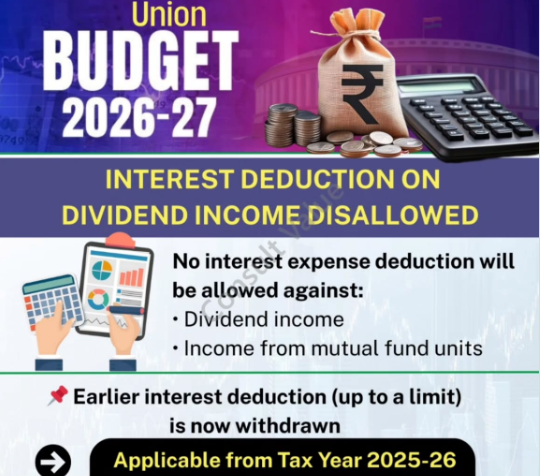

No Interest Deduction Allowed Against Dividend Income

Page Contents

No Interest Deduction Allowed Against Dividend Income (Budget 2026 Update)

Investors in stocks and mutual funds, particularly those who use leveraged tactics like margin funding or overdrafts, will be significantly impacted by the Union Budget 2026. Although this modification makes reporting easier, it greatly raises the tax burden on leveraged assets. Before FY 2026–2027, investors and corporations using debt-funded equity solutions will need to review their models. Taxpayers could deduct interest up to 20% of dividend income under the previous law. This benefit will no longer be available starting in FY 2026–2027.

What’s changing on dividend income?

Key Highlights on No Interest Deduction Allowed Against Dividend Income

Until now, taxpayers could claim a deduction for interest paid on borrowed funds used to earn dividend income (capped at 20% of the dividend).

- No Interest Deduction and No Interest Offset: Interest paid on loans/ODs used for buying shares, mutual funds, REITs/InvITs will not be allowed as a deduction. Interest paid on loans or overdrafts used to acquire shares or mutual fund units can no longer reduce taxable dividend income.

- 20% Deduction Withdrawn: Section 93(2) of the Income‑tax Act, 2025 is amended to remove the 20% cap deduction entirely.

- Full Taxation of Dividends: Dividend and mutual fund income will now be taxed entirely at slab rates — irrespective of interest costs.

- Higher Tax Outgo for Leveraged: Investors Earlier, interest costs partially offset tax liability. Now, taxation is on gross dividend.

- Effective 1 April 2026: Applicable for tax year 2026–27 and onward. A corresponding amendment has been proposed in Section 93(2) of the Income Tax Act, 2025.

Impact Example : If you earn INR 50 lakh in dividends but pay INR 40 lakh interest on borrowed funds Taxable Income = INR 50 lakh (not INR 10 lakh) and Entire dividend taxed as per slab. This significantly affects strategies involving high-yield PSUs, REITs/InvITs, and leveraged dividend investing models.

Impact on Investors Takeaway :

This amendment shifts dividend investing firmly toward non-leveraged structures. Investors relying on interest‑based arbitrage or yield‑borrowing strategies need to reassess portfolio economics post‑FY 2026–27.

- Higher tax outflow for individuals and HNIs using margin funding, OD limits, or leveraged yield strategies.

- Dividends will now be taxed on the gross amount, irrespective of interest outgo.

Impact on Corporates & Holding Structures

- Investment holding companies with borrowings for acquiring subsidiaries may face higher taxable income.

- Leveraged M&A structures may require re‑evaluation due to the loss of interest deductibility.