CCFS‑2026: Key Benefit, Eligibility & Compliance Implication

Page Contents

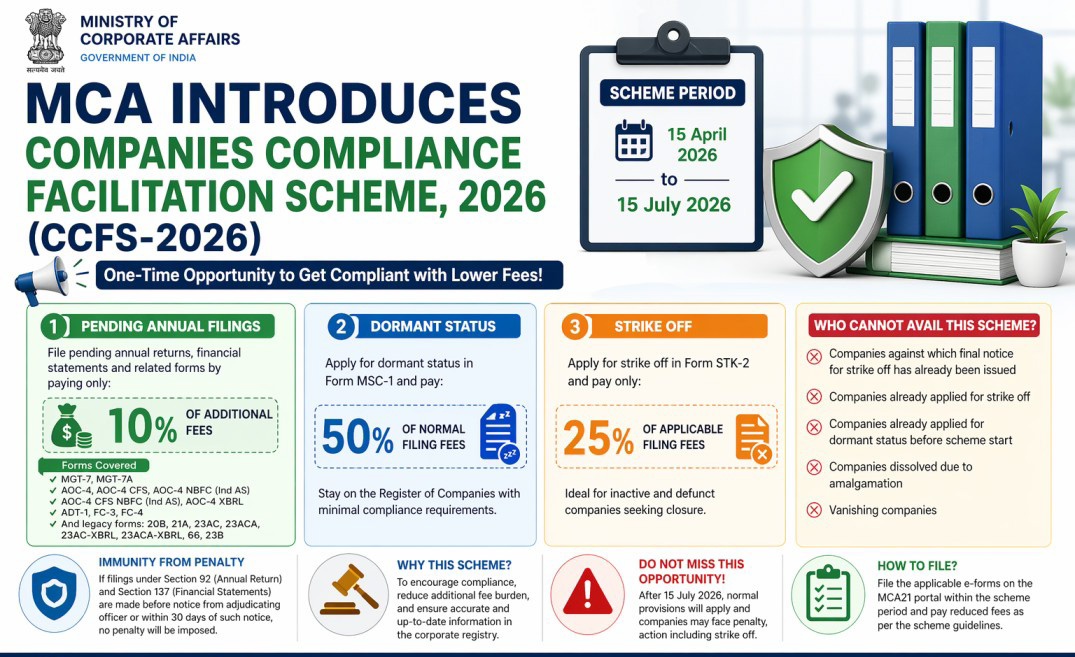

MCA Introduces Companies Compliance Facilitation Scheme, 2026 (CCFS‑2026)

The MCA has introduced the Companies Compliance Facilitation Scheme, 2026 (CCFS‑2026) to provide companies with a one‑time opportunity to regularize pending ROC compliances at substantially reduced cost and with penalty relief in specified cases. On Feb 24, 2026, the MCA issued General Circular No. 01/2026, introducing the Companies Compliance Facilitation Scheme, 2026. The Companies Compliance Facilitation Scheme, 2026, provides a time‑bound compliance window operative from April 15, 2026, to July 15, 2026, enabling companies to regularise delayed statutory filings under the Companies Act, 2013 and the Companies Act, 1956 at substantially reduced additional fees.

This scheme is aimed at encouraging defaulting companies to complete statutory filings and align with regulatory requirements without the burden of heavy additional fees and legal consequences. Effective Period: 15 April 2026 to 15 July 2026

Key Benefits under Companies Compliance Facilitation Scheme, 2026 (CCFS‑2026)

- Overdue ROC Filings at Concessional Cost : File pending annual returns and financial statements by paying only 10% of the applicable additional fees.

- Dormant Status at Reduced Fees : Companies not carrying on business may apply for Dormant Status at 50% of the normal filing fees.

- Strike‑off at Minimal Cost: Inactive companies may opt for strike‑off by paying only 25% of the normal filing fees.

- Penalty Relief : Relief from penalties and prosecution is available in specified cases, subject to compliance with scheme conditions.

- MCA has clarified that the Company Compliance Fresh Start Scheme, 2026 is a one‑time, non‑recurring compliance window introduced with the objective of providing companies an opportunity to regularise past statutory non‑compliances. The scheme is intended to:

- Enable companies to regularise historical non‑compliances under the Companies Act framework

- Facilitate filing of long‑pending statutory documents with the RoC

- Provide significant relief by way of reduced additional fees and mitigation of penal exposure, subject to the conditions of the Scheme

Forms Covered under the Companies Compliance Facilitation Scheme, 2026

The scheme covers major pending ROC filings, including but not limited to MGT‑7 / MGT‑7A – Annual Return, AOC‑4 (including all variants) – Financial Statements, ADT‑1 – Appointment of Auditor, FC Forms – Foreign Company Filings and Other relevant statutory forms as notified. Companies Compliance Facilitation Scheme, 2026, serves as a remedial mechanism rather than a continuing compliance relaxation.

