New Reporting field in Schedule Exempt Income for AY 2026-27

Page Contents

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27

The Income Tax Department has introduced a new reporting field in Schedule EI (Exempt Income) for AY 2026-27

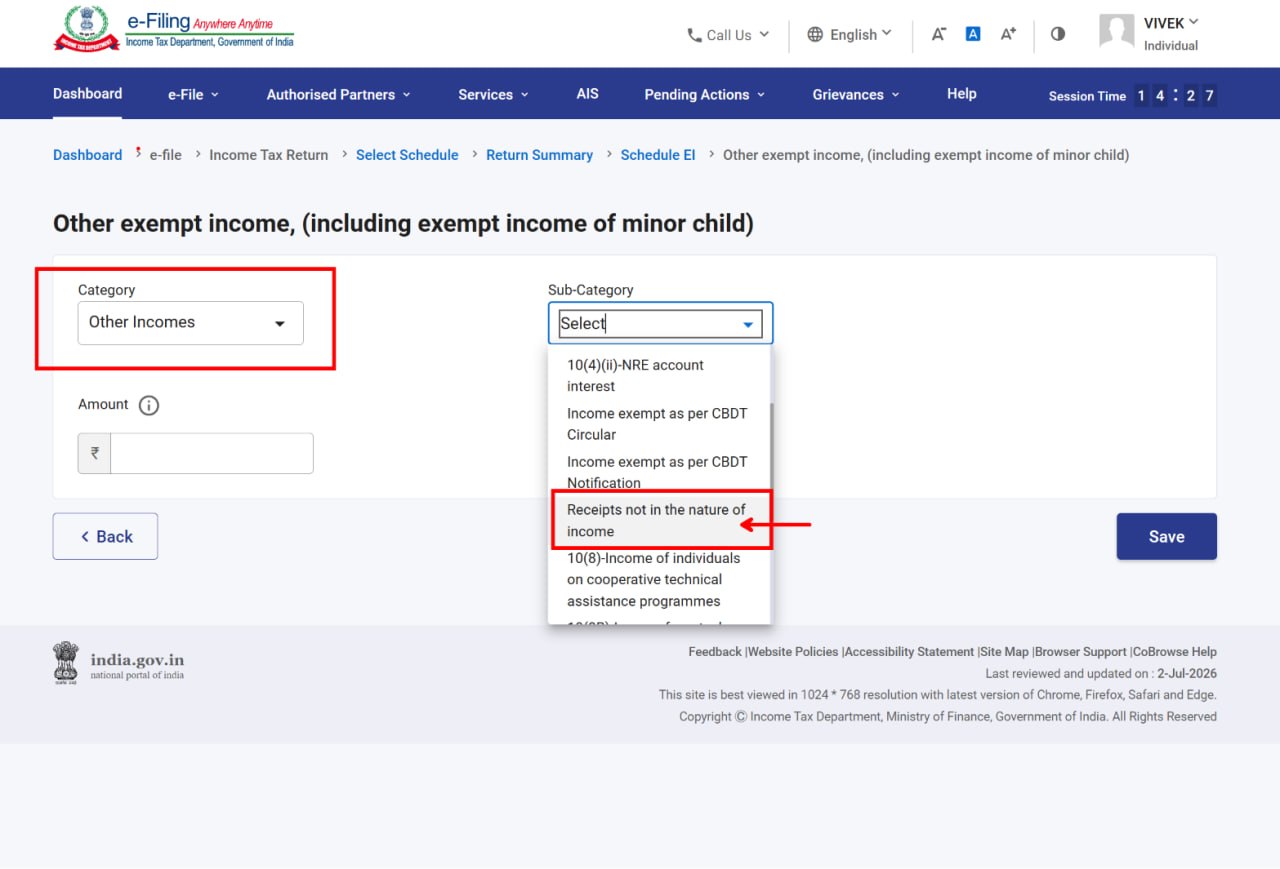

Category: Other Incomes

Sub-category: Receipts not in the nature of income

From the screenshot, this option is now available in the e-filing portal under Schedule EI.

This is primarily a disclosure facility and not a new exemption provision. It allows taxpayers to voluntarily report amounts credited to their bank accounts that are not income at all under the Income-tax Act, thereby helping explain transactions that may otherwise appear in AIS, bank statements, or other information sources.

Examples of receipts that may be reported here

- Gifts from relatives (fully exempt u/s 56)

- Return of capital or personal funds

- Gifts from non-relatives not exceeding INR 50,000 in aggregate

- Lump-sum alimony settlements

- Gifts received on marriage

- Compensation for personal damages

- Reimbursement of expenses

- Other genuine capital/non-income receipts

Taxpayers should not use this field to avoid reporting taxable income. A proper distinction must be maintained:

Exempt Income → Report under the specific applicable head in Schedule EI Examples:

- Agricultural income

- PPF interest

- Sukanya Samriddhi interest

- Dividend exempt under specific provisions

- Share of profit from firm

Taxable Income → Report under the relevant head of income.

- Salary

- House Property

- Capital Gains

- Business/Profession

- Income from Other Sources

Receipts Not in the Nature of Income → Only where the receipt itself does not constitute income under the Act. Practical benefit

Suppose a taxpayer receives a INR 10 lakh gift from father, INR 5 lakh marriage gift, INR 2 lakh reimbursement from employer or friend.

These credits may appear in bank records and could potentially attract future scrutiny. Reporting them under “Receipts not in the nature of income” creates transparency and may help explain such credits if questions arise later.

While this disclosure is useful, it should be used cautiously: “The new reporting field for ‘Receipts not in the nature of income’ is meant for voluntary disclosure of genuine non-income receipts. Exempt incomes should continue to be reported under their respective categories in Schedule EI, and taxable receipts must be offered to tax under the appropriate head of income. Mere disclosure under this new field does not convert a taxable receipt into a non-taxable one.”

This is one of the most significant transparency-oriented changes in AY 2026-27, especially for taxpayers with large gifts, family transfers, reimbursements, and other capital receipts that may otherwise remain unexplained in the tax data ecosystem.