Page Contents

Also Read : Different meanings of turnover

o Individuals include the individual and HUF

o Company and others include Company, Company, LLP, Co-op Society, Local Authority.

The Minister of Finance has outlined a series of relief measures under the Income Tax Act, which are set out below:

(a) The TDS/TCS rates for defined payments/receipts shall be decreased by 25%. This reduction in the rate shall be applicable for tax deducted or assessed between 14-05-2020 and 31-03-2021.

(b) All unpaid refunds to nonprofit organizations and non-corporate companies and occupations shall be issued shortly.

(c) The due date of all revenue-tax returns for the financial year 2019-20 will be increased from 31 July 2020 and 31 October 2020 to 30 November 2020.

(d) The deadline date for the tax audit referred to in Section 44AB shall be increased from 30 September 2020 to 31 October 2020.

(e) The final date of selecting for the Vivad se Vishwas scheme without paying an extra 10% of the tax at issue shall be expanded until 31 December 2020.

(f) The deadline of 30-09-2020 for completion of the evaluations shall be extended to 31- 12-2020. If the evaluation is blocked on 31-03-2021, it shall be extended to 30-09-2021.

| Section | Nature of Income | Rate of TDS applicable for the period | Threshold Limit for deduction tax | |

| 01-04-2020 to 13-05-2020 | 14-05-2020 to 31-03-2021 | |||

| 193 | Interest on Securities | 10% | 7.50% | – |

| 194 | Dividend | 10% | 7.50% | Rs. 5,000 in case of Individual |

| 194A | Interest other than interest on Securities | 10% | 7.50% | Rs. 5,000 to Rs. 50,000 |

| 194C | Payment to Contractors | – 1%: If deductee is an individual or HUF – 2%: In any other case | – 0.75%: If deductee is an individual or HUF – 1.50%: In any other case | – Single payment : Rs. 30,000 – Aggregate payment: Rs. 100,000 |

| 194D | Insurance Commission | – 10%: If deductee is domestic Company – 5%: In any other case | – 7.50%: If deductee is domestic Company – 3.75%: In any other case | 15,000 |

| 194G | Commission and other payments on sale of lottery tickets | 5% | 3.75% | 15,000 |

| 194H | Commission and Brokerage | 5% | 3.75% | 15,000 |

| 194-I | Rent | – 10%: If rent pertains to hiring of immovable property – 2%: If rent pertains to hiring of plant and machinery | – 7.50%: If rent pertains to hiring of immovable property – 1.50%: If rent pertains to hiring of plant and machinery | 2,40,000 |

| 194-IB | Payment of Rent by Certain Individuals or HUF | 5% | 3.75% | 50,000 |

| 194J | Royalty and Fees for Professional or Technical Services | – 2%: If royalty is payable towards sale, distribution, or exhibition of cinematographic films – 2%: If the recipient is engaged in business of operation of call Centre – 2%: If sum is payable towards fees for technical services (other than professional services) – 10%: In all other cases | – 1.50%: If royalty is payable towards sale, distribution, or exhibition of cinematographic films – 1.50%: If the recipient is engaged in business of operation of call Centre – 1.50%: If sum is payable towards fees for technical services (other than professional services) – 7.50%: In all other cases | – Director’s fees: Nil – Others: Rs. 30,000 |

| 194M | Payment to contractor, commission agent, broker or professional by certain Individuals or HUF | 5% | 3.75% | 50 lakhs |

| 194N | Cash withdrawal | – 2%: In general if cash withdrawn exceeds Rs. 1 crore – 2%: If the assessee has not furnished return for the last 3 assessment years and cash withdrawn exceeds Rs. 20 lakhs but does not exceed Rs. 1 crore – 5%: If the assessee has not furnished return for last 3 assessment years and cash withdrawn exceeds Rs. 1 crore | – 1.50%: In general if cash withdrawn exceeds Rs. 1 crore – 1.50%: If the assessee has not furnished return for the last 3 assessment years and cash withdrawn exceeds Rs. 20 lakhs but does not exceed Rs. 1 crore – 3.75%: If the assessee has not furnished return for last 3 assessment years and cash is withdrawn exceeds Rs. 1 crore | – If a person defaults in the filing of return: 20 lakhs – If no default is made in the filing of return: Rs 1 crore |

