Late Fee & last date to File updated ITR Return

Page Contents

NEW UPDATE FOR FY 2022-23 – New ITR forms for AY 2023-24

ITR forms 1-6, ITR-V (verification form), and ITR acknowledgment form are made public For AY 2023–24. For the FY 2022–2023, if you got any income from cryptocurrencies or other digital assets, You must do so using a unique schedule found in the new ITR forms FY 2022–2023.

Different kind of Income Tax Return forms are available for income tax filing, depending on the income tax taxpayer’s income & source of income. For instance,

- Income Tax Return-ITR Form 1 is applied to individuals income up to INR 50,00,000/- from sources such as salary, 1 residential property, or Income from other sources.

- The Income Tax Return-ITR-2 is applied to individuals earning over INR 50,00,000/- with income from House Property.

- Income Tax Return-ITR-3 is applied to individuals with professional or business income.

- The Income Tax Return-ITR Form 4 is a easy form designed for freelancers. Or MSME taxpayers.

- Income Tax Return- ITR-5 is for partnership firm or LLPs businesses.

- The Income Tax Return- ITR-6 is for companies if they are not claiming exemption U/s 11.

- Income Tax Return- ITR-7 is for political parties, trust & other assessee not eligible to file any of the above Income tax return form.

- The tax Dept had notified the launch Income Tax Return returns for ease and accuracy of filing. To facilitate this process, authorizing various entities to report such transactions to the Tax Dept. These specified entities will be responsible for providing the details of capital gains transactions, dividends, and interest income of the taxpayers.

- Taxpayers need to keep in mind high-value transactions they made while filing their Income Tax Return. The tax Dept is using analytics to scrutinize data to find out people who have not filed ITR or under-reported income despite doing a high-value transaction.

What is section 234F in the language of the law:

In Budget our honorable Finance Minister, introduced a new section 234F to ensure timely filing of returns of income. As per section 234F of the Income Tax Act, if a person is required to file Income Tax Return (ITR forms) as per the provisions of Income Tax Law [section 139(1)] but does not file it within the prescribed time limit then late fees have to be deposited by him while filing his ITR form. The quantum of fees shall depend upon the time of filing the return and total income.

Without prejudice to the provisions of this Act, where a person required to furnish a return of income under section 139, fails to do so within the time prescribed in sub-section (1) of said section, he shall pay, by way of fee, a sum of

- 5 thousand rupees, if the return is furnished on or before the 31st day of December of the assessment year;

- 10 thousand rupees in any other case:

Provided that if the total income does not exceed five lakh rupees, the fee payable shall not exceed one thousand rupees.

The provisions of this section shall apply in respect of the return of income required to be furnished for the assessment year commencing on or after the 1st day of April 2018.

Updated Return (ITR-U) under Section 139(8A): Major Changes by Finance Acts 2025 & 2026

- The Updated Return (ITR-U) was introduced by the Finance Act, 2022 through Section 139(8A) as a voluntary compliance mechanism. It allows taxpayers to disclose income that was omitted from the original, belated, or revised return even after normal return correction timelines have expired. The philosophy behind ITR-U is simple “Declare missed income voluntarily, pay additional tax, and avoid future litigation.” However, ITR-U is designed as a revenue-generating provision, not a tax-saving provision.

Basic Features of Updated Return

- A taxpayer can file an Updated Return to Report omitted income, Correct under-reporting of income, Correct wrong claims, disclose forgotten transactions and Increase tax liability voluntarily. However, ITR-U cannot be used To claim a refund, To reduce tax liability, To convert a profit into a loss, To increase a loss and to increase a refund amount. Thus, the Government allows correction only where the correction results in higher tax collection.

Finance Act 2025 – Major Expansion of ITR-U

- Time Limit Extended from 24 Months to 48 Months

- Earlier, an updated return could be filed within 24 months from the end of the relevant assessment year. However, the Finance Act 2025 has doubled the window.

- New Time Limit : An updated return can now be filed within 48 months from the end of the relevant assessment year. This provides taxpayers a significantly longer opportunity to voluntarily regularise past tax issues.

- New Additional Tax Structure

- The government has retained the concept of paying an additional income-tax over and above normal tax and interest. However, the extended filing window now comes with progressively higher costs. Additional Tax Payable under Section 140B

| Period of Filing ITR-U | Additional Tax |

| Within 12 months | 25% |

| More than 12 months up to 24 months | 50% |

| More than 24 months up to 36 months | 60% |

| More than 36 months up to 48 months | 70% |

The percentage is calculated on Tax + Interest payable. The delay becomes increasingly expensive.

