CBDT :Releases Draft Income Tax Rules, 2026 & Draft Form

Page Contents

CBDT Releases Draft Income Tax Rules, 2026 & Draft Forms

Draft Income-tax Rules, 2026—What You Need to Know: Key Changes, Mapping Tools & Practical Implications

The Central Board of Direct Taxes has published the Draft Income Tax Rules, 2026, along with draft forms for public consultation. This is ahead of the Income-tax Act, 2025, becoming effective from 1 April 2026. The Income Tax Department has released the Draft Income Tax Rules, 2026, proposed to take effect from 1 April 2026, alongside simplified return forms and procedures. These rules support the rollout of the Income-tax Act, 2025, and are aimed squarely at simplifying compliance and reducing litigation The draft rules focus on simplification, digital compliance, and improved taxpayer experience.

Public feedback window: Open till 22 February 2026 – (15 days):

A short 15-day consultation window for a major rewrite and heavy reliance on digital readiness may challenge small taxpayers and also MSMEs. This is real compliance relief, which depends on final rules and system execution. The Income-tax Act, 2025, is a complete rewrite of India’s direct tax law. Instead of revising the old framework, the Central Board of Direct Taxes has created an entirely new set of rules, replacing the Income-tax Rules, 1962. Early evaluation will help in system upgrades, SOP changes, client communication, and preparing for FY 2026–27.

Mandatory Digital Books of Account — Draft Rule 46

Under Draft Rule 46 (mapped from old Rule 6F), specified professionals must maintain their books and documents In electronic format, Accessible in India at all times, With backup servers physically located in India and Updated daily. These requirements form part of the broader shift toward a digital‑first compliance ecosystem.

PAN Quoting Threshold Realignment — Draft Rule 159

The draft introduces a revised PAN‑mandatory transaction threshold, including PAN must be quoted for sale or purchase of motor vehicles exceeding ₹5 lakh. This is part of the rationalisation of reporting norms and alignment with the new draft rule structure. Higher Threshold for Property SFT Reporting — Draft Rule 237 The reporting threshold under the SFT (Statement of Financial Transactions) for property‑related dealings has been increased to ₹45 lakh (earlier ₹30 lakh). This change aims to reduce unnecessary compliance for lower‑value property transactions.

Draft rules applicable from FY 2026–27, subject to final notification.

Drafting Philosophy Behind the New Rules. The draft rules adopt the same simplification-focused approach as the new Act:

· Clear, concise, and modern drafting

· Tables, formulas & structured layouts for clarity

· Deletion of redundant/obsolete provisions

· Procedural sync with the Income-tax Act, 2025

· Reduced subjectivity and scope for disputes

Massive Rationalization—Income Tax Rules & Forms Reduced

| Particulars | IT Rules, 1962 | Draft IT Rules, 2026 |

| Total Rules | 511 | 333 |

| Total Forms | 399 | 190 |

Across the draft framework, the CBDT has emphasised Simplified language and rationalisation of procedures, Standardised, smart forms with pre‑fill and automated reconciliation features, Reduction of rules from 511 → 333 and forms from 399 → 190 and Enhanced digital administration and faceless processes. These reforms are intended to reduce compliance burden, eliminate redundancies, and enhance the overall taxpayer experience.

This rationalisation comes from Consolidation, Removal of obsolete provisions and Elimination of duplicative forms

New “Smart Forms”—A Technology-First Framework

The redesigned forms introduce automation-friendly, standardized compliance:

· Uniform data fields across multiple forms

· Prefill, validation & auto-reconciliation

· Reduced manual input and error risk

· Simplified notes & instructions

Enables centralized processing, data analytics, and faster scrutiny.

Rule & Form Mapping Navigators Transition Made Easier:

The Central Board of Direct Taxes has released two key navigators

Rule Mapping Navigator :

Maps: Income-tax Rules, 1962 : Draft Rules, 2026 Helps identify corresponding provisions. Merged/restructured rules and Newly introduced rules

Form Mapping Navigator : Maps old forms to new draft forms with new reporting requirements, data capture changes, and modified compliance workflows. These tools will be essential for feedback, transition planning, and training.

