Overview on Stock Transfer vs Supply under GST

Page Contents

Comparison Matrix: Stock Transfer vs. Branch Transfer under GST

A Technical Analysis for Multi-Registration Businesses

GST fundamentally changed the tax consequence of inter‑unit movements. What was a mere “stock transfer” under Central Excise/VAT is now often treated as a taxable supply when it occurs between GST registrations of the same legal entity.

For businesses operating across multiple GST registrations (same PAN, different States or verticals), branch transfer is not a mere internal movement. it can become a taxable supply under the GST law. Since you actively track GST circulars and compliance nuances, here’s a technically structured yet practical explanation aligned with the CGST framework.

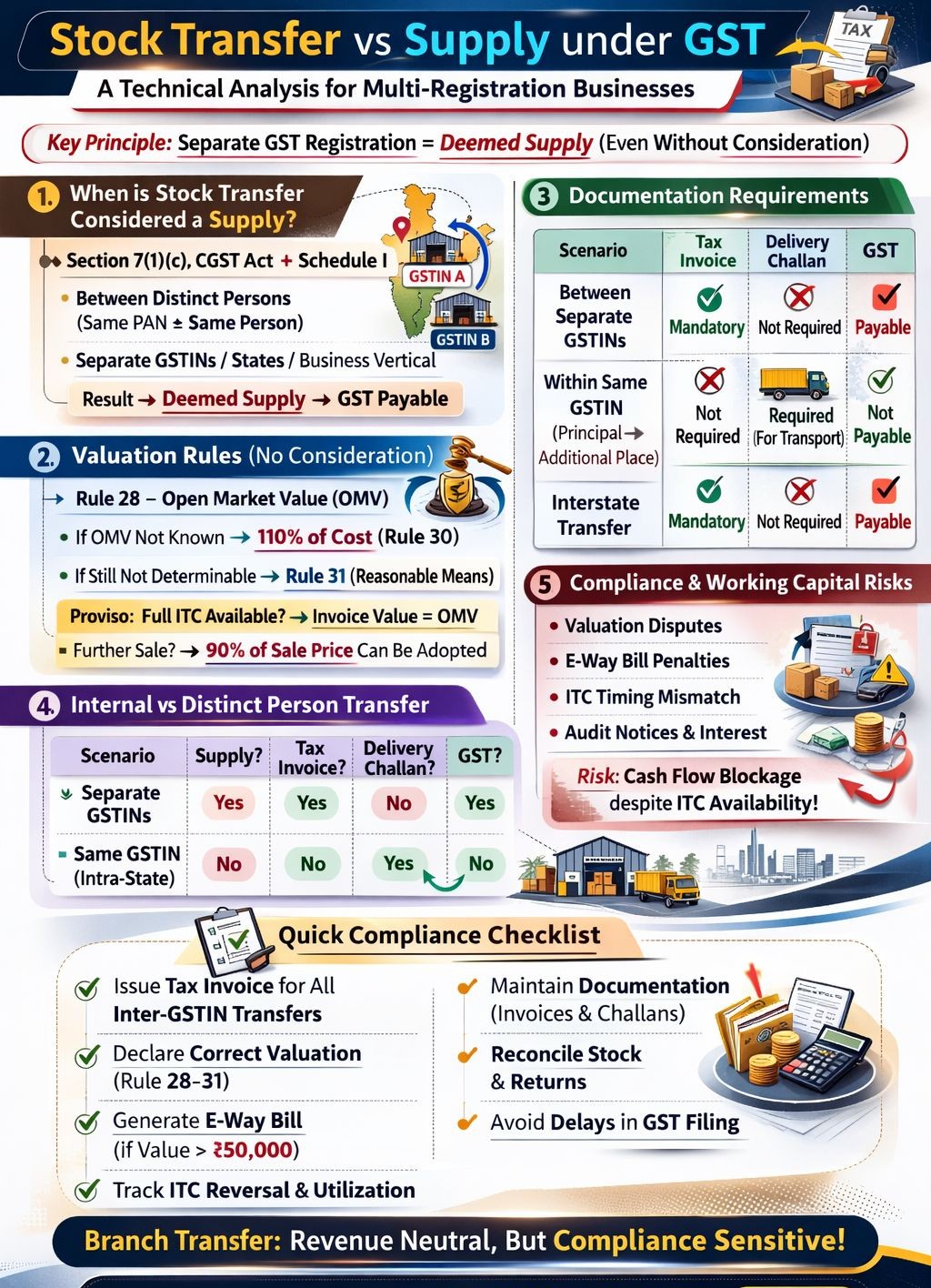

Whether Stock Transfer Constitutes “Supply” :

- Under Section 7(1)(c) of the CGST Act, read with Schedule I, supply includes: Supply of goods between distinct persons, even without consideration.