Intent Behind Higher Additional Tax

- The Government wants Early voluntary disclosure, Reduced tax litigation, Faster collection of revenue and Discouragement of strategic delay. The message is clear that The longer a taxpayer waits, the more expensive the correction becomes.

Finance Act 2026 – Significant Relief Linked to Reassessment Proceedings

- Finance Act 2026 introduced important amendments effective from 1 March 2026. These amendments deal with the interaction between Section 139(8A) (ITR-U), Section 148A (Enquiry before reassessment) and Section 148 (Reassessment notice).

Why Was This Amendment Needed?

- Earlier many taxpayers feared Updated Return may increase disclosure, Department may still reopen the case, Penalty proceedings may still be initiated and This reduced the attractiveness of voluntary compliance. Finance Act 2026 attempts to address this concern.

Penalty Protection under Section 270A(11A)

- One of the most important changes is the introduction of protection from penalty. Where Income is disclosed through a qualifying Section 148-linked Updated Return and Enhanced additional tax is paid Then Such disclosed income shall not form the basis for penalty under Section 270A.

Why Is This Important?

- Section 270A contains penalties for underreporting of income; then the penalty is 50% of tax payable

- Misreporting of income, then Penalty will be 200% of tax payable. These are severe penalties.

Benefit of New Amendment

- If the taxpayer chooses the prescribed route and Files the Section 148-related updated return, declares the income, Pays tax, Pays interest, and pays applicable additional tax, then there is no Section 270A penalty on that income. This creates a strong incentive for voluntary disclosure.

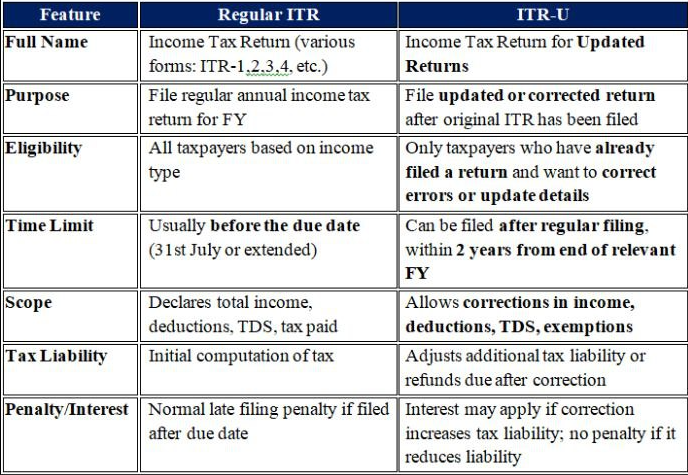

Regular ITR vs. ITR-U (Updated Return)

| Feature | Regular ITR | ITR-U (Updated Return) |

|---|---|---|

| Full Name | Income Tax Return (ITR-1, 2, 3, 4, etc.) | Income Tax Return for Updated Returns |

| Purpose | File regular annual income tax return | File updated/corrected return after original ITR |

| Eligibility | All taxpayers based on income type | Only those who have already filed a return |

| Time Limit | Before due date (usually 31st July) | Within 2 years from end of relevant FY |

| Scope | Declare income, deductions, TDS, tax paid | Correct income, deductions, TDS, exemptions |

| Tax Liability | Initial computation of tax | Adjusts tax/refund based on corrections |

| Penalty/Interest | Late filing penalty if delayed | Interest may apply if tax increases; no penalty if refund increases |

- Use Regular ITR for timely, accurate filing.

- Use ITR-U if you missed reporting income, deductions, or made errors in your original return.