Tentative rates of TCS

| Section | GST liable to TCS | Rate of TDS applicable for the period | |

| 14-05-2020 to 31-03- 2021 | 14-05-2020 – 31-03- 2021 | ||

| Section 206C(1) | Alcoholic liquor for human consumption | 1% | 0.75% |

| Section 206C(1) | – Timber obtained under Forest lease – Timber obtained by any mode other than under a forest lease – Any other forest produce not being timber or tendu leaves | 2.50% | 1.875% |

| Section 206C(1) | Tendu leaves | 5% | 3.75% |

| Section 206C(1) | Minerals, being coal or ignite or iron ore | 1% | 0.75% |

| Section 206C(1) | Scrap | 1% | 0.75% |

| Section 206C(1C) | Parking Lot | 2% | 1.50% |

| Section 206C(1C) | Toll Plaza | 2% | 1.50% |

| Section 206C(1C) | Mining & quarrying | 2% | 1.50% |

| Section 206C(1F) | Motor Car | 1% | 0.75% |

| Section 206C(1G) | Overseas tour travel package | 5% | 3.75% |

| Section 206C(1G) | Remittance of Forex under LRS of Rs. 7 lakh or more in a financial year | 0.5%: Where remittance is a repayment of loan obtained for the purpose of pursuing any education 5%: In any other case | 0.375%: Where remittance is a repayment of loan obtained for the purpose of pursuing any education 3.75%: In any other case |

| Section 206C(1H) | Sale of goods in excess of Rs. 50 lakh | 0.10% | 0.075% |

As per section 201(1A), Interest at the rate of 1 % per month or part of the month on the balance of TDS deductible from the date of tax before the date of the tax finally deducted shall be paid for the late deduction.

In addition, interest for late payment at a rate of 1.5 percent per month or half of the month on the number of TDS withheld from the date of tax to the day on which the tax is collected shall be levied.

Related Articles/pieces of information : How to file the return of TDS online

Fees are payable at Rs. 200 a day for each day on which the loss continues. The amount of the fees can not exceed the value of the TDS.

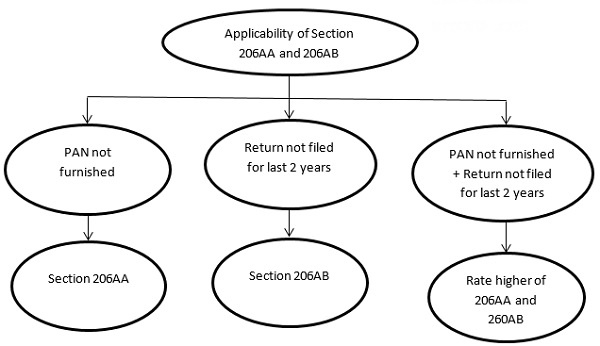

In order to have a better knowledge of the newly inserted section, let us first know the applicability of Section 206AA & 206CC in brief as the following –

| Tax is required to be collected | Tax is required to be deducted |

| (i) at 2 time of the rate specified in the relevant section provision of this Act; | (i) at the rate specified in the relevant provision of this Act; |

| (ii) at the rate of 5%: | (ii) at the rate or rates in force; or |

| (iii) at the rate of 20%: |

Also Read : New TDS deduction No cash transactions exceeding 1 Crore -Section 194N

Related Articles/pieces of information : key features of TCS on goods sale section-206c

You can give your comments and suggestions under the comment box.

Form 16A (Earlier Reflected in Form 26AS) Now Shows Deductor PAN: A Small Change with a Big Impact on TDS Reconciliation… Read More

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}