- As per Section 25(4) & 25(5): Separate GST registrations under the same PAN, registrations in different states, and separate business verticals with distinct registration.

Section 25 – Distinct Persons: Different GST registrations of the same PAN in different states are distinct persons. This creates the primary rule. “Different GSTIN = supply” and “Same GSTIN = not a supply (usually)”

These are treated as distinct people. Transfer of goods between two GST registrations of the same legal entity = Deemed Supply, even without consideration.

Stock Transfer (Same Goods and Services Tax Identification Number): Not a Supply

- When it applies: Multiple godowns/storage locations within the same Goods and Services Tax Identification Number (same state registration). And branches/units sharing the same state GST registration.

- Tax Consequence: Not treated as supply (no distinct persons).

- Documentation: Delivery Challan (as per Rule 55). And an E‑way bill if the value is greater than ₹50,000 or state threshold rules apply.

- Return Reporting: Not reported in GSTR‑1 or GSTR‑3B.

- ITC: No impact on ITC at either unit, as no supply exists.

- Accounting: Pure inventory movement.

Branch Transfer (Different Goods and Services Tax Identification Number):

Treated as Supply. If goods move from one Goods and Services Tax Identification Number to another under the same PAN:

- Why it is a Supply: Section 25 → they are “distinct persons,” and Schedule I → supply even without consideration

- GST Applicability: Inter‑State movement → IGST and Intra‑State (multiple registrations in same state) → CGST + SGST. (Even though rare, multiple registrations within the same state are possible for SEZ, business verticals, warehouses, TCS operators, etc.)

- Documentation: A tax invoice is mandatory.

- Valuation (Rule 28): Value must be the open market value, or if unavailable : 90% of the price charged to an unrelated customer (optional), or cost + 10% (Rule 30), or reasonable means (Rule 31).

- Proviso for Full ITC: If the receiving branch is eligible for full ITC, the declared invoice value = open market value. This proviso is a key tax‑planning element for large enterprises.

- Reporting: Reported as outward supply in GSTR‑1. And tax paid in GSTR‑3B.

- ITC: The receiving unit claims ITC in its 3B.

- Accounting: Stock transfer and GST liability, and the receiving unit recognizes stock and ITC.

Valuation Framework (Rule 28 Mechanism) : Since branch transfers usually happen without consideration, valuation does not fall under normal transaction value (Section 15(1)). Instead, valuation is governed by Rule 28 of the CGST Rules, 2017. Hierarchy under Rule 28: open Market Value (OMV), Value of goods of like kind & quality, If not determinable → Rule 30 (110% of cost) and Failing which → Rule 31 (reasonable means)

Important Provisos (Very Practical)

- If the recipient is eligible for full ITC, the value declared in the invoice is deemed to be OMV.

(No need to justify OMV separately.) - If goods are further supplied “as such,” the supplier may adopt 90% of the recipient’s sale price to an unrelated customer.

This offers valuation flexibility where the ITC chain is intact.

Documentation—When to Issue What? A tax invoice is required when there is a Supply between distinct persons, Interstate movement between separate GST registrations and Branch transfer between different Goods and Services Tax Identification Numbers

Delivery Challan Required When: Movement is not treated as supply OR supply is not completed at removal. Applicable in cases like goods sent for job work, goods sent on an approval basis, liquid gas (quantity not known at removal), movement for reasons other than supply, and movement between the principal and additional places of business within the same Goods and Services Tax Identification Number.

E-Way Bill Implications : Even though it is an internal transfer, If value exceeds the threshold, E-Way Bill mandatory; Interstate branch transfers always require EWB, and mismatches between invoice value and declared value may trigger scrutiny

Working Capital & Compliance Exposure : Though branch transfer is revenue neutral (output tax = recipient ITC), practical issues arise due to Valuation disputes (especially cost + 10% cases), ITC timing mismatch, GSTR-1 vs GSTR-3B inconsistency, E-Way Bill discrepancies, Section 73/74 proceedings and Resulting temporary working capital blockage, interest exposure, and Penalty risks

Multi-State Businesses : Under GST, legal registration structure overrides commercial substance. A branch transfer may be revenue-neutral and accounting-neutral but compliance-sensitive. For businesses with multiple registrations, internal standard operating procedures should cover the standard valuation method, Cost sheet support (if Rule 30 used), E-Way Bill controls and Goods and Services Tax Return reconciliation mechanism