Expected Compliance Benefits

· Improved clarity & interpretation

· Lower compliance burden

· Reduced litigation risk

· Better digital integration

· Faster processing & improved taxpayer services

Objective: Ease of Living + Ease of Doing Business

Practical Gaps & Transition Risks

· Short 15-day consultation window

· Renumbering may initially cause confusion

· Digital-readiness challenges for small taxpayers, MSMEs & non-tech users

· Real-world relief depends on system implementation, not just drafting

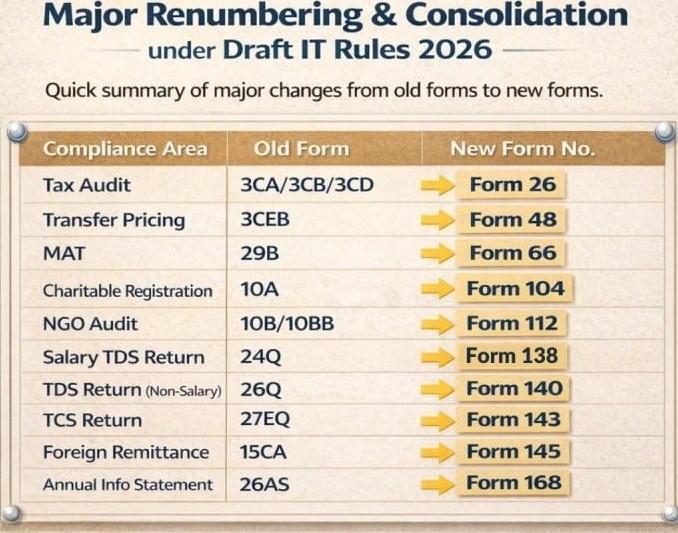

Major Renumbering & Consolidation under Draft IT Rules 2026

Few old Income‑tax forms are proposed to be renumbered into new form numbers under the Draft Income-tax Rules, 2026. Under the Draft Income‑tax Rules, 2026, the Income-tax Department proposes to Renumber many existing forms, (e.g., 3CD → Form 26) , Consolidate related forms into unified formats (e.g., 3CA/3CB/3CD merged under one new numbering), Align form numbering logically across compliance categories Transfer Pricing forms grouped in one range, audit forms in another, etc. This is part of the government’s initiative to simplify compliance, standardize form structure, reduce duplication across forms and make e-filing formats uniform. Change in compliance Area under Old Form and New Form No. following Covered as under:

| Compliance Area under Draft IT Rules 2026 | Old Income Tax Form No. | New Income Tax Form No. |

| Tax Audit | 3CA / 3CB / 3CD | Form 26 |

| Transfer Pricing | 3CEB | Form 48 |

| MAT (Minimum Alternate Tax) | 29B | Form 66 |

| Charitable Registration | 10A | Form 104 |

| NGO Audit Report | 10B / 10BB | Form 112 |

| Salary TDS Return | 24Q | Form 138 |

| Non-Salary TDS Return | 26Q | Form 140 |

| TCS Return | 27EQ | Form 143 |

| Foreign Remittance Certificate | 15CA | Form 145 |

| Annual Information Statement (AIS) | 26AS | Form 168 |

Action Points for Tax Professionals & Organisations

· Review draft rules relating to your operations (income heads, deductions, procedures).

· Analyze draft forms for data changes & new disclosures.

· Use Rule/Form Navigators to compare old vs. new.

· Submit targeted, rule-specific feedback.

What Taxpayers & Professionals Should Do Now

· Review draft rules relevant to your practice/business,

· Analyse changes in ITR data requirements

· Identify areas needing clarification

· Submit focused feedback before 22 Feb 2026

Simplified & Smart ITR Forms : Introduction of standardized, technology-enabled forms, extensive use of prefilled data, auto-reconciliation, and built-in validations. This implementation will Reduced need for repetitive disclosures across multiple forms

Outcome: Lower manual effort + fewer errors : Reduced Compliance Burden on taxpayer and Consolidation of procedural requirements, Removal of obsolete and duplicative provisions and Streamlined reporting across income categories

Outcome: Less paperwork, faster filing, alignment with digital tax administration, and income tax Forms designed for centralised processing. Improved data analytics for the department and faster turnaround time for returns and refunds. This will help in System-driven compliance instead of manual scrutiny

Proposed applicability from FY 2026-27 (AY 2027-28), Draft rules replace the Income-tax Rules, 1962, and Stakeholder feedback invited before final notification; moreover, this is time to prepare systems, SOPs, and advisory models

New Electronic Payment Modes Recognised — Draft Rule 48 : A Tier‑III category has been added under permissible electronic payment modes, now recognizing Full‑KYC Digital Rupee (P‑CBDC) wallets and Wholesale & cross‑border CBDC transactions. This aligns taxation procedures with India’s evolving digital payments and CBDC framework.

ITR Forms under Draft Income-tax Rules, 2026

The draft rules make one thing clear: ITR numbers may look familiar, but eligibility, disclosures, and filing discipline will change materially from 1 April 2026.

