Overview on Golden Rules Of Accounting

Page Contents

Overview on Golden Rules Of Accounting — Made Simple!

Golden Rules of Accounting

These rules guide which account to debit and credit, based on the account type:

| Account Type | Rule | Example |

|---|---|---|

| Personal | Debit the Receiver, Credit the Giver | Paid ₹5,000 to supplier → Dr Supplier, Cr Cash |

| Real | Debit What Comes In, Credit What Goes Out | Bought furniture for cash → Dr Furniture, Cr Cash |

| Nominal | Debit All Expenses & Losses, Credit All Incomes & Gains | Paid salary → Dr Salary, Cr Cash |

- Personal = People (Debtors & Creditors)

- Real = Things (Assets)

- Nominal = Results (Expenses & Incomes)

The foundation of double-entry bookkeeping

Personal Account

Rule : Debit the Receiver, Credit the Giver

Think : People, firms, organizations

Example: Paid cash to Mr. A

- Debit: Mr. A’s Account (Receiver)

- Credit: Cash Account (Giver)

Real Account

Rule : Debit What Comes In, Credit What Goes Out

Think : Assets (Tangible & Intangible)

Example: Bought furniture for cash

- Debit: Furniture Account (Comes In)

- Credit: Cash Account (Goes Out)

Nominal Account

Rule → Debit All Expenses & Losses, Credit All Incomes & Gains

Think → Profit & Loss items

Example: Paid salary

- Debit: Salary Account (Expense)

- Credit: Cash Account (Payment)

The foundation of double-entry bookkeeping rests on a simple but powerful idea Every financial transaction has two equal and opposite effects, recorded as a debit in one account and a credit in another. This ensures the accounting equation always stays in balance:

Assets=Liabilities+Capital\text{Assets} = \text{Liabilities} + \text{Capital}

Core Principles

- Dual Aspect Concept : Every transaction affects at least two accounts. One account is debited, the other is credited for the same amount. & This keeps total debits = total credits.

- The Ledger & Trial Balance : Transactions are first recorded in the journal (chronological order). Then posted to ledger accounts (by account type). A trial balance checks that total debits equal total credits.

- Why It Works : Ensures accuracy and completeness. Provides a full picture of both sides of a transaction. & Forms the basis for preparing financial statements (P&L, Balance Sheet).

