Whether electricity qualify as goods for applying TDS 194Q

Page Contents

Whether electricity qualifies as “goods” for applying TDS under Section 194Q.

Is Electricity “Goods”?

- Electricity is not defined in the Income-tax Act. However, it is treated as goods under the following:

- Sale of Goods Act

- GST Law (movable property)

- Customs Tariff

- Meaning of “Goods”: Not defined in the Income Tax Act. Other laws (Sale of Goods Act, GST, and CST) broadly define goods as movable property, include commodities, and need not be tangible.

- Judicial backing: Electricity is movable, tradable, and consumable. Judicial Position: Supreme Court (NTPC case) held Electricity is “goods.” Even if intangible, it can be transmitted, delivered, and bought & sold. Hence, electricity qualifies as movable property. Electricity can be legally regarded as goods, → 194Q can apply

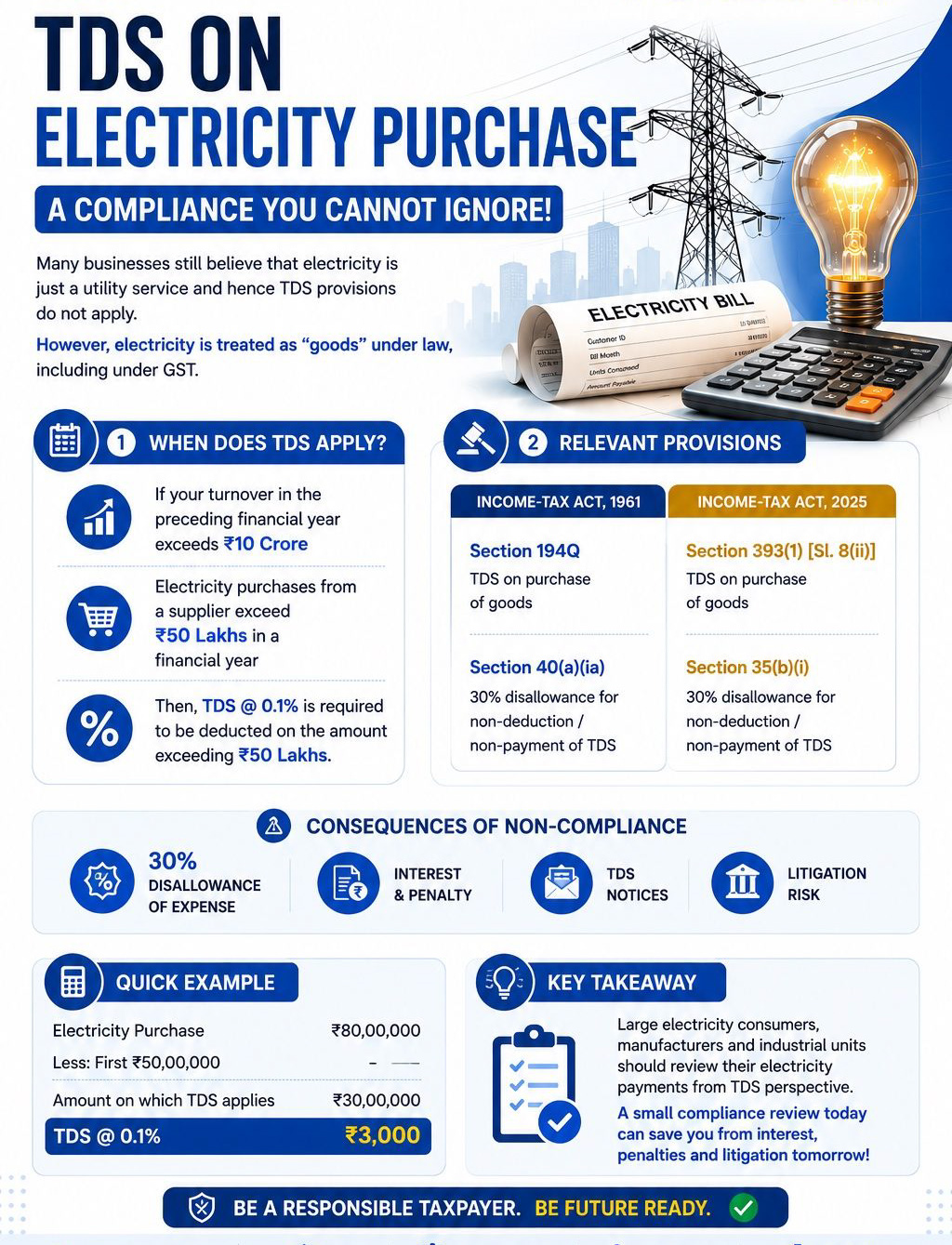

- Core Concept: Section 194Q (effective 1 July 2021) mandates Tax Deducted at Source @0.1% on the purchase of goods. Applies when the buyer’s turnover is > INR 10 crore (previous financial year) and purchases from a seller exceed INR 50 lakh in a financial year.

- Applicability to Electricity Payments: Since electricity = goods, Section 194Q can apply and applies when purchasing electricity from DISCOMs and power generation/distribution companies.

TDS on purchase of goods (Section 194Q) applicability on electricity expenses.