Fees of late filing of ITR

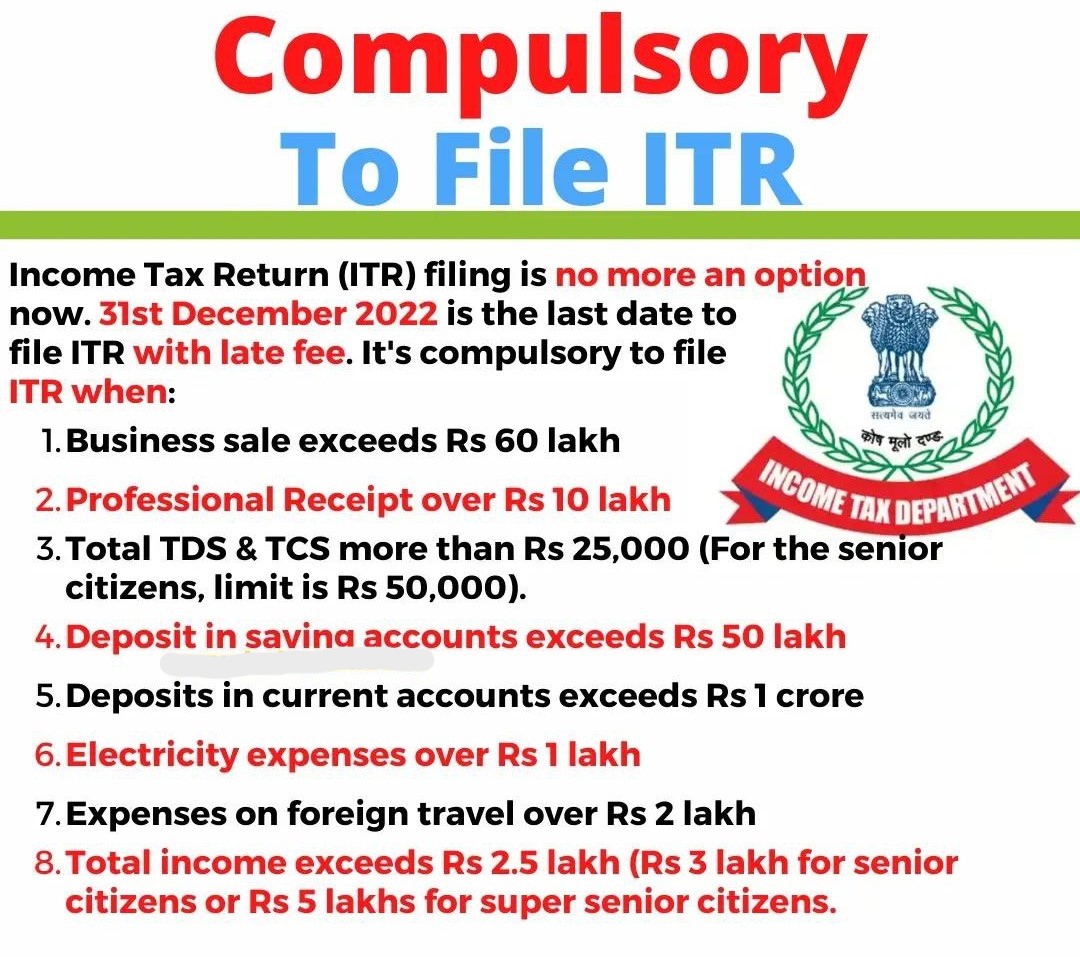

If ITR for AY is filed after the due date but before 31st Dec of the Assessment year then fees of Rs.5000/- will be levied and If ITR is filed after 31st Dec, then Rs. 10000 will be levied as extra fees.

There is one exception that if your total income is below or equal to Rs. 5 lakhs then the maximum penalty is Rs. 1000.

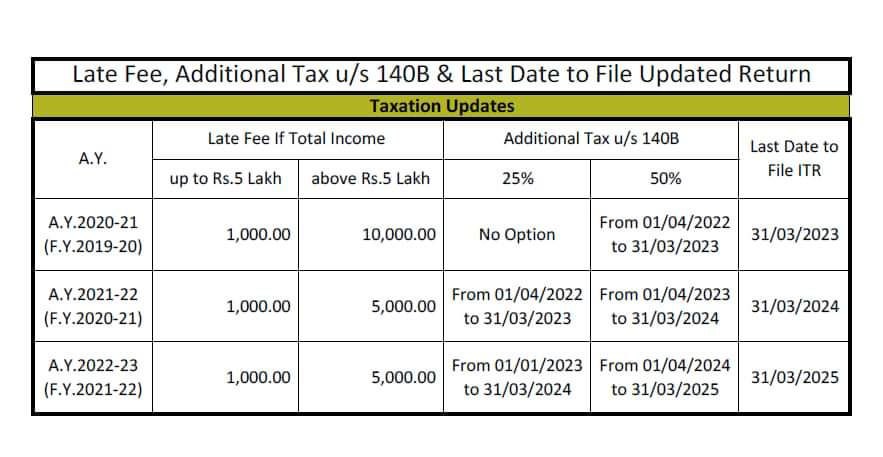

Additional Tax u/s 140B, Late Fee and last date to File updated ITR Return

How these fees are payable?