Exclusions – Who Cannot Avail This Scheme?

Lists ineligible entities, including:

- Companies against which final notice for strike‑off has already been issued

- ROC Companies that have already applied for strike‑off

- Companies that have already applied for dormant status before scheme start

- ROC Companies dissolved due to amalgamation

- Vanishing companies

Why Companies Should Act Immediately

Avoid heavy additional fees and penalties. Prevent disqualification of directors, Minimize risk of regulatory action or prosecution. Clean up historical non‑compliances in a cost‑effective manner and Regularize company status for future fundraising, closures, or restructuring

The scheme is time‑bound and will not be extended easily. Early action is strongly recommended. We advise all companies to review their ROC compliance status immediately and take appropriate corrective action well before the closure of the scheme period.

Comparative Fee Structure – Normal Provisions vs CCFS‑2026

the Companies can regularise pending ROC filings by paying only 10% of the applicable additional fees, apply for Dormant Status at 50% of normal filing fees, or opt for Strike‑off at just 25% of filing fees, along with immunity from penalties in eligible cases.

This is a non‑recurring opportunity to clean up historical non‑compliances and avoid substantial additional fees, adjudication proceedings, and regulatory action once the scheme period ends. Early compliance is strongly recommended.

A. Belated Annual Returns & Financial Statements

| Particulars | Normal Provisions (Without Scheme) | Companies Compliance Facilitation Scheme, 2026, |

|---|---|---|

| Applicable forms | MGT‑7 / MGT‑7A, AOC‑4 & all variants, ADT‑1, FC‑3, FC‑4, and 1956 Act forms | Same |

| Normal filing fee | As prescribed under ROFF Rules, 2014 | Same |

| Additional fee for delay | 100% of applicable additional fees (₹ per day / slab-wise, subject to caps) | Only 10% of the applicable additional fees |

| Maximum additional fees | Up to statutory caps (often ₹5–10 lakh depending on form) | Effectively reduced by 90% |

| Eligibility | All companies with belated filings | One-time benefit available only during scheme period |

| Financial impact | High cost; often prohibitive | Significant cost savings |

B. Dormant Status Option (Section 455)

| Particulars | Normal Provisions | Companies Compliance Facilitation Scheme, 2026, |

|---|---|---|

| Applicable form | MSC‑1 | MSC‑1 |

| Filing fees | 100% of normal prescribed fees | 50% of prescribed filing fees |

| Additional fee | Not applicable | Not applicable |

| Eligibility | Company inactive for 2 preceding FYs | Same |

| Benefit | No concession | 50% fee reduction |

C. Strike‑off Option (Section 248)

| Particulars | Normal Provisions | Companies Compliance Facilitation Scheme, 2026, |

|---|---|---|

| Applicable form | STK‑2 | STK‑2 |

| Filing fees | 100% of prescribed fees | 25% of prescribed fees |

| Additional fee | Not applicable | Not applicable |

| Eligibility | As per Section 248 | Same |

| Benefit | Full cost payable | 75% fee savings |

Snapshot Comparison – Financial Impact

| Compliance Route | Normal Cost Exposure | Cost under Companies Compliance Facilitation Scheme, 2026, |

|---|---|---|

| Delayed annual filings | Very high (additional fees accumulate daily) | Only 10% of additional fees |

| Dormant status | Full filing fees | 50% of filing fees |

| Strike‑off | Company Full filing fees | 25% of filing fees |

| Overall impact | High financial and regulatory burden | Substantial relief + compliance cleanup |

Risks of Non‑Availing Companies’ Compliance Facilitation Scheme, 2026

Companies that do not utilize the scheme within the prescribed timeline may be exposed to the following risks:

- Substantially higher additional filing fees under the standard provisions of the Companies Act and allied rules

- Penal consequences for continuing default, including levy of penalties on the company and its officers

- Adjudication proceedings and potential prosecution initiated by the RoC

- Heightened regulatory scrutiny, resulting in increased compliance burden and reputational impact

How Rajput Jain & Associates Can Assist in this Scheme

Our team at Rajput Jain & Associates will be pleased to identify pending ROC compliances and compute eligible benefits under the Companies Compliance Facilitation Scheme, 2026. Handle end‑to‑end filing and documentation, advise on dormant status or strike‑off options, and ensure smooth and timely completion within the scheme window. For assistance, please contact our team at RJA.