Most businesses treat electricity like a routine expense (similar to rent, internet, etc.). They pay the bill and don’t think about tax deducted at source. But under the Income-tax Act, electricity supplied by a distribution company can be seen as a purchase of goods (not just a service). Why this matters → Section 194Q. . Section 194Q = Tax Deducted at Source on the purchase of goods. This section applies when both conditions are met:

- Tax Deducted at Source 194Q Condition 1: Turnover threshold— Your business turnover in the previous financial year > INR 10 crore

- Condition 2: Purchase threshold: Payments to a single supplier exceed INR 50 lakh in a financial year If both are satisfied, then:

- Tax deducted at source @ 0.1% must be deducted

- On the amount exceeding INR 50 lakh

- Applying this to electricity bills: If electricity is treated as a purchase of goods, then Example: Total electricity payments: INR 80 lakh, Threshold: INR 50 lakh and Tax Deducted at Source applicable on INR 30 lakh. TDS amount = INR 30,000 (0.1%)

- Why businesses miss this because electricity is treated as a utility expense, not “purchase”, Usually no vendor negotiation or contract thinking and automatic payment systems, and then no tax deducted at source. So, compliance is often ignored unintentionally.

Exceptions / non-applicability of Section 194Q on electricity expenses

- Section 196: No tax deducted at source if payment is made to the government, RBI, or certain tax-exempt statutory corporations. However, most electricity companies (PSUs/private) are not fully exempt, so this exemption usually does not apply

CBDT Position (Circular 13/2021)

- Not Applicable: Electricity purchased through power exchanges (IEX, PXIL). Reason: No identifiable seller and automated transactions.

- Applicable : Direct purchase from Power generation companies, DISCOMs / SEBs, and under PPAs / bilateral contracts.

- Central Board of Direct Taxes Circular 13/2021: Section 194Q NOT applicable for electricity traded via power exchanges and transactions in securities/commodities via exchanges. But direct purchases from electricity companies are covered.

- Section 196 Exception: No TDS if payment is made to the government and Certain exempt entities But: Most electricity suppliers are companies (even if govt-owned), and hence, Section 196 is usually NOT applicable.

Practical Applicability Conditions—Applicability of Section 194Q on Electricity Payments

Applicability of Section 194Q on Electricity Payments

TDS under 194Q applies if:

- Buyer turnover > INR 10 crore

- Electricity payments > INR 50 lakh (vendor-wise)

- Purchase is direct (not via exchange)

- Scenario 1 (TDS Applicable) : Turnover: INR 12 crore, Electricity purchase: INR 70 lakh (direct from SEB) then TDS applies on INR 20 lakh, TDS = INR 2,000.

- Scenario 2 (Not Applicable) : Purchase via power exchange (IEX) : No TDS (no identifiable seller)

Risks of non-compliance of electricity are not treated as a purchase of goods.

- Tax Deducted at Source consequences are interest (late deduction/payment), penalty, and possible disallowance proceedings.

- Section 40(a)(ia): Expense may be disallowed in income-tax computation, and This increases taxable profit. For example, electricity expense: INR 80 lakh, then disallowed, then Profit increases by INR 80 lakh. Tax impact can be very large compared to small tax deductions at source.

Before blindly applying 194Q, check: Is electricity really “goods” : Courts/positions are not fully settled universally. Power may sometimes be treated differently.

Overriding sections for electricity expenses as purchase of goods.

- If another Tax Deducted at Source section applies, 194Q may not apply.

- Section 194Q does not apply if Tax Collected at Source under 206C(1H) applies, but utilities usually don’t collect Tax Collected at Source.

A practical checklist for electricity expenses is not treated as a purchase of goods.

Step-1: Threshold check: Turnover > INR 10 crore? And vendor-wise electricity payments > INR 50 lakh?

Step-2: Vendor identification: Same DISCOM? Multiple meters but the same permanent account number?

Step-3: Legal position review: Is your electricity supplier Government-regulated utility and Distribution license holder?

Step-4: Documentation: Permanent account number of electricity provider and invoice structure (goods vs nature of service)

Step-5: Compliance: Deduct Tax Deducted at Source if applicable. Report in the Tax Deducted at Source return (Form 26Q) and reconcile with books and the tax audit.

What looks like a small compliance (0.1% tax deducted at source) can turn into a large tax disallowance risk. Utility expenses are not always “simple” under tax law.

Final Conclusion

- Electricity is legally treated as goods; electricity payments are no longer a routine expense for tax purposes—if procured directly from suppliers, they can trigger Tax Deducted at Source u/s 194Q, making vendor structure and procurement mode critical for compliance.

- Therefore, Tax Deducted at Source u/s 194Q applies on electricity payments if thresholds are met. Therefore, Tax Deducted at Source u/s 194Q will be triggered on the purchase of electricity directly from companies engaged in power generation/distribution. The exception applies only in limited cases (e.g., power exchanges or exempt entities).

- Businesses must not ignore Tax Deducted at Source on electricity just because it’s a utility expense. Direct payments to electricity suppliers can trigger 194Q compliance.

- Electricity = goods in tax law. Section 194Q can apply on electricity payments.

- Key differentiator:

- Direct purchase → TDS applicable

- Exchange purchase → No TDS