- ITR-1 (SAHAJ): Still Simple, Now Strictly Digital. Who it’s for Resident individuals, Salary income, One house property and Other income like interest. ITR-1 remains for straightforward cases only, Electronic filing is mandatory, Paper filing allowed only for super senior citizens (80+) and Filing through EVC or DSC becomes the norm. Sahaj stays simple—but only if facts are clean and basic

- ITR-2: Default Once Things Get Complex , ITR-2 Applicable to Individuals / HUFs, No business or professional income, Capital gains, Multiple house properties and Foreign income or assets. Basic changing is clearly positioned as the fallback return once ITR-1 conditions fail. Expected expanded disclosures, especially for Capital gains (new framework) & Foreign assets & income (tighter rules). The moment complexity enters, ITR-2 becomes compulsory

- ITR-3: Business & Profession = Heavy Disclosure. Who must file Business or professional income earners, Non-presumptive cases & Complex income profiles. Under the new rules ITR-3 becomes unavoidable once simplified regimes don’t apply, Likely to see more granular disclosures for Professionals, Traders, High-income individuals & Special income categories. Business income is data depth, not shortcuts

- ITR-4 (SUGAM): Biggest Tightening then earlier. This is the most impactful change for individuals and small businesses. Still available for Presumptive taxation cases But NOT allowed if you have Foreign assets or foreign income, Directorship in a company, Unlisted equity shares, Total income exceeding INR 50 lakh, More than two house properties and Carry-forward losses, and Agricultural income above INR 5,000. Many taxpayers who earlier used Sugam will now be forced into ITR-3. ITR-4 is no longer a “default easy option”

- ITR-5 & ITR-6: Structure Same, Compliance Deeper. ITR-5 is applicable on Firms, LLPs, AOPs, BOIs.

- ITR-6 is applicable on Companies. New under ITR 6 is Stronger digital compliance, tighter audit linkages and Integration with new returns is ITR-A (business reorganisation) and ITR-BL (block assessment). Forms stay familiar, but backend scrutiny increases

- ITR-7: Trusts & Institutions Under Sharper Lens : Applicable to Charitable trusts, Political parties & Exempt institutions. Key focus areas under ITR Forms under Draft Income-tax Rules, 2026. ITR -7 is Electronic filing, Audit report linkage, Donation disclosures, and Fund utilisation tracking. Defective or delayed filing may risk registration or exemptions. Substance over form compliance discipline is critical

The Draft Income-tax Rules, 2026 send a uniform signal Digital filing is mandatory, Simplified returns are narrowly defined, Disclosure requirements are expanding, Tax administration will rely on structured data, not explanations, Study draft ITR eligibility conditions and identify likely migration between forms after that Review disclosure changes then Submit practical feedback by 22 February 2026.

From 1 April 2026, filing an ITR will be less about choosing a familiar form and more about qualifying correctly, disclosing fully, and filing digitally. The era of “easy forms for complex facts” is clearly ending.

India’s Regulatory Push on Crypto, AI & Digital Compliance

- According to Rajput Jain and Associates, India’s latest regulatory moves reflect a decisive shift towards tighter oversight of digital and emerging sectors, particularly crypto-assets and AI-driven ecosystems.

- Core Regulatory Signals Introduce India’s Regulatory Push on Crypto, AI & Digital Compliance

- Stricter Reporting for Crypto-Asset Service Providers (CASPs) : Introduction of rigorous reporting obligations for entities dealing in crypto-assets and alignment of compliance and due diligence norms with global standards, which focus on tracking transactions, beneficial ownership, and cross-border flows. This creates the objective of India’s regulatory push on crypto, AI & digital compliance, which curbs base erosion, profit shifting, and opacity in digital asset transactions.

- Global Alignment of Due Diligence Norms : Indian framework increasingly mirrors OECD, FATF, and international tax transparency standards. So Signals India’s intent to Avoid regulatory arbitrage and Strengthen credibility in global digital finance governance

Crypto and AI-linked businesses will no longer operate in a regulatory grey zone.

- Faceless Proceedings & Digitized Dispute Resolution can continue emphasis on Faceless assessments, digital notices and responses, and online dispute resolution mechanisms. Which creates a positive impact via Reduced physical interface, Lower litigation friction, and greater process transparency

- For businesses, it helps with higher compliance cost for crypto & tech platforms. The Need for strong internal controls, audit trails, and data governance and Early investment in compliance tech becomes essential

- Increased advisory demand in Crypto taxation, international reporting, Digital compliance frameworks and Greater scrutiny under anti-avoidance and information-sharing regimes

- For India’s AI & Tech Ambitions, regulatory clarity improves investor confidence, balances innovation with accountability, and supports sustainable scaling of AI and fintech ecosystems.

- Over-regulation risk for startups and smaller players and Execution quality will determine whether compliance becomes facilitator or friction also Need for clear guidance notes and FAQs to avoid interpretational disputes

- India is clearly positioning itself as a rule-based digital economy, where innovation in AI, crypto, and fintech is encouraged—but not at the cost of transparency, tax integrity, or systemic risk. The regulatory direction is firm: digitise, disclose, and comply

Conclusion

The Draft Income Tax Rules, 2026, represent a structural reset of India’s compliance architecture. With new rules, new forms, and new mapping tools, this is the biggest procedural overhaul in decades. The consultation phase is a pivotal opportunity for stakeholders to shape the final framework before it becomes operational on 1 April 2026. The Draft Income-tax Rules, 2026, signal a shift from form-heavy compliance to smart, system-driven taxation. If implemented well, they can significantly improve ease of compliance, but the transition phase will be critical.