Comparison Matrix: Stock Transfer vs. Branch Transfer under GST

| Particulars | Stock Transfer (Same GSTIN – Within Same State) | Branch Transfer (Different GSTIN – Inter‑State or Intra‑State) |

| Nature of Transfer | Movement of goods within the same Goods and Services Tax Identification Number (e.g., godown to depot). | Movement of goods between two different GSTINs of the same PAN (distinct persons). |

| GST Applicability | No GST is applicable, as the supply requires two distinct persons (Sec 7). | GST applicable (treated as supply even without consideration—Schedule I). |

| Tax Invoice | Not required. Delivery Challan is used. | Mandatory. A tax invoice must be issued and GST charged (IGST/CGST+SGST). |

| E‑way Bill | Required if value > ₹50,000 (and state rules apply). | Required as a tax invoice is issued. |

| Valuation | Not required (no supply). | Valuation per Rule 28: Open market value / 90% of price to unrelated customer / Cost + 10%. |

| ITC Eligibility (Receiving Unit) | Not applicable. | ITC is fully available (subject to Sec 16 conditions). |

| Impact on Turnover | No impact on “supply turnover.” | Included in aggregate turnover and outward taxable supplies. |

| Compliance Burden | Very low (only stock movement records). | High: invoice, GST payment, return reporting, ITC reconciliation. |

| GST Reporting | Not reported in GSTR‑1/3B. | Reported in GSTR‑1 (as outward taxable supply) & GSTR‑3B. |

| Accounting Treatment | Simple stock movement; no revenue booking. | Recorded as a stock transfer with GST; GST booked and ITC claimed. |

| Pricing Impact | No GST cash flow. | Cash flow impact unless on full ITC mode. |

| Valuation Disputes | Rare. | Common, especially when the stock transfer price differs from the selling price. |

| Place of Supply | Not relevant (no supply). | Location of recipient (Sec 10). |

| Purpose | Operational movement (distribution, storage). | Legal supply between distinct entities for redistribution or resale. |

| Reversal of ITC (Sec 17 / Rule 42/43) | Not triggered. | May arise if goods are used in exempt activities by the receiving unit. |

Summary for Quick Understanding

- Stock Transfer (Same Goods and Services Tax Identification Number): No GST, no invoice, only delivery challan + e‑way bill (if required), not treated as supply.

- Branch Transfer (Different Goods and Services Tax Identification Number): GST compulsory even without consideration., Must issue invoice, shown in GST returns, ITC available to receiving branch, treated as taxable supply between distinct persons.

Special Situations (Important for Multi‑Location Businesses)

- Movement for Job Work (Section 143) : Job‑work movements are not supply if returned within the time limits.

- Cross‑Charging of Services: Services between Goods and Services Tax Identification Number of the same PAN must be cross‑charged, unless covered by the ISD mechanism.

- Stock Transfer to Depots Before Sales : Depot receives stock on IGST basis → sells locally with CGST + SGST.

- Free Samples/Promotions Between GSTINs : Still treated as supply due to Schedule I, even though movement is without consideration.

Practical Issues Faced by Corporates

- Valuation disputes: Especially where branch transfer price ≠ actual selling price.

- Mismatch in GSTR‑2B due to incorrect Goods and Services Tax Identification Number tagging

- Cash flow blockage: If the receiving unit has low utilization of ITC.

- Reversal under Rule 42/43 : If the receiving unit uses goods for exempt supplies.

- E‑way bill + delivery challan mismatch for bulk movements: Strategic Takeaways for Businesses

For Same‑GSTIN:

- Keep SKU‑wise tracking to defend non‑supply classification.

- Maintain challan + e‑way bill consistency.

For Different GSTIN:

- Use the full‑ITC valuation proviso to simplify pricing.

- Avoid cash flow shocks—align branch transfer value with ITC planning.

- Harmonize ERP Masters (Goods and Services Tax Identification Number‑wise defaults).

- Implement an Standard Operating Procedure for cross-charging and stock movement paperwork.

- The dividing line is clear: Stock Transfer = operational movement within the same GSTIN → NO SUPPLY

- Branch Transfer = movement between distinct persons (different GSTINs) → SUPPLY

- For multi‑registration businesses, understanding this distinction impacts Tax planning, Cash flows, Valuation, ERP configuration, compliance accuracy, and Litigation exposure