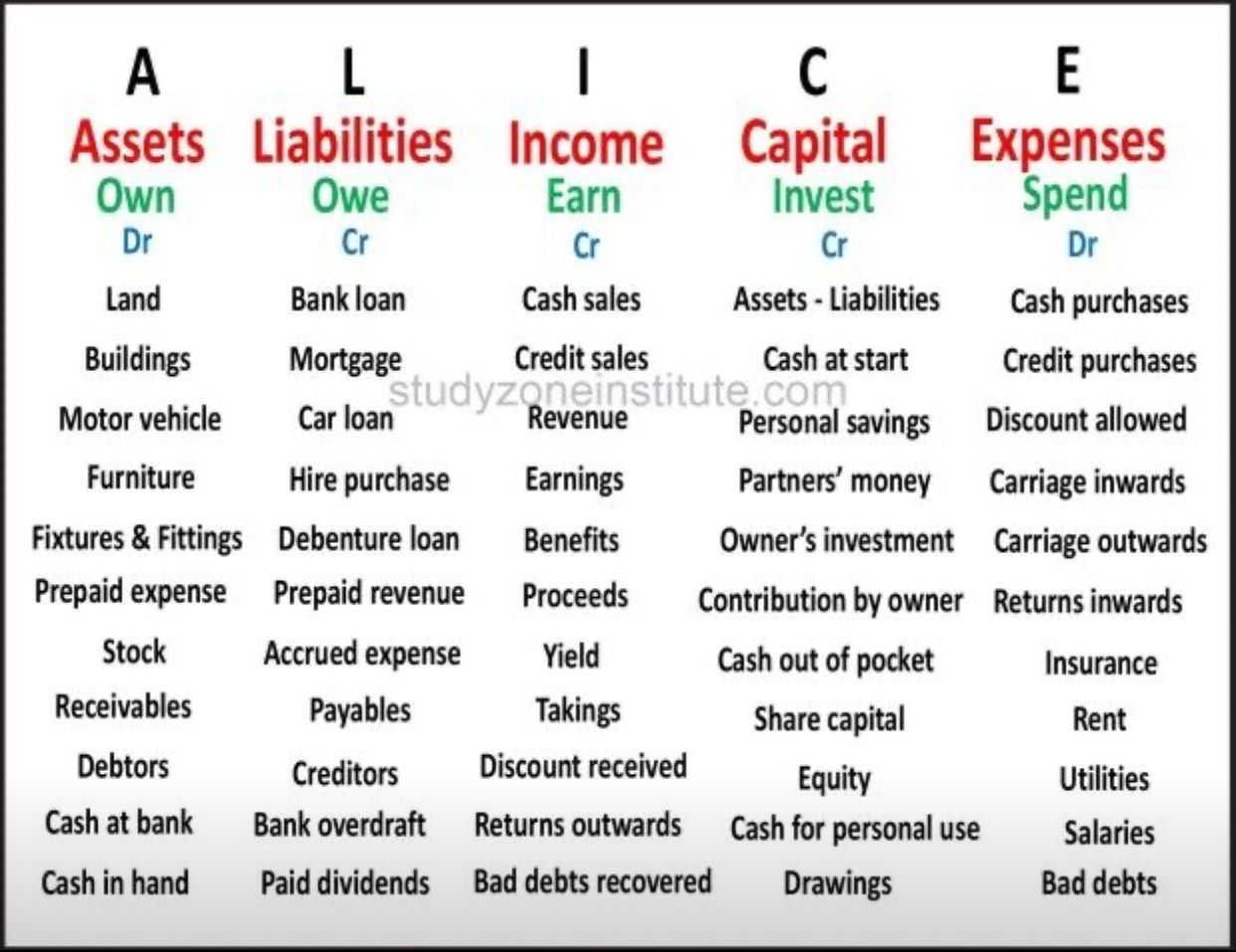

A Guide to A.L.I.C.E.- Understanding the Accounting Categories

The A.L.I.C.E. acronym is a helpful tool for categorizing the fundamental components of accounting: Assets, Liabilities, Income, Capital, and Expenses. Each element plays a vital role in understanding financial statements and maintaining balance in accounting.

- Assets (A) : What the business owns.

- Liabilities (L) : What the business owes.

- Income (I) : What the business earns.

- Capital (C) : What the owners invest.

- Expenses (E) : What the business spends.

From a double-entry perspective, it also instantly reminds you of the normal balance for each category. It also shows which side they appear on in double-entry bookkeeping:

- Debit (Dr) : Assets, Expenses

- Credit (Cr) : Liabilities, Income, Capital

Money Flow Basics

Every transaction affects at least two categories of A.L.I.C.E., keeping the accounting equation balanced

Assets=Liabilities+Capital+(Income−Expenses)Assets = Liabilities + Capital + (Income – Expenses)Assets=Liabilities+Capital+(Income−Expenses)

Examples of Real-World Movements

| Transaction | Effect on A.L.I.C.E. | Flow Explanation |

| Owner invests INR1,00,000 | +Asset (Cash) / +Capital | Cash increases (A), owner’s equity increases (C). |

| Take a bank loan of INR50,000 | +Asset (Cash) / +Liability (Loan) | More cash in the bank (A) but you owe the bank (L). |

| Buy furniture for INR20,000 cash | -Asset (Cash) / +Asset (Furniture) | Cash (A) decreases, furniture (A) increases — just swapping asset types. |

| Sell goods for INR5,000 cash | +Asset (Cash) / +Income (Sales) | More cash (A) and you earned revenue (I). |

| Sell goods on credit for INR3,000 | +Asset (Debtors) / +Income (Sales) | You have receivables (A) and revenue (I). |

| Pay rent INR2,000 in cash | -Asset (Cash) / +Expense (Rent) | Cash (A) decreases, rent expense (E) increases. |

| Pay INR500 towards loan repayment | -Asset (Cash) / -Liability (Loan) | Cash (A) decreases, loan liability (L) decreases. |

| Owner withdraws INR1,000 for personal use | -Asset (Cash) / -Capital | Cash (A) decreases, owner’s equity (C) decreases. |

Money Flow Pattern

If we visualize it:

- Assets ↔ Liabilities → Borrowing & repayments

- Assets ↔ Capital → Owner’s investments & drawings

- Assets ↔ Income → Sales & collections

- Assets ↔ Expenses → Payments for goods/services

- Income → Capital → Profits retained in business

- Expenses reduce Capital (via profit reduction)

Details are mention here under :

-

A – Assets (Own, Debit)

Things the business owns that have value — They provide future economic benefits and can include land, buildings, vehicles, furniture, prepaid expenses, stock, receivables, debtors, cash. Assets are everything a company owns. – Land. Each asset type can either be tangible or intangible and must always be recorded on the balance sheet.

-

L – Liabilities (Owe, Credit)

Liabilities represent obligations that a company owes to outside parties. Obligations the business must pay . They signify what needs to be paid in the future, including loans, mortgages, hire purchase, debentures, accrued expenses, payables, overdrafts.

-

I – Income (Earn, Credit)

Money the business earns — e.g., sales, revenue, earnings, benefits, proceeds, yield, takings, discounts received, returns outwards, bad debts recovered. Income refers to the revenue earned by a company from its business operations and can come from Cash Sales, Credit Sales, Earnings, Interest, Benefits, Investment Returns. The income generated is essential for growth and sustainability, impacting the overall profitability of the business.