As per Finance Act, Late fees under section 234F can be paid by the way of Self-Assessment Tax u/s 140A. Therefore, through Challan 280, under the head of Self-Assessment Tax, these fees can be paid from FY 17-18 and onwards.

Normal Due date of Advance Tax under the income tax act

| Installments | Rate of Advance Tax | Total Liability/due under adavnce Tax |

|---|---|---|

| First Installments | 15 % | 4,80,000*15%= 72,000 |

| Second Installments | 45% | 4,80,000*45%= 2,16,000 |

| Third Installments | 75% | 4,80,000*75%= 3,60,000 |

| Fourth Installments | 100% | 4,80,000*100%= 4,80,000 |

kind of Interest under section 234 of the income tax act

There are three kind of interest payable u/s 234 of the I-Tax Act 1961. as below mention here under :

- Interest under section 234A—Delay in Filing of Income Tax Return

- Under Section 234B interest—Delay in payment of Advance Tax

- Interest under section 234C—Short payment of Advance Tax

1st Update of 2024 :

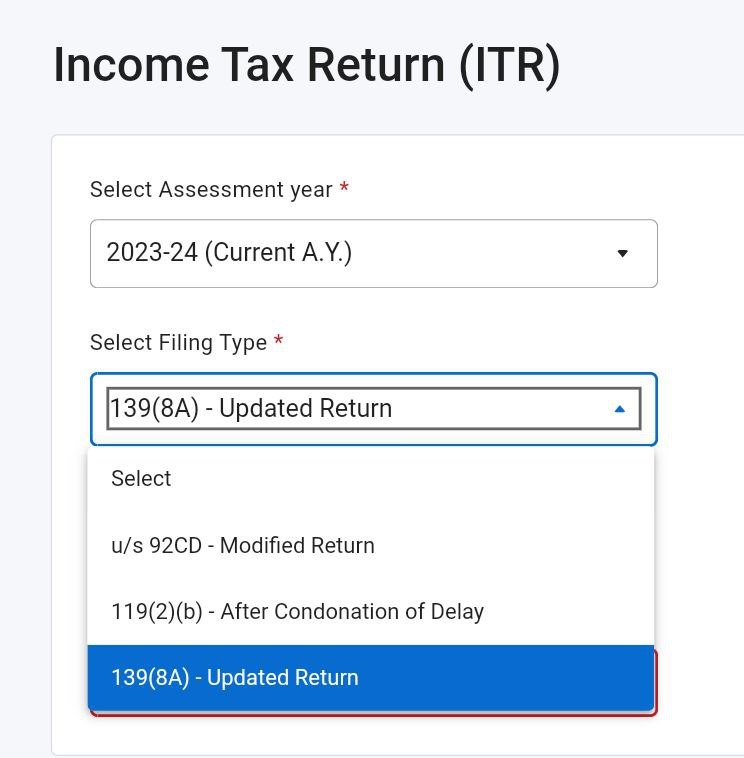

- E-filing of Updated Income Tax return has been enabled on Income Tax Portal for Assessment Year 2023-24 (Financial Year 2022-23)

Practical Impact: The amendment seeks to strike a balance.

- Government Gets : Faster collection of revenue, Reduced litigation, better tax compliance and Increased voluntary disclosures.

- Taxpayer Gets : Opportunity to regularise past defaults, Protection from harsh penalty provisions, Greater certainty and Reduced litigation risk

- The evolution of ITR-U shows a clear policy shift towards “disclose voluntarily and pay, rather than litigate.”

Position after Finance Acts 2025 & 2026

- Updated Return filing period increased from 24 months to 48 months.

- Additional tax ranges from 25% to 70% depending upon delay.

- Cost of delay increases year after year.

- Special protection introduced for qualifying Section 148-related Updated Returns.

- Income disclosed through such returns can enjoy immunity from penalty under Section 270A.

- Encourages voluntary compliance while ensuring the Government receives tax, interest, and substantial additional revenue.

For query or help, contact: singh@carajput.com or call at 9555-555-480