Tax Regime. When deductions are high, the old regime, with its higher rates but more allowable deductions, becomes more beneficial. Taxpayers can reduce their taxable income significantly with these deductions, leading to lower overall tax liability despite the higher rates.

- Total Deductions Between ₹1.5 Lakhs and ₹3.75 Lakhs: Choose the the New or Old Determining Factor is Income Level. In this range, the choice of regime depends on the taxpayer’s income level:

-

- Lower Income Levels: The new tax regime may still be advantageous as the impact of lower rates could offset the moderate deductions.

- Higher Income Levels: The old tax regime might be more beneficial as the higher income can push the taxpayer into higher tax brackets, where the deductions in the old regime significantly reduce the taxable income.

Loss from house property has become noteworthy under the default (new) regime!

Clarification on New Tax Regime Effective from April 1, 2024

The Ministry of Finance has issued a press release to address misleading information regarding the new tax regime under section 115BAC(1A), introduced in the Finance Act 2023. The new tax regime under section 115BAC(1A) introduced in the Finance Act 2023 remains the default regime with no changes from April 1, 2024. Taxpayers can opt out of the new regime until filing their return for Assessment Year 2024-25. Flexibility to choose the regime that offers the most tax benefit each financial year. This clarification helps taxpayers understand the stability and options available within the new tax regime framework, allowing for informed tax planning and filing decisions. Here are the key points clarified:

- No New Changes from April 1, 2024: The new tax regime remains unchanged since its introduction on April 1, 2023.

- Default Regime: The new tax regime is the default for persons other than companies and firms from FY 2023-24 (AY 2024-25).

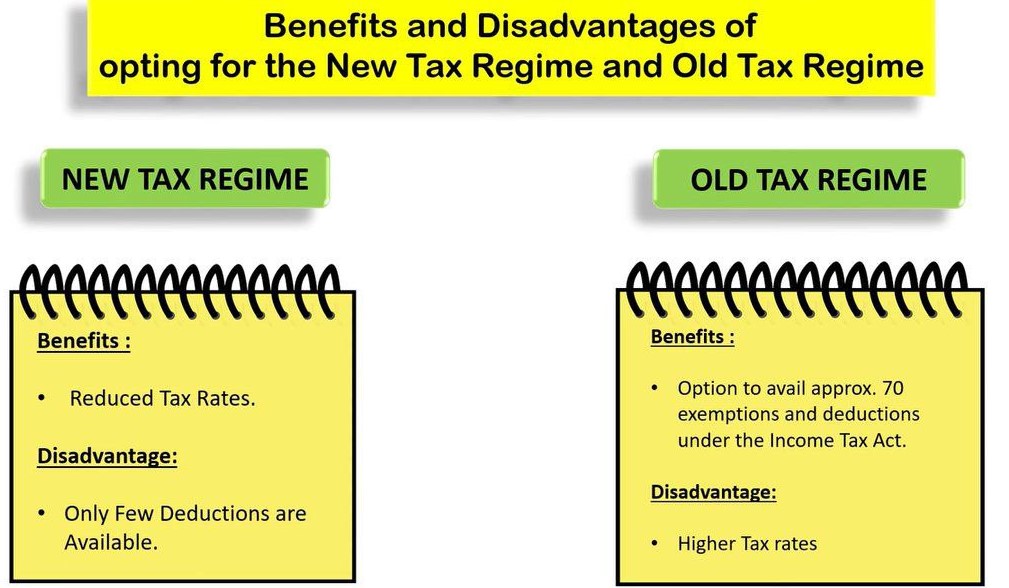

- Lower Tax Rates: Offers significantly lower tax rates compared to the old regime.

