Complete Overview Legal Entity Identifier (LEI)

Page Contents

Complete Overview Legal Entity Identifier (LEI)

A Legal Entity Identifier (LEI) is a 20‑digit unique alphanumeric code used to identify legal entities that engage in financial transactions. It is based on the ISO 17442:2012 standard and enables uniform global identification of counterparties. The Legal Entity Identifier system was introduced by global bodies such as the G20 and the Financial Stability Board (FSB) to

- Improve transparency in financial markets

- Enable better risk management

- Track and monitor systemic risk

- Support regulatory reporting on a global scale

Structure of an Legal Entity Identifier Code

The 20-digit Legal Entity Identifier code has the following defined structure:

- Characters 1–4: LOU (Local Operating Unit) prefix

- Characters 5–18: Entity-specific code assigned by the Local Operating Unit

- Characters 19–20: Check digits

The Legal Entity Identifier contains no embedded intelligence; each code is unique but does not reveal any internal information about the entity.

Regulatory Mandates Requiring Legal Entity Identifier in India

The Legal Entity Identifier is mandatory under several Indian regulatory frameworks. Agencies requiring a Legal Entity Identifier include:

- Reserve Bank of India (RBI) – for derivatives, large corporate borrowers, forex transactions, and high‑value RTGS/NEFT payments

- SEBI – for issuers of non‑convertible securities, securitized debt instruments, and security receipts

- IRDAI – for insurers and borrowers of insurers

- Banks, NBFCs, Financial Institutions, and others in regulated financial markets

Key Situations Where a legal entity identifier is Mandatory

RBI – Large Borrowers (Credit Exposure): Entities with aggregate fund‑based and non‑fund‑based credit exposure of INR 5 crore or above must obtain a Legal Entity Identifier as per the following schedule:

- Above INR 25 crore: On or before 30 April 2023

- INR 10–25 crore: On or before 30 April 2024

- INR 5–10 crore: On or before 30 April 2025

Legal Entity Identifier for RTGS / NEFT Transactions: The legal entity identifier is mandatory for any single transaction of INR 50 crore or above carried out via RTGS or NEFT. This requirement applies per transaction, not cumulatively.

Legal Entity Identifier for Foreign Exchange (Forex) Transactions: In non‑derivative forex markets, Legal Entity Identifier is required for Any single transaction of USD 1 million or equivalent. Applies to cash, tom, and spot transactions.

Steps for Applying for a Legal Entity Identifier

Follow the steps below to complete a legal entity Identifier registration:

- Visit the LEIL (Legal Entity Identifier India Ltd.) website

- Create a user account on the portal

- Upload mandatory documents, such as:

-

- Letter of Authority (LOA) / Board Resolution

- Audited financial statements

- Parent company financials / auditor certificate (where applicable)

- Pay the LEI registration fees online

- LEIL validates the documents and issues the Legal Entity Identifier within 1–2 working days

Documents Required for Legal Entity Identifier Application

You must upload or submit:

- Letter of Authority (LOA) or Board Resolution authorizing the applicant

- Audited financial statements of the legal entity

- Parent company audited financials or an auditor certificate, if the entity has a direct or ultimate parent

Legal Entity Identifier registration & renewal fees:

| Type | Fee (Including GST) |

| New Registration | INR 4,130 |

| Renewal (Annual) | INR 3,304 |

| Multi‑Year Options | Available for 2 to 5 years |

Multi-year renewals help avoid lapsing and reduce annual administrative work.

Legal Entity Identifier Validity & Renewal Requirements:

- The legal entity identifier is valid for 1 year

- It must be renewed annually to remain active

- If the Legal Entity Identifier is not renewed, its status becomes LAPSED, which may restrict banking, financial, and regulatory transactions

Authorized Person Requirements : A Legal Entity identifier application can be submitted only by an authorized person, based on:

- A valid Letter of Authority (LOA), or

- A Board Resolution approving the authorized signatory

Change of Authorized Person :

If the authorized person needs to be updated:

- Submit a new LOA/Board Resolution to LEIL

- Create a new user login

- LEIL will link the existing Legal Entity Identifier to the new authorized person’s email ID

Mandatory Reporting of Relationship Data

Entities must report:

- Direct Parent

- Ultimate Parent

If parent details cannot be reported, acceptable exception reasons include the following:

- The parent does not have a legal entity identifier.

