GST Implications on Sale of Used Assets

Page Contents

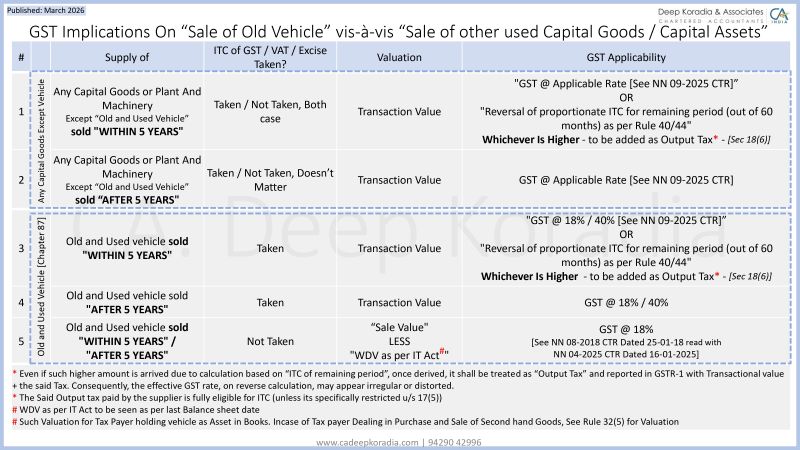

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods

Some Tamil Nadu AAR judgments that a business must pay Goods and Services Tax on the entire transaction value while selling an outdated car have sparked a lot of debate. This interpretation, in my opinion, is inaccurate and lacking, especially when read in isolation and without reference to Notification No. 08/2018–Central Tax (Rate), as amended. The Products and Services Sale of other used capital items (not vehicles) and the sale of old or used cars are both subject to tax treatment. differs significantly, and each must be examined separately.

Sale of Old / Used Motor Vehicles

Statutory Framework : A particular valuation method for the supply of old and used cars, including those used for commercial purposes, is provided by Notification No. 08/2018–CT (Rate) (as updated periodically). The notification is applicable not only to dealers but also to individuals who sell used cars that are part of their company’s assets.

Valuation Mechanism – Key Relief. Goods and Services Tax is payable only on the MARGIN, not on the gross selling price. Margin = Selling Price – Depreciated Value

- Depreciation is to be computed as per the Income‑Tax Act, wherever applicable.

- If the margin is negative, it shall be ignored (deemed as NIL).

- Hence, no Goods and Services Tax is payable where the selling price is lower than WDV.

This benefit applies even where input tax credit was availed at the time of purchase (unlike Rule 44 reversals, which do not apply here due to the special notification).

Applicable Goods and Services Tax Rate

| Type of Vehicle | Goods and Services Tax Rate (on margin) |

| Old petrol / diesel / LPG vehicles | 18% |

| Old EVs | 5% |

(Compensation cess is not applicable on sale of used vehicles)

Authority for Advance Rulings – The Reasons for Reliance’s Misplacement According to certain Tamil Nadu AAR rulings, the entire transaction value of an old car sale is subject to the Goods and Services Tax. However, the applicant alone is bound by the Authority for Advance Ruling. Notification 08/2018 was not sufficiently contested in a number of instances. Facts included non-commercial intent, employee recoveries, or one-time disposals. Beneficial announcements cannot be disregarded in value, according to court rulings and appellate authority. As a result, the notification’s explicit margin-based valuation cannot be overridden by the Authority for Advance Ruling. Following are Practical Correct Position

- Sale of old motor vehicles, even when part of business assets, does NOT attract Goods and Services Tax on full sale value

- Goods and Services Tax is payable only on positive margin, subject to conditions of Notification 08/2018

Sale of Other Used Capital Goods (Other Than Vehicles)

No Special Valuation Notification: Unlike motor vehicles, no specific exemption or margin‑based valuation notification exists for other used capital goods such as Machinery, Furniture, Equipment, Computers and Plant & machinery (non‑vehicle). Therefore, general Goods and Services Tax provisions apply.

Taxability & Valuation

- Sale of used capital goods qualifies as “supply” under Section 7 Central Goods and Services Tax Act, 2017

- Goods and Services Tax is payable on the full transaction value

- Value to be determined u/s 15 of Central Goods and Services Tax Act, 2017

Rate of Tax : Goods and Services Tax rate shall be the rate applicable to such goods at the time of supply and No special concession rate or margin mechanism is available

ITC Reversal: Rule 44 / Section 18(6) applies and Tax payable shall be higher of ITC reduced by prescribed percentage (5% per quarter), or Tax on transaction value

Comparative Summary on GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods

| Particulars | Old Motor Vehicles | Other Used Capital Goods |

| Special Notification | Yes (08/2018–CTR) | No |

| GST on Full Value | No | Yes |

| GST on Margin | Yes | No |

| Negative Margin | Ignored (NIL GST) | Not relevant |

| ITC Reversal Mechanism | Not required if margin scheme applied | Mandatory (Rule 44) |

GST treatment depends on just 3 factors:

- Nature of asset (vehicle vs other capital goods)

- Whether ITC was availed

- Period of use (before or after 5 years)

Capital Goods (Other than Vehicles)

- Within 5 years then GST = Higher of: GST on sale value and ITC attributable to remaining life

- After 5 years ITC = Nil then GST only on transaction value

- No margin scheme then Full value taxation applies

Old & Used Vehicles (ITC Availed)

- Within 5 years, then GST = the higher of GST on sale value and remaining ITC.

- After 5 years GST on transaction value But here’s the twist Margin scheme may still be explored strategically (often ignored in practice)

Old Vehicles (ITC NOT Availed) – The Most Misunderstood Rule. This is where 90% of mistakes happen. Applicable: Margin Scheme

- Value = Sale Price – WDV (as per Income Tax Act)

- If profit → GST applies. If loss → NO GST

- Applies even if You are NOT a car dealer; the vehicle is a business asset and Sold after years of use

Summary GST on Sale of Used Assets

The prevailing fear that sale of old vehicles attracts GST on full transaction value is misplaced.

- Vehicles → Always evaluate margin scheme

- Capital goods → Section 18(6) is mandatory

- Planning opportunity exists in asset disposal

- Documentation of method adopted is critical

Notification No. 08/2018–CTR explicitly grants relief, even where vehicles are part of business assets and ITC was availed. However, this relief is limited only to motor vehicles. For all other used capital goods, GST continues to be payable on full transaction value, subject to ITC reversal provisions. Important Reality Check on GST on Sale of Used Assets

- GST on full sale value of old car → Not always correct. Blind reliance on AAR rulings → Risky

- Notifications still prevail, and the margin scheme is legally valid and powerful

- Full value taxation is NOT the default rule for used vehicles and Margin-based taxation is often the correct and tax-efficient approach