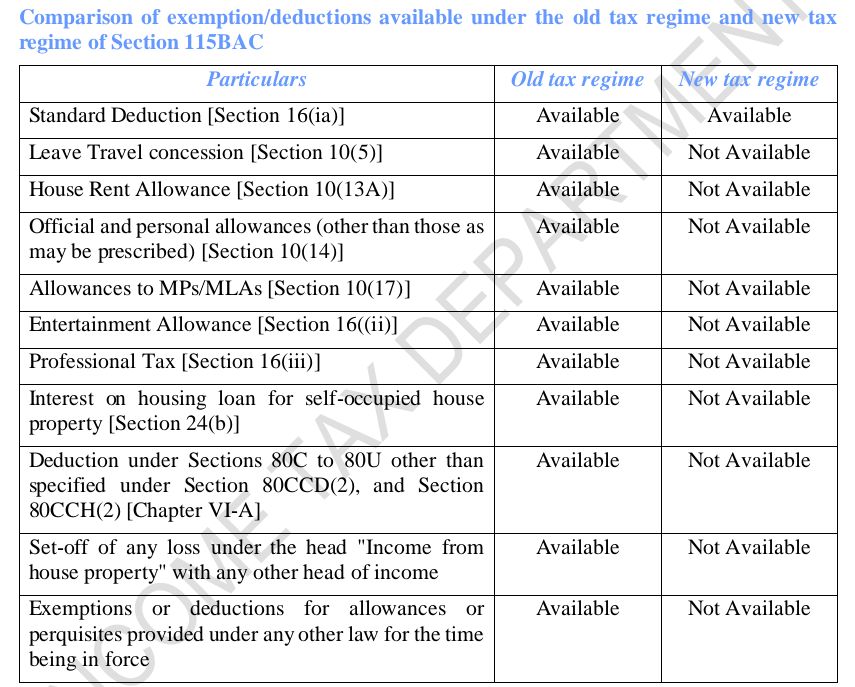

- Limited Exemptions and Deductions: Does not allow various exemptions and deductions available under the old regime, except: Standard deduction of Rs. 50,000 from salary. & Rs. 15,000 from family pension.

- Flexibility for Taxpayers: Taxpayers can choose between the new and old tax regimes based on which benefits them more. Option to opt out of the new regime is available until the filing of the return for AY 2024-25. Eligible persons without business income can choose the regime for each financial year.

- Annual Choice: Income Taxpayers can switch between regimes each financial year: Opt for the new tax regime one year. And Opt for the old tax regime another year.

Default Regime: New Tax Regime

Form 10IEA Filing Rules – For Opting Old Regime

For ITR-1 & ITR-2:

- No need to file Form 10IEA to opt for the Old Regime or switch back to the New Regime.

No restrictions on switching between regimes each year.

For ITR-3 & ITR-4:

- Filing Form 10IEA is mandatory to opt for the Old Regime.

If you later want to return to the New Regime, you must file Form 10IEA again.

Switching is allowed only once — after switching back to New, you can’t go back to Old again.

Only two filings of Form 10IEA are permitted: -

First: To opt for Old Regime

-

Second: To revert to New Regime

Important Caution: Once Form 10IEA is filed, you cannot change your selection for that AY