- Information is non-public due to confidentiality restrictions

- The entity is controlled by natural persons

- No consolidation required under accounting standards

Parent Data Reporting is mandatory. When

- Applying for a new Legal Entity Identifier

- Renewing an Legal Entity Identifier

- Transferring a legal entity identifier from another LOU

LEI for International Branches :

An international branch can obtain a legal entity identifier if:

- The branch is registered in India, and

- The head office already has a legal entity identifier.

Only one legal entity identifier is issued per network of branches in the host country.

Validation Agents (VA) : Validation Agents are financial institutions authorized by GLEIF to assist entities in:

- Legal Entity Identifier registration

- Legal Entity Identifier renewal

- Data validation

Current Validation Agents in India:

- Rubix Data Sciences Pvt. Ltd.

- MNS Credit Management Group Pvt. Ltd.

These agents simplify the onboarding and reduce errors in applications.

Time Taken for Legal Entity Identifier Issuance

- LEIL typically takes 1–2 working days to issue a legal entity identifier.

- This is subject to submission of correct documents and successful payment

Exception Reporting under the Legal Entity Identifier System

Entities may opt for exception reporting when they are unable to report direct parent or ultimate parent information. As per the LEIL guidelines, the following situations qualify for exception reporting:

- Parent has No Legal Entity Identifier : If the parent entity does not have an LEI number, the reporting entity may select the “No Legal Entity Identifier” exception.

- Parent Data is Non‑Public: An exception applies where parent information cannot be disclosed due to reasons such as Legal restrictions, confidentiality obligations, lack of consent, and disclosure being detrimental. These fall under the “Non‑Public” exception category.

- Entity Controlled by Natural Persons : If the entity is controlled by individuals (natural persons) without an intermediate legal entity preparing consolidated financials, exception reporting is allowed.

- Entity Not Subject to Consolidation : If the parent exists but does not prepare consolidated financial statements, the entity may report the “Non‑Consolidating” exception.

Legal Entity Identifier Status Types:

The Legal Entity Identifier system assigns different statuses based on the lifecycle and validity of a Legal Entity Identifier. Below are the key status categories defined by the LEIL framework:

- ISSUED: Indicates that the LEI is active, valid, and successfully issued.

- LAPSED: Occurs when the entity fails to renew the Legal Entity Identifier by the due date. A lapsed legal entity identifier may cause banks and regulators to reject transactions.

- RETIRED: Used when the legal entity has ceased operations, is dissolved, has merged into another entity, or no longer legally exists.

- TRANSFERRED : Means the Legal Entity Identifier record has been moved to another LOU (Local Operating Unit) for management.

- PENDING: The Legal Entity Identifier application has been submitted and is under validation by the LOU.