-

C – Capital (Invest, Credit)

Owner’s equity or investment — e.g., starting capital, savings, partners’ contributions, share capital, equity, drawings. Capital represents funds contributed by the owners or shareholders to start and grow the business. It includes – Owner’s Investment, Share Capital, Personal Savings, Partners’ Money, Capital is critical because it builds the foundation for growth and investment in assets.

-

E – Expenses (Spend, Debit)

Costs the business incurs — e.g., purchases, discounts allowed, carriage, returns inwards, insurance, rent, utilities, salaries, bad debts. Expenses are costs incurred by a business in its operations, which diminish the income. They include Cash Purchases, Credit Purchases, Salaries and Wages, Insurance, Rent, Utility Bills. Monitoring expenses is vital for maintaining profitability and managing cash flow effectively.

Accruals vs. Provisions — The Key Differences

Accruals: “We owe it / are owed it — just not paid yet.” – Certain.

Provisions : “We might owe it — better set aside something.” – Uncertain.

Both ensure financial statements reflect reality — but they do it for different reasons.

| Aspect | Accruals | Provisions |

| Definition | Expenses or income that are certain, but not yet paid/received by period-end. | Amounts set aside for probable future losses or obligations with uncertain amount/timing. |

| Certainty | High — obligation exists and amount is known or measurable. | Low to Medium — obligation is probable but amount/timing is estimated. |

| Purpose | To match income/expenses to the correct accounting period (accrual concept). | To anticipate and account for expected losses (prudence concept). |

| Examples | Unpaid salaries, electricity bill, accrued interest income. | Provision for bad debts, legal claims, product warranties. |

| Balance Sheet Impact | Creates a liability (e.g., Accrued Expenses) or asset (e.g., Accrued Income). | Creates a liability or a contra-asset (e.g., Provision for Doubtful Debts). |

| Reversal | Typically reversed in the next period when payment is made or income received. | Carried forward and adjusted as more information becomes available. |

| Accounting Standards | Required under accrual basis per IFRS/GAAP. | Governed by IAS 37 / AS 29 (Provisions, Contingent Liabilities & Contingent Assets). |

Debit Note vs. Credit Note — The Key Differences

- Debit Note : Buyer Debits Seller’s account (from buyer’s perspective)

- Credit Note : Seller Credits Buyer’s account (from seller’s perspective)

| Aspect | Debit Note | Credit Note |

| Who Issues It? | Buyer (to supplier/vendor) | Seller (to buyer/customer) |

| Purpose | To request a reduction in the payable amount — due to reasons like damaged goods, short supply, overcharging. | To confirm and acknowledge the reduction in receivable amount as per the buyer’s request or agreed terms. |

| Accounting Impact (Issuer’s Books) | Increases accounts receivable from seller / decreases accounts payable to seller. | Decreases accounts receivable from customer / increases accounts payable to customer. |

| Typical Reasons | – Goods returned by buyer – Overbilling – Defective goods |

– Acceptance of goods return – Correction of overbilling – Post-sale discounts |

| Document Flow | Buyer sends to seller as a claim for adjustment. | Seller sends to buyer to officially grant the adjustment. |

| Example | Buyer receives damaged products worth ₹5,000 and issues a debit note to reduce payment. | Seller accepts the debit note and issues a credit note confirming ₹5,000 reduction. |

Understanding about Every accountant is an auditor, however every auditor is not an accountant

Why every accountant can be an auditor

- Accounting training covers auditing basics : Accountants are skilled in recording, classifying, and summarizing transactions, but also learn to review and verify records.

- Built-in review role: Many accountants check ledgers, reconcile accounts, and verify documentation activities that overlap with audit work.

- Qualification overlap : In many jurisdictions, professional accounting qualifications (CA, CPA, ACCA) include auditing as a core competency.

Why every auditor is not necessarily an accountant

- Specialized audit fields : Some auditors focus on non-financial areas (e.g., IT audits, operational audits, compliance audits).

- Different skill sets : An IT auditor may assess cybersecurity controls, or a compliance auditor may check regulatory adherence — without preparing or maintaining accounts.

- Entry from other disciplines : Auditors may come from law, engineering, information systems, or risk management backgrounds.

The takeaway

- Accountants : Broad financial expertise, can perform audits if required.

- Auditors : Focused on examination, may not handle accounting functions.

- Relationship : All accountants have the potential to audit; not all auditors are trained accountants.

Final Adjustments in Financial Accounting

Conclusion

Because every transaction affects at least two of these categories, remembering A.L.I.C.E. helps ensure that the books always stay balanced. Using the A.L.I.C.E. framework allows both students and practitioners in accounting to better understand the core elements of financial statements. Keeping these categories in mind aids in recognizing their interconnectedness and the importance of maintaining the balance that defines the accounting equation.