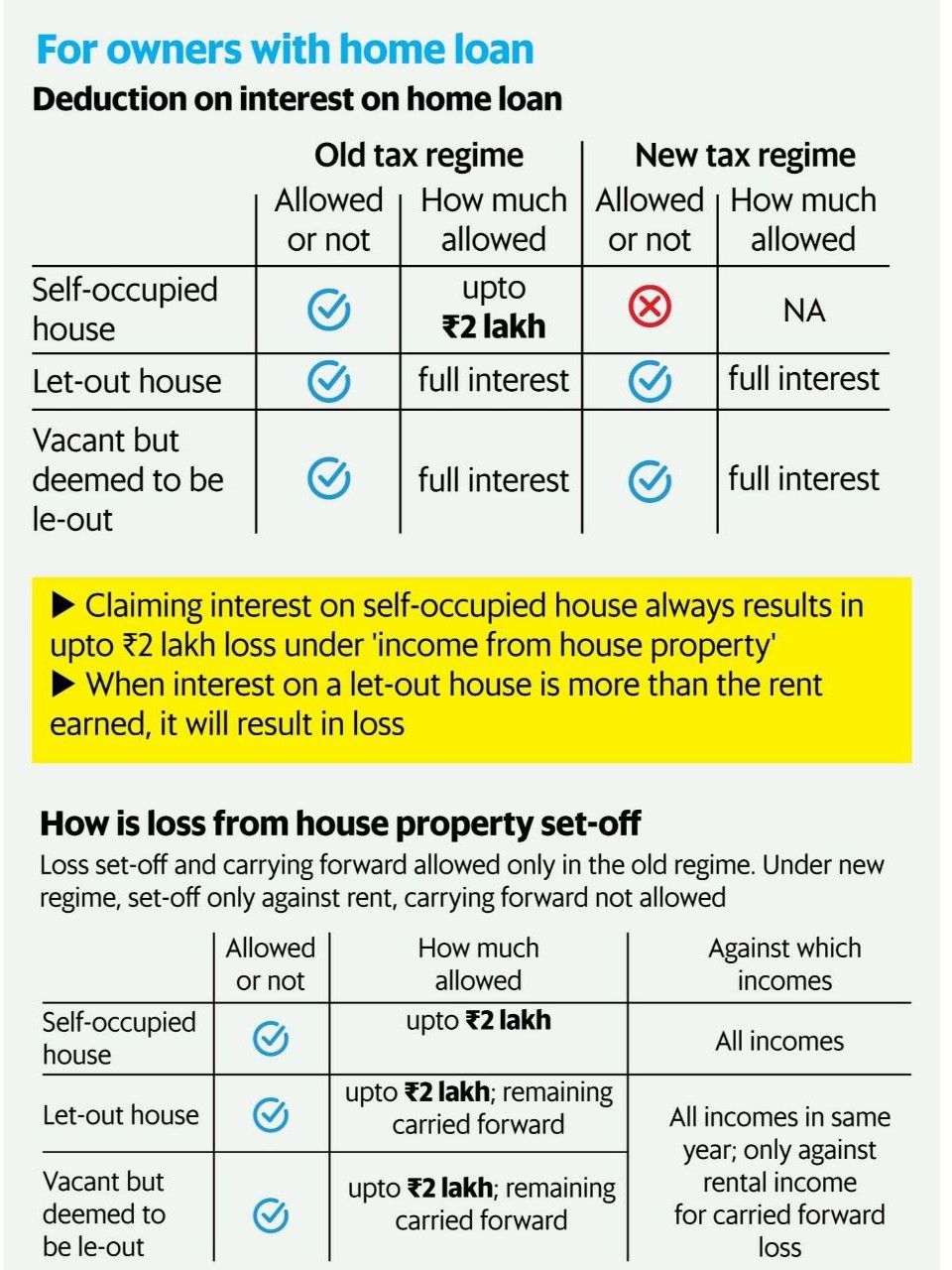

Deduction on Interest on Home Loan

| Type of Property | Old Regime | New Regime |

|---|---|---|

| Self-occupied house | Allowed, up to ₹2 lakh | Not allowed (NA) |

| Let-out house | Allowed, full interest | Allowed, full interest |

| Vacant but deemed to be let-out | Allowed, full interest | Allowed, full interest |

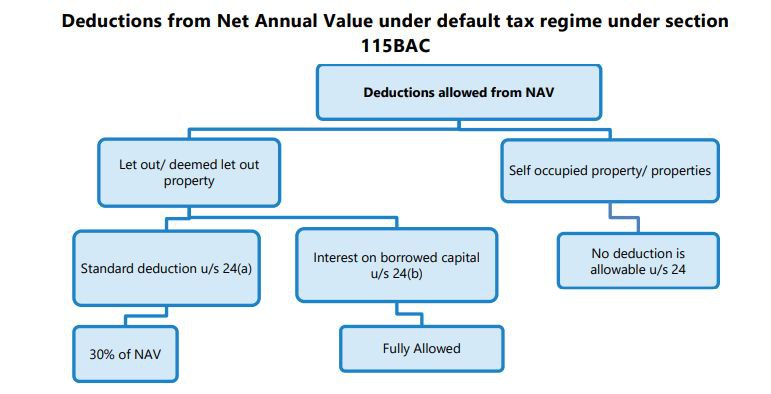

For self-occupied homes, the old regime allows deduction of interest up to INR 2 lakh under Income from House Property. Under the new regime, no deduction is allowed for interest on self-occupied property loans. For let-out or deemed let-out properties, both regimes allow deduction of the entire interest, but with different loss set-off rules.

How Is Loss from House Property Set-Off?

This part is only applicable under the old tax regime. The new regime allows set-off only against rental income, and no carry-forward of loss is permitted.

| Property Type | Allowed | Amount Allowed | Set-Off Against |

|---|---|---|---|

| Self-occupied house | Yes | Up to INR 2 lakh | All types of income |

| Let-out house | Yes | Up to INR 2 lakh; remaining can be carried forward | All incomes in same year; carried forward loss only against rental income |

| Vacant but deemed to be let-out | Yes | Up to INR 2 lakh; remaining can be carried forward | Same as above |

If taxpayer have a self-occupied house loan, opting for the old regime can save you tax via a INR 2 lakh interest deduction.For rented or deemed let-out properties, both regimes allow full interest deduction, but only old regime allows broader set-off and carry forward of losses. Under the new regime, losses can only be set off against rental income and cannot be carried forward.