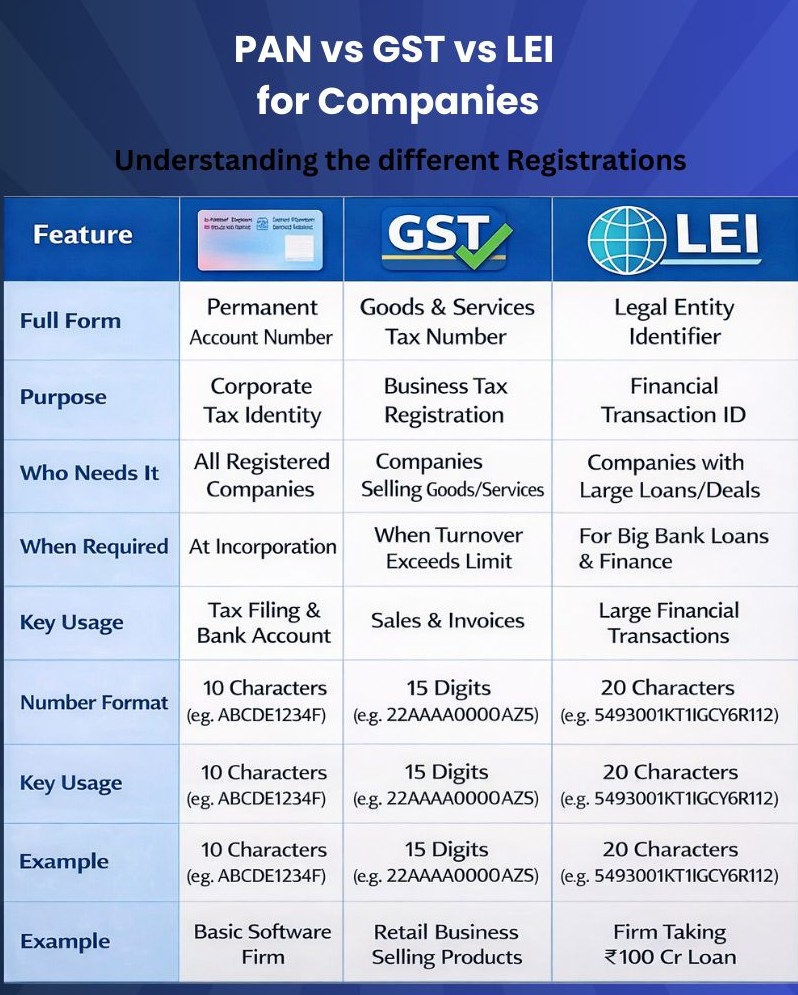

Key Differences at a Glance – PAN vs GSTIN vs LEI

| Feature | PAN | GSTIN | LEI |

| Full Form | Permanent Account Number | Goods & Services Tax Identification Number | Legal Entity Identifier |

| Purpose | Income tax identification | Indirect tax compliance (GST law) | Transparency in global financial transactions; counterparty identification |

| Format | 10‑character alphanumeric | 15‑character alphanumeric | 20‑character alphanumeric |

| Issuing Authority | Income Tax Department (CBDT) | Goods & Services Tax Council / GSTN | Global Legal Entity Identifier Foundation (GLEIF) + LEIL (India) |

| Applicability | Mandatory for all businesses & individuals for income tax | Required based on turnover, interstate supply, business activity | Required based on financial exposure & regulatory mandates (RBI, SEBI, IRDAI) |

| Primary Use | Income tax filing, banking, statutory KYC | Goods & Services Tax returns, invoicing, ITC claims | Loans, derivatives, RTGS/NEFT ≥ ₹50 crore, forex ≥ USD 1 million |

| Regulatory Domain | Income Tax Act | Goods & Services Tax Law | RBI, SEBI, IRDAI, G20/FSB global framework |

| Who Needs It? | Individuals & entities having taxable income | Businesses exceeding Goods & Services Tax threshold or doing interstate supply | Entities engaged in high‑value financial transactions |

Common Misconceptions About Compliance, PAN, GST & LEI

Misconception 1: “PAN is enough for all compliance”

Reality: A PAN (Permanent Account Number) is used only for Income Tax–related identification. It is not sufficient for

- GST compliance

- Banking regulations (e.g., LEI requirement for high‑value payments)

- RBI‑mandated financial transactions

- Corporate or regulatory reporting outside Income Tax

Misconception 2: “LEI replaces PAN” Reality:

A Legal Entity Identifier (LEI) is an additional global identification requirement, especially for:

- Large borrowers

- Derivatives

- High‑value RTGS/NEFT

- Forex transactions

- SEBI and IRDAI‑regulated activities

LEI does NOT replace PAN.: Both serve different regulatory purposes and are required simultaneously in many cases.

Misconception 3: “GST is required for every company”

Reality: GST registration is not mandatory for every business or company.

It depends on:

- Annual turnover thresholds

- Nature of business activity

- Inter‑state supply conditions

- E‑commerce operations

- Special category supplies

Many small businesses below the threshold limit are not required to register under GST.