Complete Guide RCM under GST

Page Contents

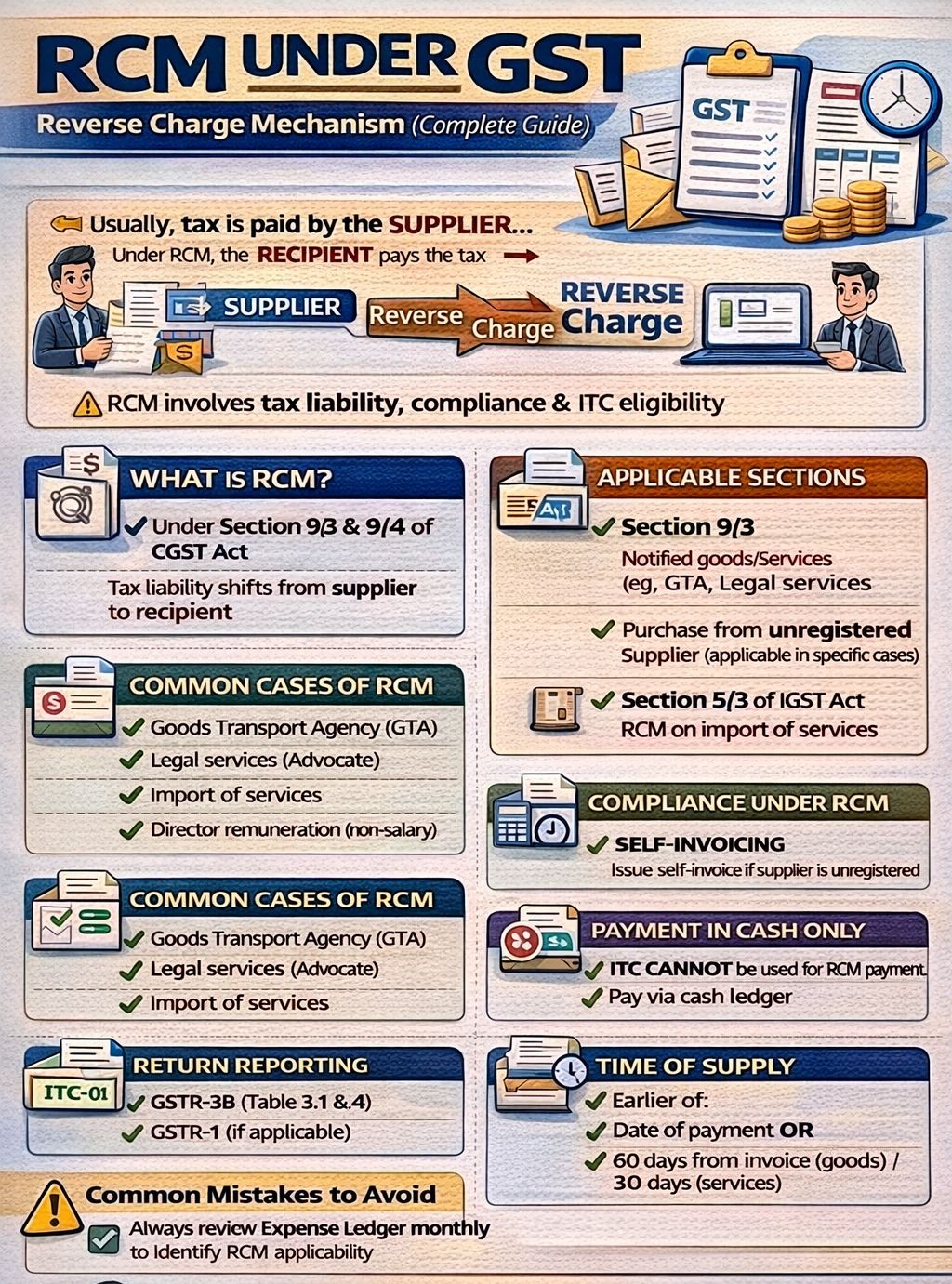

Complete Guide to Reverse Charge Mechanism (RCM) under GST

Under Goods and Services, tax is generally paid by the supplier…But in specified cases, the recipient becomes liable. This is called the reverse charge mechanism. Mismanaging the reverse charge mechanism is one of the top reasons for Goods and services notices & Input tax credit disputes.

What is RCM? :

Under Section 9(3) & 9(4) of CGST Act and Section 5(3) of IGST Act,

The liability to pay GST shifts from supplier → recipient. Monthly review of legal & professional expenses , freight/logistics payments, foreign payments (import of services), and related party transactions. It’s important to map GL codes with the Reverse Charge Mechanism applicability matrix. The reverse charge mechanism is not just a compliance provision. it’s a litigation trigger point by reason of the following reasons: no supplier compliance trail , fully department-driven detection, and easy mismatch via AIS / Goods and Services analytics. RCM MATTERS because it ensures tax collection where the supplier is unregistered / outside India, protects revenue leakage, and avoids interest (18%) , penalty, and input tax credit disallowance. The reverse charge mechanism is less about volume and more about vigilance

LEGAL FRAMEWORK (SIMPLIFIED)

- Section 9(3) → Notified goods/services (mandatory Reverse Charge Mechanism)

- Section 9(4) → Purchase from unregistered suppliers (restricted applicability)

- Section 5(3) IGST → Import of services (always under Reverse Charge Mechanism )

- Important: Section 9(4) is not blanket applicable—it applies only to notified classes of registered persons.

COMMON & PRACTICAL RCM CASES

- Services: Goods Transport Agency, Legal services (advocate/firm), Director remuneration (non-salary), Security services (if supplier is non-body corporate & recipient is body corporate) and Import of services

- Goods (Notified) : cashew nuts (raw), Tobacco leaves, Scrap (in certain cases)

CORE COMPLIANCE REQUIREMENTS

- Self-Invoicing (Sec 31(3)(f)) : Mandatory if supplier is unregistered Also issue a payment voucher at the time of payment.

- Payment of Tax : Input tax credit cannot be used and Must be paid in cash ledger only

- Input tax credit eligibility (Sec 16) : Available only after payment of Reverse Charge Mechanism tax. Subject to business purpose, not blocked under Section 17(5), and the reverse charge mechanism creates a timing difference, not a cost (if ITC eligible).

Return Reporting

GSTR-3B

- Table 3.1(d) → Reverse Charge Mechanism liability

- Table 4(A) → Input tax credit claim

GSTR-1 : Generally, not required for pure Reverse Charge Mechanism (except self-invoice scenarios impacting reporting)

Time of Supply (Critical for Interest Risk)

- Goods (Reverse Charge Mechanism): earlier of Date of payment or 30 days from supplier invoice

- Services (Reverse Charge Mechanism): the earlier of the date of payment or 60 days from the invoice. If not determinable → Date of entry in books

HIGH-RISK AREAS (WHERE NOTICES ARISE)

- Missing RCM on import of services (very common)

- Treating director remuneration incorrectly (salary vs professional)

- Wrong classification of GTA (forward vs. reverse charge mechanism option)

- Claiming Input tax credit before paying Reverse Charge Mechanism tax

- No self-invoice / payment voucher